I was forced to talk about bitcoin this week. On a podcast (in German).

The discussion was triggered by the remarkable surge in bitcoin’s value – the second great surge in the Ur-crypto’s turbulent history since it’s launch on 3 January 2009.

Lisa Splanemann, the journalist with whom I do the podcast, has been pushing the topic for a while. I was reluctant.

Money talk is political talk. We should be selective in the political talk we engage in. I don’t like the politics of crypto/bitcoin.

Money is an expression of social power. In particular, it is an amalgam of the power and confidence leveraged by the state and capital. All actual monies, whatever form they are cast in, have an element of “fiat” about them.

As the Merriman-Webster dictionary helpfully explains: “fiat: a command or act of will that creates something without or as if without further effort. According to the Bible, the world was created by fiat.”

The fiat money world is the world that we have inhabited since the collapse of the Bretton Woods system between 1971 and 1973. It is normally contrasted to the gold standard world that preceded it. But are gold and “fiat” really that different? To back a currency with gold is a political choice too, anchored in structures of expectation on the part of creditors, debtors and investors, on systems for gold production, storage, relationships between banks and central banks, in other words structures of power.

Money is tricky stuff. To disentangle the basic issues I recommend Geoff Ingham’s 2004 book on The Nature of Money.

“What backs fiat money?” is the question relentlessly posed by the bitcoin crowd. The question itself is a provocation. The answer that is implied is that “nothing of substance” backs fiat money, so you are foolish to trust the status quo and ought to be running for safety, buying gold and silver. Hoarding gold and silver will make you and your family into a target. So you will need a gun to protect yourselves and ample ammo. Or you could just own bitcoin …

But go back to the beginning. What is the nothing that backs fiat money? “Nothing” other than the trifling matter of tens of trillions of dollars in private credit, the rule of law and the power of the state, itself inserted into a state system. In other words the entire structure of global macrofinance.

On this score, this twitter thread is great: Trolly🐴 McTrollface 🌷🥀💩 @Tr0llyTr0llFaceThis meme of “dollar isn’t backed” just won’t die in the sterilised bubble of Bitcoin bagholders’ echo chamber. Fiat currencies are all backed by debt – very overcollateralized, even. A thread. Dollars are created when anyone – you, me, Boeing Corp – takes out a loan from a bank. March 2nd 202166 Retweets253 Likes

All money talk is political talk. Indulging silly money talk is to indulge silly and dangerous politics. We should avoid doing that.

I didn’t want to talk about bitcoin because I regard it first and foremost not so much as a technical or commercial proposition but as a conservative/libertarian efforts to escape the shadow of the political order of money that has half-emerged from the collapse of Bretton Woods. Bitcoin’s “solution” is to create an artificial scarcity founded in solving maths problems with vast computer power, consuming huge quantities of electricity, generated from coal that contributes in a non-trivial way to the climate crisis. Recent estimates put bitcoin’s current carbon footprint at c. 37 megatons of CO2 annually, the same as the emissions of New Zealand.

To paraphrase Gramsci, crypto is the morbid symptom of an interregnum, an interregnum in which the gold standard is dead but a fully political money that dares to speak its name has not yet been born. Crypto is the libertarian spawn of neoliberalism’s ultimately doomed effort to depoliticize money.

In the end, however, not talking about this morbid symptom felt like a copout. Lisa won. We did the podcast.

I thought it might be worth sharing my short crypto reading list in case others share what Germans would call my Berührungsangst (fear of touching).

***

I started by asking for advice from my expert on all things money, my dear friend, Stefan Eich of Georgetown who has a brilliant book Currency of Politics: The Political Theory of Money from Aristotle to Keynes out soon with Princeton UP.

Stefan sent me to his excellent article on the emergence of crypto out of the struggle over the politics of money in the 1970s, specifically Friedrich Hayek’s call for a fully privatized money.

Source: Bitcoin Exchange

One of the striking things that Stefan’s piece does is to reverse time’s arrow. Rather than pointing forward to the future, he highlights how crypto actually points backwards to a longing for the “time before”.

Stefan also recommended the fantastic blog by JP Koning called “Moneyness”.

In one of his most extensive and fundamental posts, Koning punctures the idea of bitcoin as a store of value or as a medium of exchange, to argue that it is basically a speculative game.

“What is now apparent is that bitcoin was never a monetary phenomenon. No, bitcoin is a new sort of financial betting game. It is a digital, global, highly-secure, and fairer version of the old-fashioned chain letter.”

What has driven the recent surge in the value of the tokens is the prospect that giant institutional investors are about to join in, which, if true, enormously increases the value of the tokens held by those who got in early on the issuance of the coins.

The question that Isabel Kaminska at FT’s Alphaville – known in general as an acute critic of bitcoin hype – has been asking, is whether 2020 was the year in which bitcoin went “institutional”.

This excellent medium post by Mike Co surveys the range of evidence up to Feb 1 of big money engaging with bitcoin. Amongst the new players in crypto, one name that leapt out at me was Guggenheim Partners, where Scott Minerd, one of the most influential dollar skeptics, is CIO.

A minimum condition for an asset to serve as a store of value is that its value cannot go to zero. As so-called “chartalists” and advocates of MMT argue, one of the key foundations of money’s value is that it serves as a means for paying taxes. In the end, along with death, taxes are inevitable. We all need money to pay them.

An entirely private system of money lacks that foundation. Or does it? As Kaminska argues, ransomware sharks now exact a form of crypto taxation. This mind-blowing passage is worth quoting in full:

In 2020, however, that doesn’t seem quite right. Private “hackers” routinely raise revenue from stealing private information and then demanding cryptocurrency in return. The process is known as a ransom attack. It might not be legal. It might even be classified as extortion or theft. But to the mindset of those who oppose “big government” or claim that “tax is theft”, it doesn’t appear all that different. A more important consideration is which of these entities — the hacker or a government — is more effective at enforcing their form of “tax collection” upon the system. The government, naturally, has force, imprisonment and the law on its side. And yet, in recent decades, that hasn’t been quite enough to guarantee effective tax collection from many types of individuals or corporations. Hackers, at a minimum, seem at least comparably effective at extracting funds from rich individuals or multinational organisations. In many cases, they also appear less willing to negotiate or to cut deals. In an increasingly polarised world where a near majority of people don’t recognise the legitimacy of their governments, a bitcoin enthusiast might legitimately question what really constitutes legal extortion anyway? When established norms are in flux, everything becomes a matter of perspective and it would be irresponsible for fiduciary agents to bet on only one horse.

Bitcoin is the scrip for the age of the digital mafia. Danegeld for the 21st century. The dark web functions of crypto are not a bug, but a feature.

Of course, bitcoin advocates prefer narratives of state-failure of a rather different kind. They liked to tout crypto as a solution for folks in distressed monetary systems.

For instance, could stablecoin play a role in supporting US policy towards Venezuela, as some boosters like to claim?

Koning does a fabulous hatchet job on Venezuela. PayPal really might have been able to organize an airdrop of currency for the Venezuelan opposition, but it did not want to put its local business at risk.

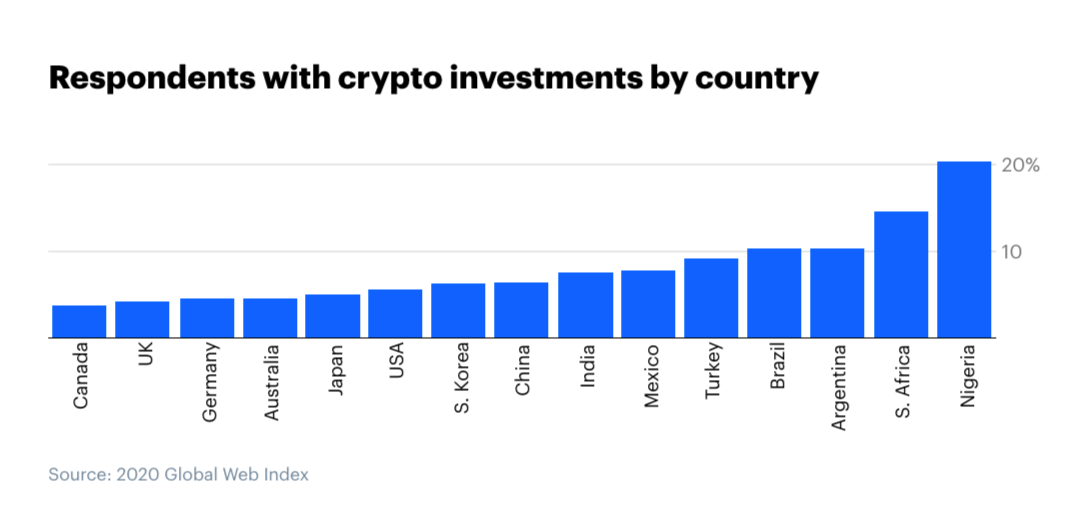

In Nigeria, another distressed economy, bitcoin does seem to play a more important role, as one of a variety of ponzi-like “investment products”. If surveys are to be believed, Nigerians are four times more likely to hold crypto than Americans.

Source: Mike Co

As Koning explains, those who gamble on bitcoin in Nigeria are not, for the most part, dupes. “The demand to play life-changing betting games gets channeled into whatever the underground market can provide, like ponzi schemes” aka bitcoin.

One can see the significance of crypto as a means of paying ransom or side stepping a rapacious state. But does it have to be an expression of state failure?

One of the reasons it was high time for me to do some bitcoin reading was to resolve a tension in my head between my aversion to bitcoin’s politics and my enthusiasm for digital banking and the idea of digital central bank currency in particular.

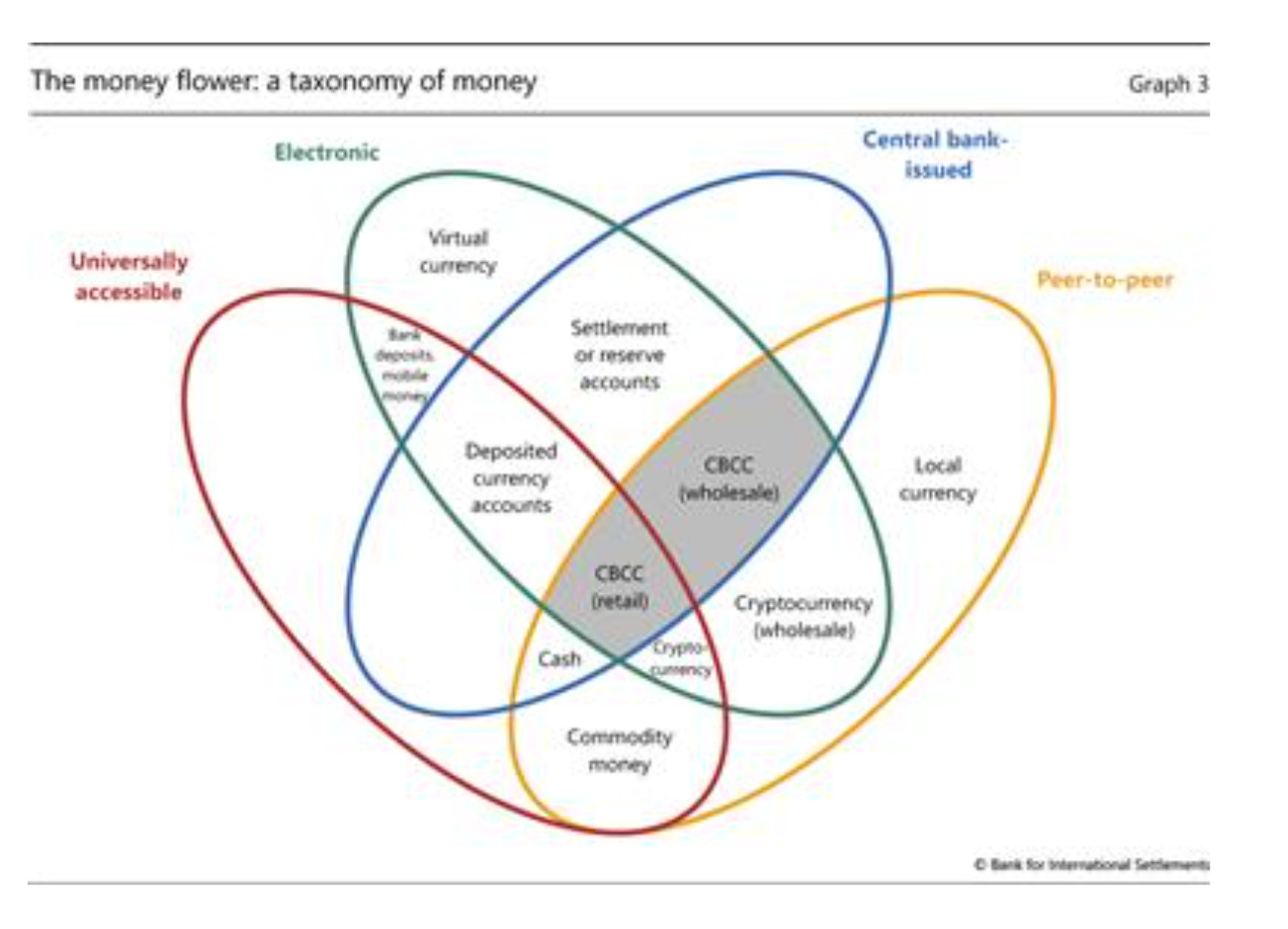

Bitcoin is really just one particular ecosystem in the much wider world of digital currencies. Predictably, the team at the BIS have provided us with the best map. They offer us what they call the “money flower”:

Source: Bech & Garratt (2017)

Crypto currencies are that niche in this new field of digital monies defined by being peer-to-peer (non hierarchical not involving central banks), electronic and universally accessible. There are many other options. For a truly deep dive I am going to have to come back to what appears to be a foundational paper by Augustin Carstens, GM of the BIS, on “Digital currencies and the future of the monetary system” from 27 January 2021. There is just too much in it, to digest here.

Digital central bank currency could very well open the door to radical experiments in fiat money. Everyone could be equipped with central bank accounts, blurring the boundary line between fiscal and monetary policy. Enabling helicopter drops of money and people’s QE, the very opposite of what the founders of bitcoin intended. Very much my cup of tea. Of course, digital central bank currency has its own political issues.

Unsurprisingly, the People’s Bank of China is a leader in the field of digital central bank currencies and the direct distribution of purchasing power to citizens. E-yuan enable complete surveillance of transactions and also cut out any potential challenge to the regime’s authority by electronic payment giants like Ant Group and Tencent. Beijing does not regard the prospect of fintech disruption lightly. As I discussed in Chartbook Newsletter #9, Beijing’s understanding of regime stability is holistic. Since 2019 crypto trading and the use of bitcoin as means of payment has been banned in China. This piece on China’s digital currency by James Kynge and Sun Yu in the FT is excellent.

One fundamental difference between central bank digital currency and bitcoin is that the former is top-down state money. The second fundamental difference is that central bank digital money is not based on a perverse model of artificial scarcity.

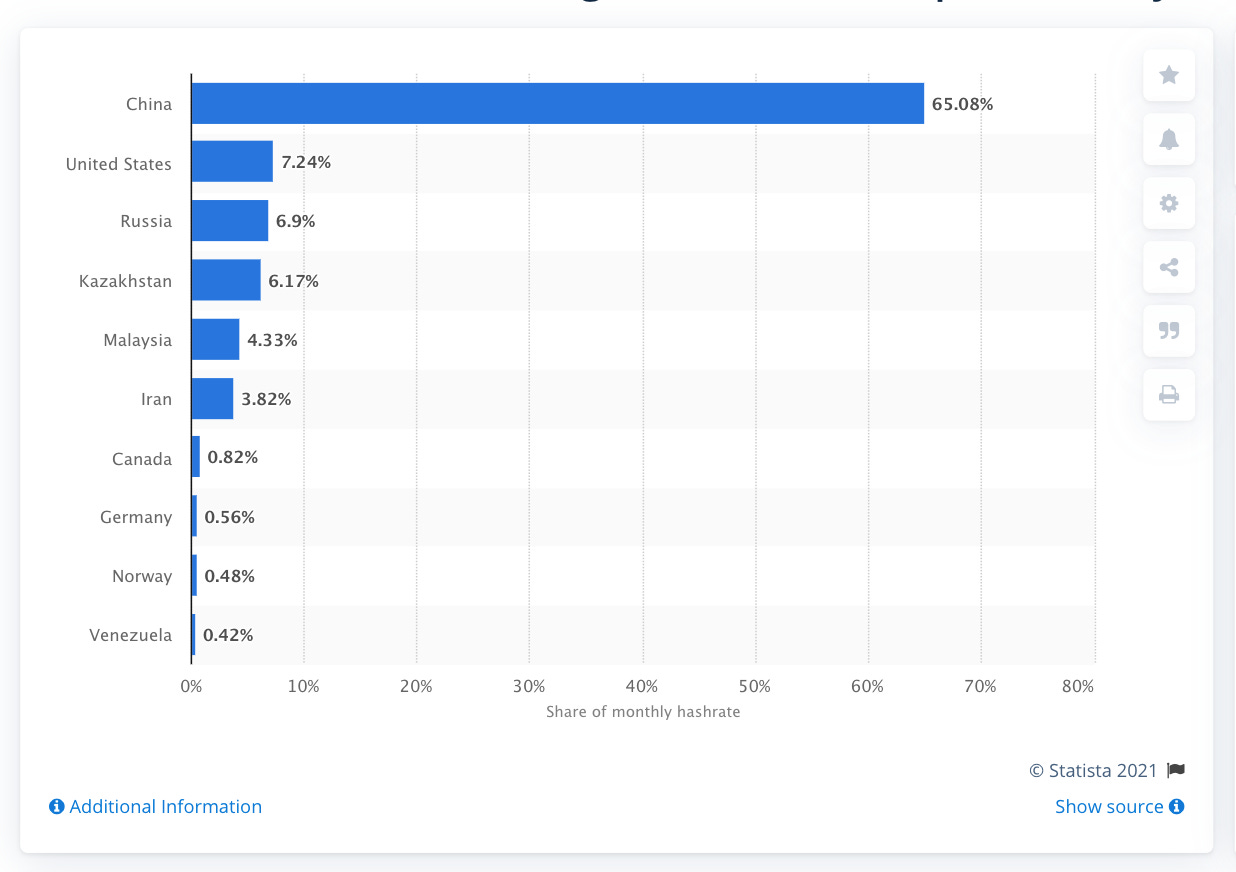

Crypto mining is deeply weird. It is expensive. It is environmentally damaging. It tends to take place where electricity is ruinously cheap. As of April 2020 most of it was done in China, mainly in the North East close to the Mongolian coal fields.

In a very promising development on March 1 2021 Frank Tang of the the SCMP reported that all bitcoin mining operations in Inner Mongolia will cease by April 2021. The region was the only one of thirty not to have met Beijing’s demand to reduce energy consumption and energy intensity. It is not compatible with Beijing’s new carbon neutrality goals.

Outside China, there are pockets of bitcoin production in many strange locations. The most extraordinary piece on the entire phenomenon which brilliantly captures the sense of cryptocurrency as a morbid symptom is this long form essay by the wonderful writer Alexander Clapp.

The single most mind-blowing piece on the weird world of crypto mining that I’ve read, came out in the summer of 20202. It’s an essay by the wonderful journalist and writer Alexander Clapp. Let’s just say that it lives up to its title!

I’ll end with Clapp’s glorious final paragraph:

“Elites and unemployed alike (in North Kosovo and along the Dniester River), now huddle around the dying embers of their gutted welfare state—the free electricity that once kept the lights on at battery factories and in mineshafts—to perform a caper on the capitalist world that triumphed over them. How ironic that they are using its greatest symbol, currency itself, to enrich themselves.”