“The market for U.S. government debt (Treasuries) forms the bedrock of the global financial system.

The ability of investors to sell Treasuries quickly, cheaply, and at scale has led to an assumption, in many places enshrined in law, that Treasuries are nearly equivalent to cash. Yet in recent years Treasury market liquidity has evaporated on several occasions and, in 2020, the market’s near collapse led to the most aggressive central bank intervention in history. … a high degree of convertibility between Treasuries and cash generally requires intermediaries that can augment the money supply, absorbing sales by expanding their balance sheets on both sides. The historical depth of the Treasury market was in large part the result of a concerted effort by policymakers to nurture and support such balance sheet capacity at a collection of non bankbroker-dealers. In 2008, the ability of these intermediaries to augment the money supply became impaired as investors lost confidence in their money-like liabilities (known as repos). Subsequent changes to market structure pushed substantial Treasury dealing further beyond the bank regulatory perimeter, leaving public finance increasingly dependent on high-frequency traders and hedge funds—“shadow dealers.” The near money issued by these intermediaries proved highly unstable in 2020. Policy makers are now focused on reforming Treasury market structure so that Treasuries remain the world’s most liquid asset class. Successful reform likely requires a legal framework that, among other things, supports elastic intermediation capacity through balance sheets thatcan expand and contract as needed to meet market needs.”

This is the abstract for an essay modestly entitled “Money and public debt: Treasury Market Liquidity as a Legal Phenomenon” – the latest block buster collaboration from Lev Menand of Columbia University and Josh Younger (ex of JP Morgan now NY Fed) – in the Columbia Business Law Review.

My aim here is to amplify their crucial arguments. Everyone interested in global finance should read the article. If you are looking for a shorter summary, read Alexandra Scaggs’s excellent piece at the FT.

***

The essential starting point of the Menand and Younger account is the basic insight that

American public finance has long been closely intertwined with the American monetary framework and that deep and liquid Treasury markets are, in large part, a legal phenomenon. Treasury market liquidity, in other words, did not arise organically as a product primarily of private ordering. Instead, it was actively constructed by government officials. The high degree of convertibility between Treasury securities and cash—the market’s “liquidity”—depends upon entities that can create new, money-like claims to buy Treasuries. Sometimes the government’s central bank has issued these claims directly, as in March 2020; other times these claims were issued by central bank-backed instrumentalities, such as banks and select broker-dealers.

They connect here to three important strands of thinking about money and finance: the idea that the state money-finances its spending (MMT/Tankus et al), the political economy of financial markets (Braun, Gabor et al), the legal construction of finance (Pistor et al).

The key point is that the issuance of public debt goes in hand with the issuance of credit and money in a public-private partnership.

United States has never relied exclusively, or even primarily, on money instruments issued directly by government agencies. Instead, since the Founding, the government has outsourced money augmentation. By design, investor-owned enterprises—typically, chartered banks—have been the predominant money issuers in the economy. And the federal government, recognizing this, has set terms and conditions for their money creation.

The early stages of America’s modern monetary history nicely illustrates the point.

Between 1863 and 1916, Congress established a network of investor-owned federal corporations—national banks—to serve as the country’s primary money-issuing institutions and required that these instrumentalities back their paper notes with Treasuries. … In doing so, the federal government conjured captive demand for federal debt. Although, under the resulting legal regime, the government formally borrowed to manage deficits, it borrowed in significant part by selling Treasuries to national banks, which, in turn, funded their purchases with newly issued notes and deposits.

After the establishment of the Federal Reserve in 1913 and under the pressure of World War I finance,

Congress adjusted the law so that the Fed could incentivize banks to purchase Treasuries with newly issued deposits. Under this second configuration, government officials actively managed debt monetization by deposit-creating banks. Less than thirty years later, when the U.S. joined the Allied effort in World War II, the Fed went even further. It bought large quantities of Treasuries directly and administered prices for Treasury debt, pegging short-and-long-term Treasury rates using its own balance sheet—monetary finance ..

Up to 1951 there was thus a relatively direct conveyor belt that shuffled initially small volumes of debt and then (with the world wars) larger volumes directly onto the balance sheets of state-backed banks with money issuing privileges, or commercial banks that issued credit to their private clients and were back-stopped by the Fed.

As Menand and Younger highlight, the elasticity of the system in the 1940s was spectacular:

In total, the stock of … direct obligations of the government more than doubled relative to economic activity—from 43% of GDP in 1939 to more than 110% in 1945. To put this in a more recognizable, modern context, if we size a similar program to 2019 GDP it was as if the Treasury was able to issue more $40 trillion of new Treasuries over just a few years.

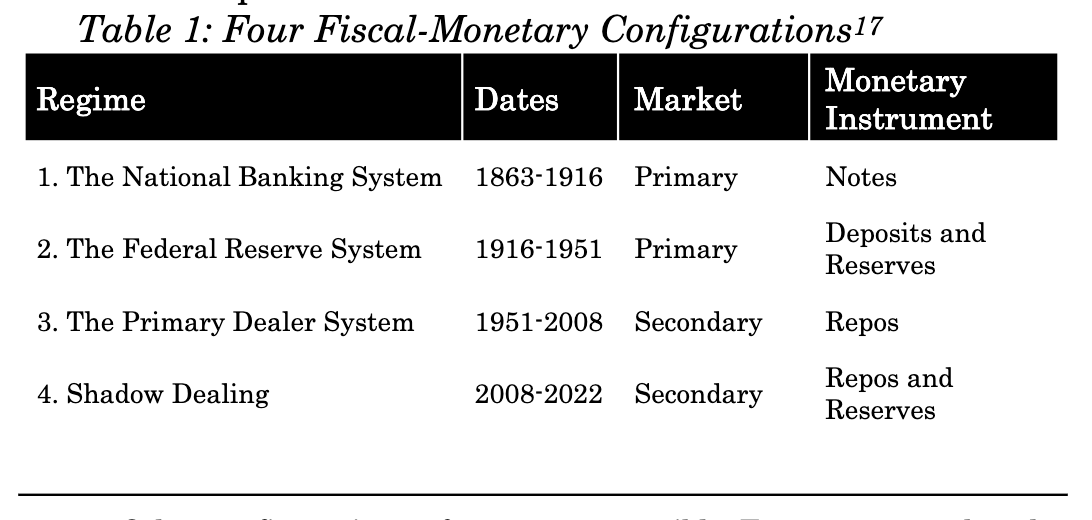

Up to the mid-century, secondary markets for already-issued government debt, what we think of today as the “bond market”, did not play a major role in the US monetary and fiscal nexus. In the 1950s this changed, with a deliberate policy decision to shift conduits of Treasury financing away from bank balance sheets attached to the Fed and instead to place Treasuries, through the capital markets (where bonds are bought and sold daily) with a much wider array of investors. This decision was motivated by the realization that a system for absorbing Treasuries based on bank balance sheets, left the banking system “clogged up” and inelastic.

Menand and Younger illustrate the shift in the debt-money nexus from a bank to a capital market model with a dramatic graph. Before 1914 almost two thirds of America’s very limited public debt was held by banks. By the early 2000s banks held a tiny fraction of a gigantic debt pile.

**

It might be tempting to think of this switch from banks to capital markets, as a retreat by the Fed. But not only did the Fed’s share of public debt ownership barely decline after World War II, but as Menand and Younger show, it was the Fed that was key to enabling the vast bulk of US Treasuries to be held outside the US banking system, through a new set of relationships with participants in capital markets.

As a major hiccup in 1953 revealed, for a large and dynamic market in Treasuries to be other than dysfunctional, it needed backstops and this required “creative lawyering and ongoing government support”. And so, to help stabilize the new market for Treasuries, the Fed set about developing and supporting the sale-and-repurchase agreement, or “repo.”

A repo is economically equivalent to a secured loan but structured as a sale of a bond combined with an agreement to repurchase that bond at an adjusted price on a date specified in advance. When the first and second transaction in a repo are spaced a day apart (and made exempt from the bankruptcy process), repos function (in certain respects) like bank deposits. Dealer firms, therefore, could conduct overnight repo transactions primarily with nonbank corporate “depositors,” effectively money-financing their operations.

The new role of the Fed as manager of the capital market-Treasury funding mechanism rather than the bank-based-Treasury funding mechanism, was to backstop the repo market.

The Fed did not indiscriminately extend this support to all comers but instead designated an inside group of “primary dealers”. Initially there were 18 primary designated in 1960. The number grew to 46 by 1988 before declining to 21 in 2007.

These were not high street banks benefiting from deposit insurance and intensive regulation, but market-facing investment banks – both US and foreign – and bond dealerships. Their access to Fed repos meant they could build a deep and liquid market for end-investors to buy Treasuries in the safe knowledge that they could always be repoed for cash with the primary dealers, with the Fed acting as the guarantor of the final link in the chain.

Developed with active Fed backing and defended against obstructive regulatory changes – crucially to exclude repoed collateral from any bankrupty proceedings – the repo system expanded “from roughly $2 billion in the early 1960s, to $12 billion in the late 1970s, to more than $300 billion in the mid-1980s.” From there it continued to progress.

The Fed-backed, primary dealer-managed Treasury market, operating on the basis of repos, was the anchor not just of America’s financial system, but that of the entire capitalist economic world. In the 1980s, 70-80 percent of reserves worldwide were held in dollar-denominated assets. Treasuries were the most liquid and widely traded US asset for foreign reserve holders. And roughly 30 percent of US Treasuries outstanding were in non-American hands.

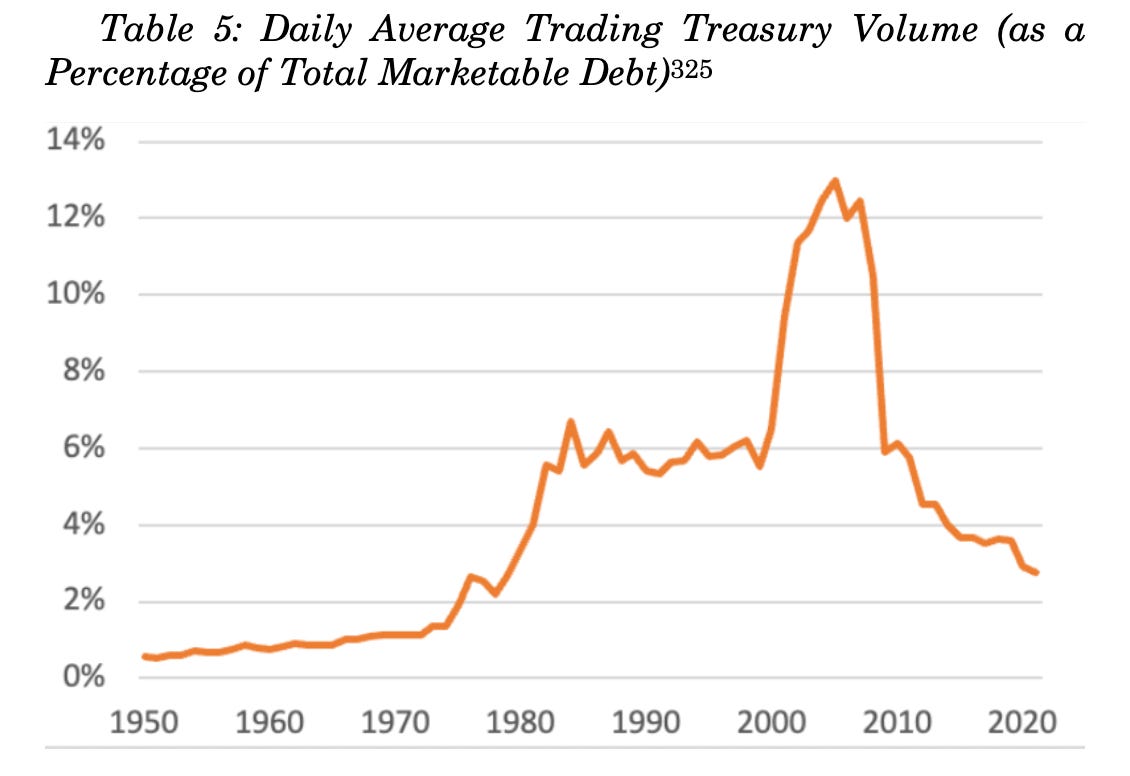

By the early 2000s, with private bonds, and large packages of mortgage-backed debt entering the system, the repo market was churning many trillions of dollars in credit per day. In 2007 daily turnover reached a remarkable 13% of total marketable Treasury debt. And the primary dealers were operating with leverage of 47x their capital base. Despite the huge volumes and the hair-trigger responses of a market that was in effect offering trillions of dollars in overnight finance, the risks seemed manageable because, in the last instance, a primary dealer could always access the Fed backstop for their Treasury portfolio.

It was this system that imploded in 2008, with huge “runs on repo” the most famous victim of which was Lehman.

Through massive liquidity provision the Fed prevented a total collapse. But, though this forestalled an implosion, the pre-2008 structure did not survive. The elite group of primary dealers were shaken to their foundations and over the coming years, they either folded (Lehman) or were bought out and absorbed by bigger banks (Bear Stearns by J.P. Morgan Chase, Merrill Lynch by Bank of America), or formed their own bank holding companies (Goldman Sachs and Morgan Stanley), thus coming under the protection of deposit insurance and comprehensive bank supervision.

As Menand and Younger comment: “Though smaller dealers remained independent (e.g., Jeffries, Cantor Fitzgerald), for the first time in modern financial history (i.e. since the formation of a large secondary market in Treasuries in the 1950s) the majority of dealer activity was performed within BHCs.” The capital market-based-non-bank-primary dealer model first shaped in the 1950s was finished.

**

Though in the aftermath of the 2008 financial crisis much attention was paid to the systemic stability of the banking system, what received less attention was the stability of major financial markets. And yet the implications of regulatory change for banks for the wider markets was significant.

Having been absorbed into the banking system, the primary dealers fell under far more strict regulations applying to Bank Holding Companies and then to the global Basel III rules. To reduce the risk of a systemically important mega-bank getting into serious trouble, these regulations were designed to dissuade big banks (which now controlled the primary dealers in Treasuries) from engaging in very high volume, highly leveraged, low margin business, like running large repo books. This reduced the elasticity of the Treasury markets.

Despite the huge surge in Treasury issuance with gaping Federal deficits after 2008, this increasing rigidity in the capital market was not immediately obvious for two reasons.

First, the Fed was itself buying Treasuries in huge volumes.

Second, new financial actors emerged to take up some of the market vacated by the more tightly regulated bank-primary-dealers. As Menand and Younger put it:

new actors further beyond the bank regulatory perimeter, high-frequency traders (HFTs) and hedge funds, stepped in. Some refer to these entities as “shadow dealers,” as they are incentivized to serve the same economic function as dealer firms but are not currently subject to regulation as dealers (and are not required or expected to support the market to the same extent as dealers).

The growth in the new non-bank “shadow dealers” kept the market functioning, but from 2017 onwards pressures increased.

The Trump tax cut pushed the Federal deficit from 2.4% of GDP in 2015 to 4.6 % in 2019, an unprecedented number at a time of near full employment. Public debt in private hands increased by $2.7 trillion from 2017 to 2019. At the same time, the Fed was unwinding its QE purchases and America’s big banks had no appetite to expand their holdings of Treasuries. Increasingly, the Treasury market migrated back towards lightly regulated non-bank players.

Into the place of the old primary dealers stepped so-called principal trading firms (PTFs) and other high-frequency traders (HFTs) that earned margins on trade matching. At the same time hedge funds devised new strategies that incentivized them to hold long positions, effectively functioning as inventory managers for the market. Hedge funds gobbled up whatever balance sheet capacity was offered to them by the big banks, for fearing of losing their “allocation”.

The result was a build up of Treasury holdings in the hands of lightly regulated but highly leveraged balance sheets. Menand and Younger summarize as follows:

SEC Private Funds Statistics … show a rapid increase in gross exposure to Treasuries among the hedge funds in their sample, which had remained around $1 trillion from early 2014 (the earliest data available) until the fourth quarter of 2018,367nearly doubling to $2.2 trillion by the end of 2019.

It was this fragile patchwork of bank and non-bank actors in the US Treasury market that imploded in March 2020 under the impact of the COVID shock. Menand and Younger offer by far the most compelling account of the Treasury market dysfunction of March 2022 to date. I reproduce here only the briefest summary:

… in 2020, the onset of the pandemic revealed that shadow dealers, which were often much more thinly capitalized than commercial banks and lacked explicit or implicit access to central bank backstopping, were extremely vulnerable to run-like dynamics in the face of market volatility. Just when private intermediaries, including hedge funds and high-frequency traders as well as securities dealers, were most needed to warehouse a deluge of sales by end-investors in a largely one-sided market, these firms stepped back in unison.

Menand and Younger hedge their bets on the role of the big bank-primary dealers in the March 2020 spasm.

Size constraints may not have been strictly binding on the banking system or individual bank holding companies at the time, but they created a brittle internal arrangement that acted as an amplifier of market volatility.

Younger had a front seat in the action at JP Morgan and he did a huge service to the analytic community at the time with his commentary on market dynamics.

In any case, the role of particular big banks is not the key issue. From a historical point of view the key point is that under massive stress, the basic legal, financial and, ultimately, political structure that underpins the interlinked public and private system of money and public debt was starkly revealed:

The day was saved only by a dramatic intervention by the Fed, which used its balance sheet to absorb supply and smooth out price fluctuations. It was what Chairman Martin (chairman of the Fed between 1951 and 1970) had aimed to avoid: direct central bank intervention undergirding federal finance.

**

The disturbance of spring 2020 was both profoundly alarming and dangerous. Whether you regard the denouement – direct Fed stabilization – as a disaster depends on your worldview. It depends on how squarely you are willing to face the historical fact that our modern monetary and fiscal constitution profoundly entangles the state and the private financial system and it is the central bank that forms the ultimate backstop. You can reasonably advocate for a system that is even more transparently backstopped by the central bank. You can also reasonably prefer a new iteration of public-private partnership with new rules, new participants and new backstops. What Menand and Younger’s wonderful essay shows to be a fantasy is any idea of a fiscal and monetary system based on rigid separation, a “free” capital market, or a “privatized” money supply.

As Menand and Younger conclude, these questions are urgent. We are entering

… a critical phase in the financial history of the U.S. and the dollar. The trajectory of mandatory federal spending points to a secular widening of deficits over the medium-to long-term. Ensuring markets keep pace with that growth remains, as Chairman Martin observed back in 1959, “obviously needed for the functioning of our financial mechanism.” Absent reform, one possibility is another panic.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you will receive the full Top Links emails several times per week.