When was the era of Bretton Woods? This might seem like a trivial question with a simple and familiar answer. But on closer inspection it reveals itself to be a rabbit-hole of narrative uncertainty. Nor is this merely a scholastic debating point. Exploring it reveals a lot about how we think about power and how we write its history. The politics of power and history are very much to the fore in the current moment as we digest the bold claims made for Biden’s industrial policy, Jake Sullivan’s declaration of a “new Washington consensus” and the rumored demise of neoliberalism.

Should progressives be heeding the call of history and throwing their weight behind shaping the agenda of the new era? Or is caution warranted? Is the rhetoric of novelty and historical change deceptive? Do we continue to live, as formidable critics like Daniela Gabor insist, under the auspices of the de-risking state and the Wall Street consensus? These questions update and give urgency and actuality to older questions of how we, defined by our respective social locations, identities and interests, relate to narratives of economic order and the history of economic policy. Heroic periodization, labels like the era of Bretton Woods, or the Washington consensus, matter.

***

I was prompted to think about these questions by reading Martin Daunton’s The Economic Government of the World, 1933-2023 which I reviewed for the FT and will likely become an essential reference. Daunton’s book paints the history of global economic policy over a pullulating, 90-year historical canvas. The “postwar” era is at the heart of his narrative and Daunton’s account offers what I take to be a post-heroic, realist account, well-suited to our times.

Most people who are not deep in the weeds of monetary or financial history, would probably say that the era of the Bretton Woods system, which pegged the dollar to gold and the other major currencies to the dollar, extended from the United Nations Monetary and Financial Conference held at Bretton Woods, New Hampshire from 1–22 July 1944, to March 1973 when the postwar monetary system came to an end.

Others might quibble and say that Bretton Woods ceased to function in all but name on August 15 1971 when President Nixon announced that he was unilaterally abandoning the gold convertibility of the dollar.

Either of these conventional datings, anchors the idea of a “postwar golden age”, stretching from 1945 to the early 1970s. In French the period is sometimes labeled the “trente glorieuse”.

The currency system of Bretton Woods with its network of fixed exchange rates bolstered by restricted capital mobility, is thought of as having provided a propitious environment for high investment, growth, full employment and win-win wage-price-profit trade offs. The idea behind Bretton Woods was to avoid the disastrous trade offs imposed by the 19th-century gold standard between external currency stability and domestic economic and social welfare. This aligns the idea of an era of Bretton Woods with the narrative of the “Keynesian revolution” in economic policy and the idea that the postwar era was one of “embedded liberalism”. That in turn serves as the backdrop to narratives which see the terminal crisis of Bretton Woods in the 1970s as the birth moment of a new era of capital mobility, financialization, market economics, neoliberalism, inequality, deindustrialization and large-scale unemployment. The current excitement about the new era of industrial policy, summons us to attend to the dawn of a new era of economic policy, of similar historical standing.

***

Broad-brush historical narratives of this type have a life and significance of their own. They legitimate and motivate action.

For critics of the neoliberal era and hyper-globalization, Bretton Woods has become something of a rallying call. From both the center right and left came calls for a “new Bretton Woods”, whether in the form of a reformed World Bank and IMF, or, more ambitiously, for a restoration of managed exchange rates, capital controls, or taxes on capital mobility. In 2009 Zhou Xiaochuan Governor of the Peoples Bank of China called for a new Bretton Woods to adjust the global currency system to a system no longer anchored on the dollar.

Such political uses of history are all well and good. But one cannot help wonder at the gap between the actual reality of monetary and economic policy in the years after World War II and the cliché that is made out of that history. One cannot help wondering, also, about the practical and political conclusions that are drawn from that cliché.

I’ve long marveled at the myth of Bretton Woods. Indeed, it has been a recurring theme in these newsletters and the blog that went before it. Daunton’s history highlights once again the huge gap between reality and the slab-like chronologies of the world economy that organize much public discourse.

To avoid misunderstanding, the point is not that good history shows that “everything is more complicated” and that greater levels of detail are better than simplification. Let alone some silly academic back-biting between historians (who do archives and detail and complexity and people) and social scientists (who do big concepts and simplification and grand social forces).

The question is how power and specifically monetary power and the dollar-system in particular have actually operated since 1945 and which general models of history are most useful as first order approximations. Is the story of the global monetary system best thought of as one of cooperation and harmony, or one of conflict, hegemony and power? Should we think in terms of long phases of stability and order punctuated by crises? Or is it, instead, better to track a story of continuous adjustment? Is it a story of established hegemonies? Or one of continuous improvisation? How does that in turn help to orientate a promising strategy and tactics of global monetary and financial reform?

What Daunton’s history shows is that the nostalgic, reconciled, hegemonic, order-centric view of the governance of the world economy, as a succession of distinct phases each with its own distinct and proper logic, is a long way from reality. If we care about actually understanding how we have arrived where we are at, we should prefer a vision of monetary, financial and trade systems that prioritizes power, improvisation, linkages between the domestic and the international, improvisation and American unilateralism. And that has implications too for how we should think of the current moment.

***

One particularly egregious and telling misreading of history is the idea that Bretton Woods and GATT emerged from a cooperative “postwar settlement”. This is Klaus Schwab’s take from 2019.

In fact, as Daunton shows, Bretton Woods and postwar trade politics were creations of the war itself. They were forged in the power-relations of the Allied coalition against Hitler’s Germany and Imperial Japan. They took the sweeping and grandiose form that they did, because the backdrop was the war economy in which market-based trade and financial relations were suspended and the very foundations of the monetary system and the global division of labour were up for grabs. To wish for a “second Bretton Woods” is a fantasy that, if we take it literally, should fill us with horror. It is to imagine the financial and economic conclusion to World War III.

As Daunton shows, as soon as the global conflict of World War II ended, the relatively easy cooperation between the United States and the British Empire broke down, giving way to tough bilateral debt diplomacy, painfully reminiscent of the disastrous aftermath of World War I. It was brutal financial arm-twisting not sweet cooperation that set the time table for the first effort to implement Bretton Woods in the summer of 1947 by establishing the convertibility for the pound sterling, putatively the strongest currency in Europe. Within a matter of weeks it was clear that it was a recipe for disaster. Controls were reimposed. As a postwar project, Bretton Woods was a non-starter.

The Marshall Plan of 1947 was not the complement to Bretton Woods. The merger of the two into a single narrative of benign US hegemony, is another facet of the postwar imaginary which turns reality on its head.

The Marshall Plan was the improvised and contentious response to the fact that reconstruction plans hatched during the war, like Bretton Woods, were clearly out of touch with the realities of a ruined and crisis-torn world economy. The need for a new policy was made all the more urgent by escalating tension with the Soviet Union, tensions which had not yet been envisioned in July 1944, but which were essential to propelling the Marshall Plan and which the Marshall Plan itself further exacerbated.

After the shock of the sterling crisis in 1947 and the escalation of the Cold War, further steps towards monetary integration by way of currency convertibility confined themselves to Europe itself, much to the horror of American liberals and free-traders everywhere. The European Payments Union between 1950 and 1958 could be thought of as a mini “European” Bretton Woods. But it excluded the United States and shielded the Sterling area.

Bretton Woods did not finally come into effect until 1958 with the convertibility of the major currencies within the “Western” bloc. Bretton Wood started thirteen years after 1944 and in a completely different world. And as soon as it did, major tensions became evident.

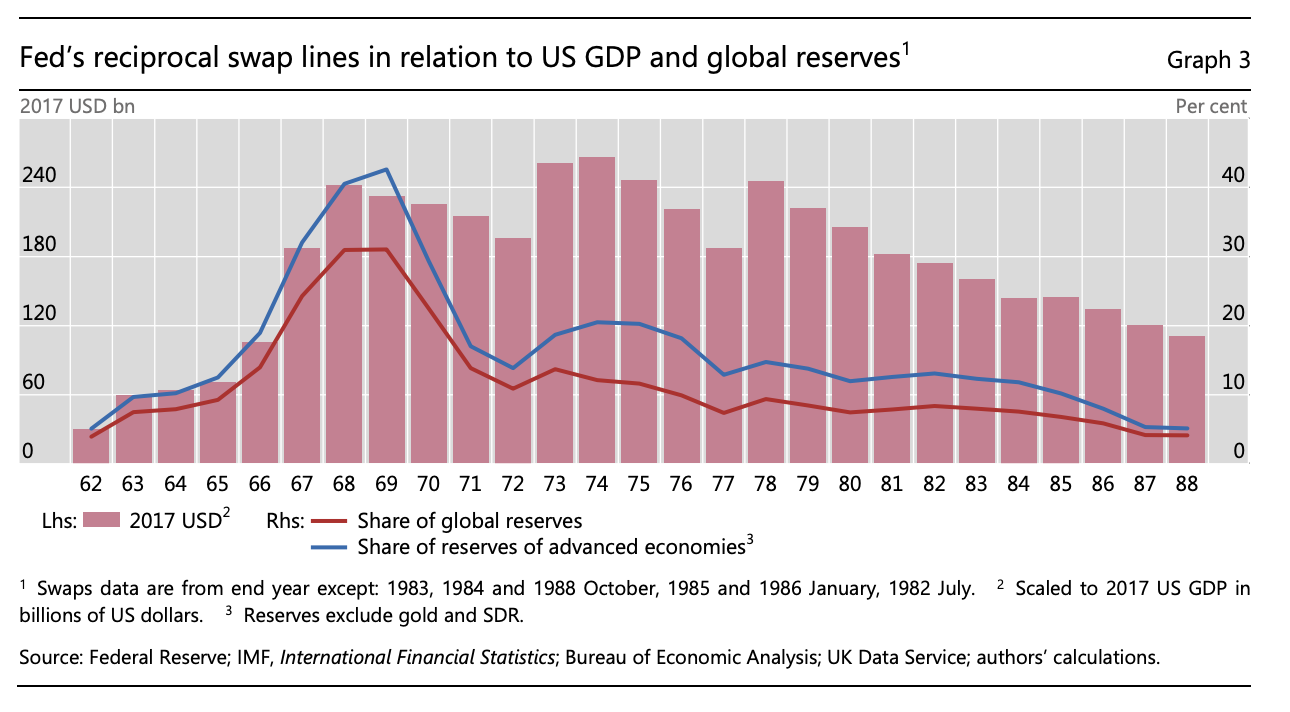

As Robert N McCauley and Catherine R Schenk show in their fascinating work on swap lines in the 1960s, from 1962 onwards, the Bretton Woods system was underpinned by a complicated network of mutual central bank support. The amounts outstanding on the Bretton Woods swap line system surged in the course of the 1960s to a quarter of a trillion dollars in 2017 terms, comparable to the amounts that were outstanding during the onset of the 2007-8 crisis.

These swap lines helped to hold the system together. But already by 1964 the value of official dollar liabilities held by foreign monetary authorities exceeded that of the US monetary gold stock. This undermined the basic stability of the gold-dollar peg.

In 1967 the pound sterling was forced into a nail-biting devaluation, which left the dollar so exposed that in March 1968 the Gold Pool was disbanded. Though the US currency remained nominally attached to gold, the US administration intensified its efforts (which began already in the early 1960s), to dissuade other central banks from actually converting dollars into gold. What Nixon announced in August 1971 simply made explicit what had been evident since at least 1968: the Bretton Woods system was unworkable.

What, during its brief period of operation, made Bretton Woods so fragile, were incompatible national economic policies (too much stimulus in the United States), beggar thy neighbor export-centric development strategies pursued by Germany and Japan, but also the revival of Wall Street’s global ambition. Wall Street had never been reconciled to the curtailed Keynesian vision of international finance that Bretton Woods nostalgics hanker after. As Eric Helleiner showed, the impatient bankers of New York had powerful sympathizers in the US Treasury, and the creation of the offshore eurodollar market was eagerly welcomed, as Jeremy Greene has shown, by the British authorities in the City of London. It was not just macroeconomic imbalances and democratic deficits that destabilized Bretton Woods. It was undermined from within by the North Atlantic nexus of state and financial power that was crucial to world history from 1916 onwards.

What these underlying disharmonies, discrepancies and contradictions point to, is that formal agreement is one thing – whether it be the original Bretton Woods deal in 1944 or the decision to move to convertibility in 1958 – but mobilizing a power bloc in support of those decisions that is capable of sustaining not just formal compliance but cooperative behavior, is quite another. And this reality checks applies both to international economic policy and to the necessary agreement at the national level. It is not clear that Bretton Woods ever enjoyed stable elite buy-in, for precisely the reasons one would imagine from the enthusiasm with which progressive still today invoke the Keynesian idea of capital controls. As Perry Mehrling has recently argued in his intellectual portrait of economic historian Charles Kindleberger, the true undergirding continuity of international finance were not inter-governmental arrangements about national currencies, but the interlocking balance sheets of private finance stretched between the City of London and Wall Street. These made the Bretton Woods system increasingly unworkable by the late 1960s but they also ensured that the end of the system in the early 1970s did no produce a bottomless collapse of the dollar.

***

So this question – when was the era of Bretton Woods? – is, in fact, anything but simple. And its implications for how we think about global political economy are clearly non-trivial.

The answers we give have a “now you see it, now you don’t quality”. The very longest you could possibly claim for the actual existence of Bretton Woods would be 1958 to 1973 and that involves glossing over the chronic crises of 1968-1971. The decade from 1958 to 1968 would actually capture something like the Bretton Woods system as originally conceived in routine operation. Reduced to a span of ten years this leaves precious little of the “trente glorieuse”. Viewed from that angle, perhaps. the currency system has less to do with economic growth than we commonly imagine. And if you look inside the boiler room of Bretton Woods, as Daunton allows us to do, that sense of disconnect is even stronger. Already in early 1960s the system was in disequilibrium and sustained by continuous improvisation. At which point one has to begin to wonder wether referring to a Bretton Woods system really makes that much sense at all.

The realist response might, indeed, be to dismiss the historical significance of Bretton Woods altogether. A prophet of market economics like Milton Friedman who was an early and vocal advocate of flexible exchange rates, might contend that the entire project was quixotic from the start and it was only a matter of time before it disintegrated and gave way to something more adaptive and more clearly driven by the collective wisdom of the invisible hand and the force of rational self-interest. Given the course of history, the least that can be said for this point of view is that it rationalizes what actually did occur from the 1960s onwards with the development of the offshore eurocurrency market and the move to floating exchange rates in the 1970s. That, however, was not natural artifact of a human proclivity to truck and barter but the result of lobbying by interests on Wall Street and the City of London.

This brings us to the mirror image of the Friedman position on the left. This argues that the contradictory dynamic of capitalist development, so long as it remains untamed, is bound to render any effort at state regulation, bounded, crisis-ridden and ultimately ineffectual. The way forward is, therefore, to mobilize progressive political forces to overcome the contradiction that lies in the private profit-driven system of credit, money creation and global finance. This pushes for a state-driven credit system, which can then be effectively managed because the underlying source of incoherence has been removed. The last historically significant effort to realize something along these lines in the West was probably the Mitterand government in France that engaged in wholesale nationalize of the commanding heights of the French financial system. It is a project that was abandoned by 1983 under huge pressure from bond and currency markets, that over the preceding years had been roiled by inflation and the aggressive interest rate policy of the Fed, the Bank of England and the Bundesbank.

From either of these positions, in light of the actual history of monetary and financial relations between 1944 and 1973 you might be tempted to relegate Bretton Woods to the dusty chamber of historically transient and largely irrelevant episodes. After all a system as ephemeral as this can hardly have been a significant force shaping postwar growth. The scrambling efforts to keep it alive between 1958 and 1973 distorted markets and created perverse incentives.

One can discern echoes of this kind of roundhouse, knock-down critique in debates going on right now about our own moment of economic policy transition – the new era of industrial policy.

For critics from within the old mainstream, the “new” industrial policy is not “new” at all. It is yet another costly and inefficient abandonment of market logic. It isn’t the first and it won’t be the last. For critics from the left as well, any claim to novelty is overstated. What we are witnessing is just another iteration of de-risking and public-private partnership, the basic operating logic of late neoliberalism since the 1990s.

But if we return to the Bretton Woods case, the one-sidedness of this kind of critique becomes evident. Because, after all, between 1944 and the early 1970s though the idea of a stable fixed exchange rate system based on the dollar was to a degree always a fugitive vision, it remained a point of orientation, something to work towards, or to try to make work. Restrictions on capital mobility were real. The succession of makeshifts put in place until the early 1970s did facilitate a rebuilding of the European and Asian economies. In the same way the ideas of a green energy transition, of friend-shoring, of rebalancing the economy towards workers are best thought of as forming a new horizon, towards which policy is directed.

The mistake is not to take Bretton Woods seriously. The mistake is to treat it as an accomplished and established fact rather than as a project that continuously fails and demands adaptation and improvisation. The same is no doubt true of the New Washington Consensus.

Reading Daunton reminded me of my encounter with Tim Geithner – veteran of 2008 and 1990s crisis fighting – in the torrid early days of the Trump administration. Looking back regretfully, Geithner spoke of “defying gravity” as the Leitmotif of his generation of US globalizing policy-makers. I took “defying gravity”, the scrambling effort to assemble domestic coalitions amidst the United States’s violent and fraught entry into the 20th-century, as the motif for the LRB lecture on American power which I was privileged to give in 2019.

In the era of Bidenomics, the IRA, and yet another debt ceiling stand off, I still find the image compelling of American policy-making making repeated efforts to defy gravity. I will expand on that theme with regard to the new era of industrial policy, in a subsequent post.

The version of policy-making and economic order not as established fact, but as iterative efforts at intervention and reform opens the door to those on the left who have not despaired of actually improving and influencing policy as it is made within existing processes. The problem is how to engage with the continuous process of policy-making improvisation without becoming seduced by its Sisyphean heroics, the sheer complexity and technocratic fascination of its procedures, or the more or less hidden configuration of interests that underpin it and limit its efficacy. The era of Bretton Woods may continue to inspire those who crave a more orderly global financial system, but it also provides plenty of examples of precisely these logics of capture at work. The defense of Bretton Woods inflicted huge damage, notably on social democratic governments in the UK.

This is where critical histories, including those of the most recent past, which debunk simple visions of the past and offer a more complex view of how power operates in practice, may prove useful for those engaged in the risky business of trying to influence actually existing policy processes. A healthy start, in the present moment, would be to resist the bait offered by Jake Sullivan and his speech-writing team. Foreswear any talk of a new Washington Consensus before we become too attached to it. Stop either heroizing or demonizing the Inflation Reduction Act. Preserve a sense of proportion when it comes to claims for the IRA’s quantitative significance and never forget the circumstances of the IRA’s birth, in a gut-wrenching compromise between Joe Manchin and corporate energy interests. That would be the start for a realistic account of our present moment, that neither flattens the flux of history into an endless repetition of the same, nor succumbs to the temptation of heroic periodization.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation, you will receive the full Top Links emails several times per week.