How is the path of globalization shifting?

Ian Bremmer, Ngair Woods, Niall Ferguson and I debated this at Davos. I continued the train of thought in the FT and in Chartbook #192. Nothing could delight me more than the fact that this inspired Hyun Song Shin of the BIS to give a new outing and an update to his fundamental paper on how to envision globalization: as an island model or a network of balance sheets and how to connect financial and real economic globalization.

The first iteration of this paper appeared as I was finishing Crashed. It really fired my imagination. Hyun Song Shin’s argument is just as interesting and pertinent today.

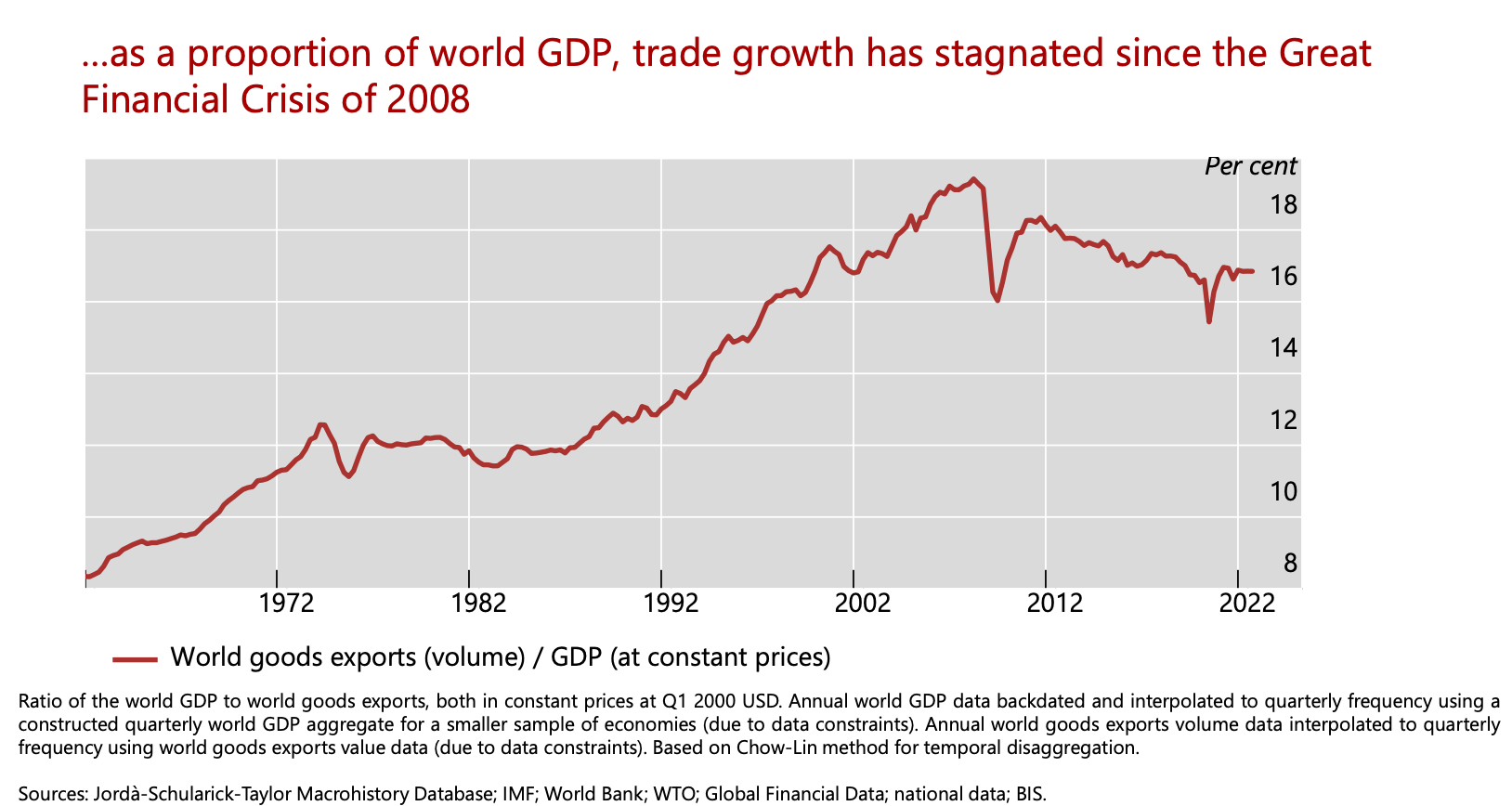

Shin starts with some basic observations about the trajectory of trade, which certainly suggest that something happened to globalization around 2008. Shin refers to what has happened since 2008 as stagnation. This seems rather polite. It might also be called a regression. World goods exports in relation to GDP are now back to where they were in 2000. This is not so much slowbalization as slow-deglobalization.

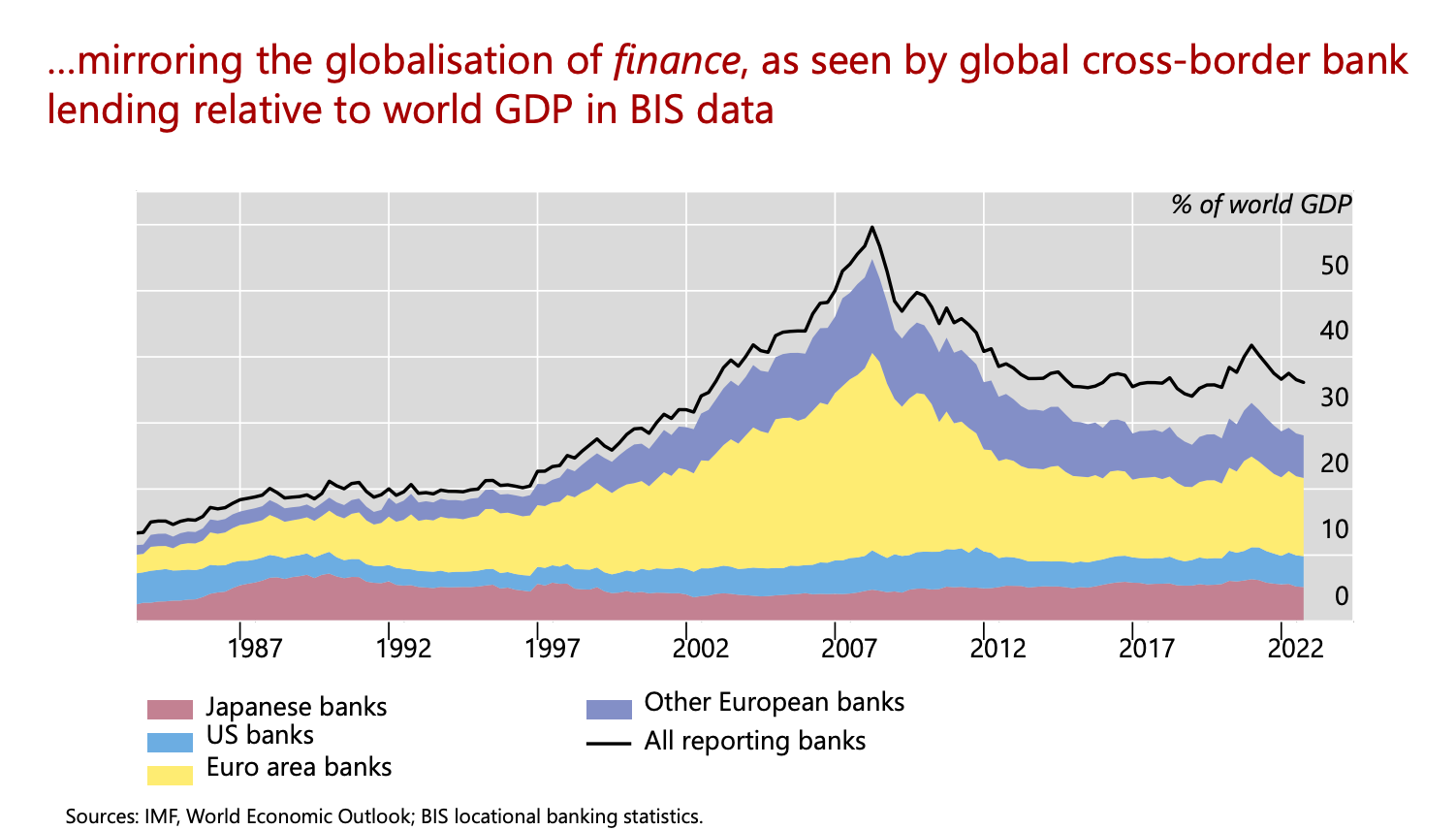

Shin connects this regression in trade to a parallel regression in the degree of financial globalization as measured by global cross-border bank lending. In 2008 this touched 60 percent of global GDP and now has fallen back to c. 37 percent.

For Shin this is related to the extension and contraction of value chains.

Value chains involve complex mediated linkages between a series of sub-contractors. Credit financed those transactions. “Real” and financial globalization are not separate processes but tightly interlinked.

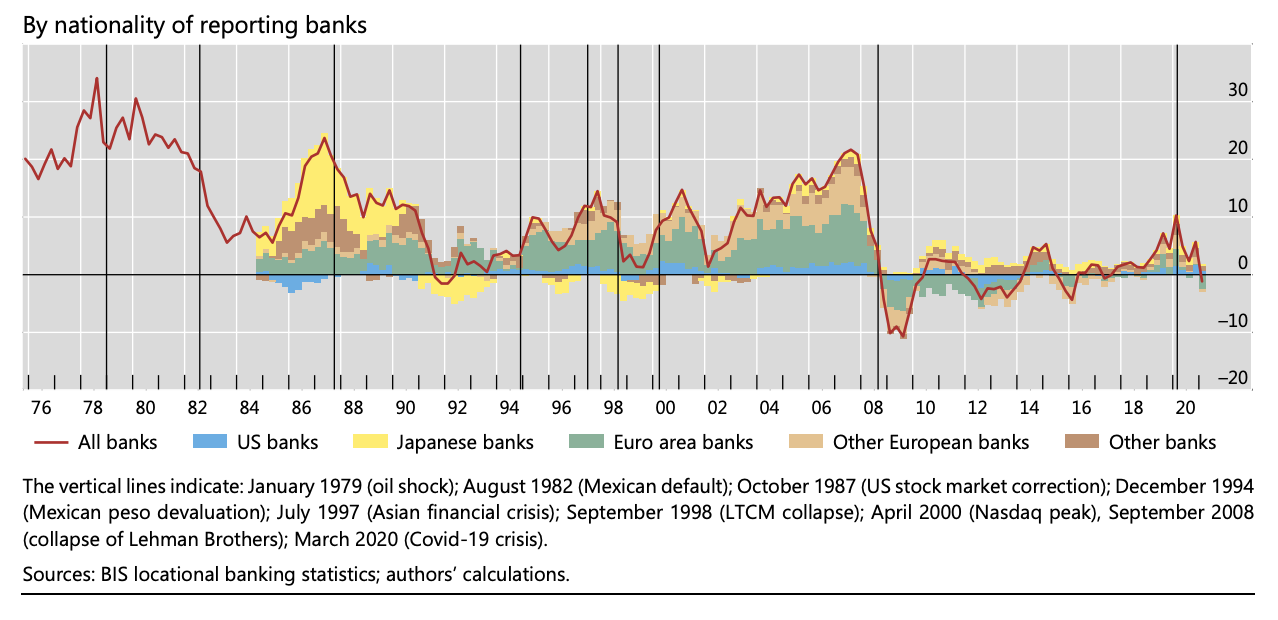

This makes a lot of sense. But it begs at least one important question. If global value chains are contracting how does this relate to the fact that the contraction in global finance since 2008 is confined to European banks, both Euro area, British and Swiss?

This is a truly dramatic reversal as shown by this remarkable chart from McCauley, McGuide and Wooldridge (2001).

Contributions to year-on-year changes in international claims, in per cent

From the 1990s onwards, European banks became THE main drivers of financial globalization. This went into reverse in 2008. By contrast, since the 1990s cross-border banking by Japanese and US banks shows no pronounced trend whilst cross-border banking by ROW banks (Chinese and other EM) has significantly expanded.

It would seem that there are three possible ways of interpreting this relationship between global value chain stagnation and European banking contraction: (1) European banks are particularly important in financing global value chains. (2) The value chains that contracted were those most tightly linked to Europe both in real and financial terms. (3) Finance is fungible, so a contraction in European lending shrinks funding across the entire system.

When I put the question to Shin, he said he preferred option 3: “European banks were at the center of dollar intermediation globally, and so their retrenchment reverberated globally.”

The key point is that it is not the national balance of payments or the national trade balance that counts here so much as the matrix of interlocking private balance sheets that mesh flows of raw materials, semi-finished goods, components and final products with their counterparts on the financial side across borders worldwide.

To further explore that network Shin uses a technique developed by Si Ying Zhang of the Hong Kong Monetary Authority in a recent paper in the Journal of Economics and Business, to track relationships between firms and their suppliers.

As Zhang describes it:

Data on inter-firm customer and supplier relationships and firm financial variables were taken from S&P’s Capital IQ (CIQ) database, which provides a snapshot of inter-firm linkages declared within the last two years. Our sample consists of all publicly traded and private firms in the “Manufacturing”, “Mining” and “Agriculture, Forestry and Fishing” SIC industry classifications that have declared a “supplier” and / or “customer” linkage with another firm in the last two years as of end-February 2020. This amounts to 35,940 companies covering eight of the eleven Global Industry Classification Standard (GICS) sectors in over 170 economies, and more than 120,000 bilateral customer-supplier relationships declared among them. Before going any further, it is important to point out some of the limitations of the CIQ data on business relationships. First, firm’s reported connections may represent only a portion of their total customers and suppliers, as companies are typically not obligated to disclose them all (the SEC mandates that issuers disclose all customers representing 10 % or more of their revenue, for example). To account for this, we follow Carvalho et al. (2016) by augmenting each firm’s list of suppliers (customers) with the reports of other companies that declare the firm as their customer (supplier), although this may not be able to capture all the unreported suppliers and customers. Second, the data is simply a binary variable representing the existence of a relationship, but does not provide the nominal value of each linkage nor the details of the transaction (such as what types of goods or services were exchanged). Such data, even if available from other sources, is notoriously sparse, especially on a global scale.

Though the CIQ data do not allow the construction of a corporate-level global input-output model, they do allow us form an impression of the extent of corporate interconnections by country and by sector.

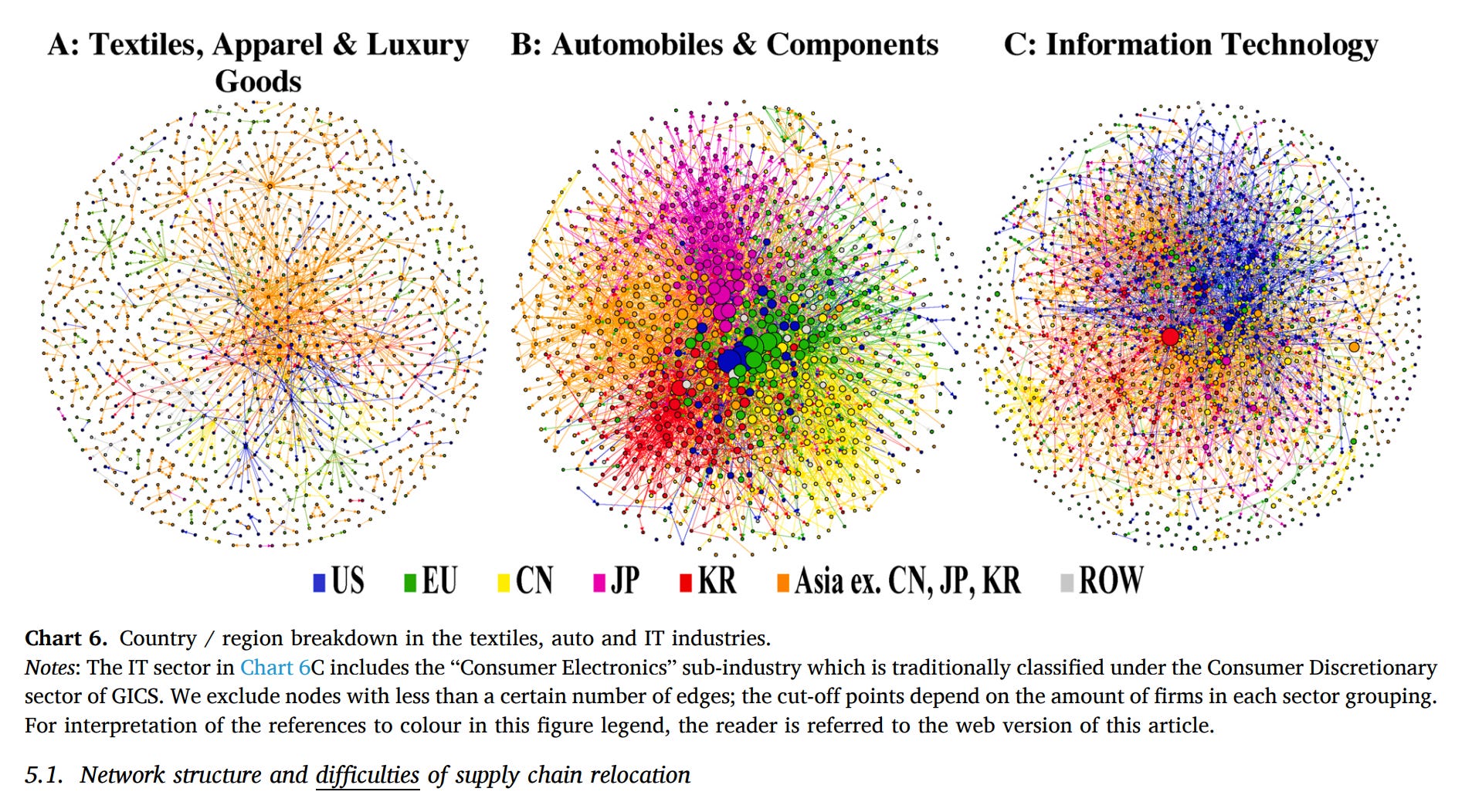

The diagrams are so complex that they are easier to read when broken down by sector.

We can clearly differentiate the different modes of globalization that prevail in the textiles, automotive and information technology sectors.

Textiles globalization takes the form of relatively simple China-Asia networks. The automobile industry is dramatically more complex and has a multi-polar structure with Japan, Europe and Korea operating complex regional and national networks (Japanese with Japanese) and the large American producers engaging in more cross national connections. Finally globalization of firm networks in IT involves a mesh of interconnections between Japanese, Chinese, Korean and US firms. The giant Korean node, presumably Samsung, stands out. Whereas the auto-motive industry is more regional in its patterns of integration, the electronics industry has developed a truly “global-scale” of integration.

Apart from their inherent fascinating, the significance of these diagrams for the discussion about globalization is that they demonstrate that the world economy has always consisted of a patchwork and likely always will. It has always been driven by networks that connect particular nodes in a way that is anything but uniform or comprehensive. Globalization has never consisted of all-with-all trade or financial flows. Sectors differ from each other in their logics. And large parts of the world, notably Africa, are simply not included in the maps.

From the point of view of legal structures, trade deals, WTO reform etc it may make sense to talk, as I did both on the panel and in my FT piece, about globalization being remade as a patchwork. But from the point of view of trade and financial flows, the real issue is how networks that are always and already uneven and heterogeneous shift over time. The relevant question is how the patchwork is being reproportioned and how the different logic of industrial sectors may shape those shifts.

As Zhang points out, there are crucial differences between key sectors in global value chains like automotive and IT:

Auto firms from the same country / region tend to gather in bunches, implying extensive intra-country and intraregional linkages, with significant overlap closer to the center of the network showing interlinkages between important (larger node) Asian, European, and US firms. … Even if major US and EU automakers (the large blue and green nodes in the centre of Chart 6B) were to reduce their supply chain exposure to China, or Asia more generally, Asian automakers may continue to capitalize upon the well-established regional supply chain clusters, which are likely to remain competitive due to their economies of scale.

In the IT industry, however, there is no such discernible pattern. Instead, the tech industry shows a highly decentralised network with a mix of intertwined Chinese, Korean, Japanese, “Asia ex. CN, KR, JP”, and US firms. … This suggests that cutting ties with Chinese firms in the tech industry could risk uprooting the regional IT supply chain due to deeply integrated US and Asian firms throughout the entire production network. A complete US-China decoupling would not only involve removing exposures to China and other central Asian players at the first layer (due to their interlinkages with Chinese firms), which in itself is damaging, but also the dependencies at all segments along the supply chain which could risk disintegrating the entire structure of the regional tech network. In other words, the highly decentralised nature of the tech industry suggests that, if the US is to reshore IT production, Asian economies may not have sufficient critical mass to allow their tech industries to develop self-sustainability.

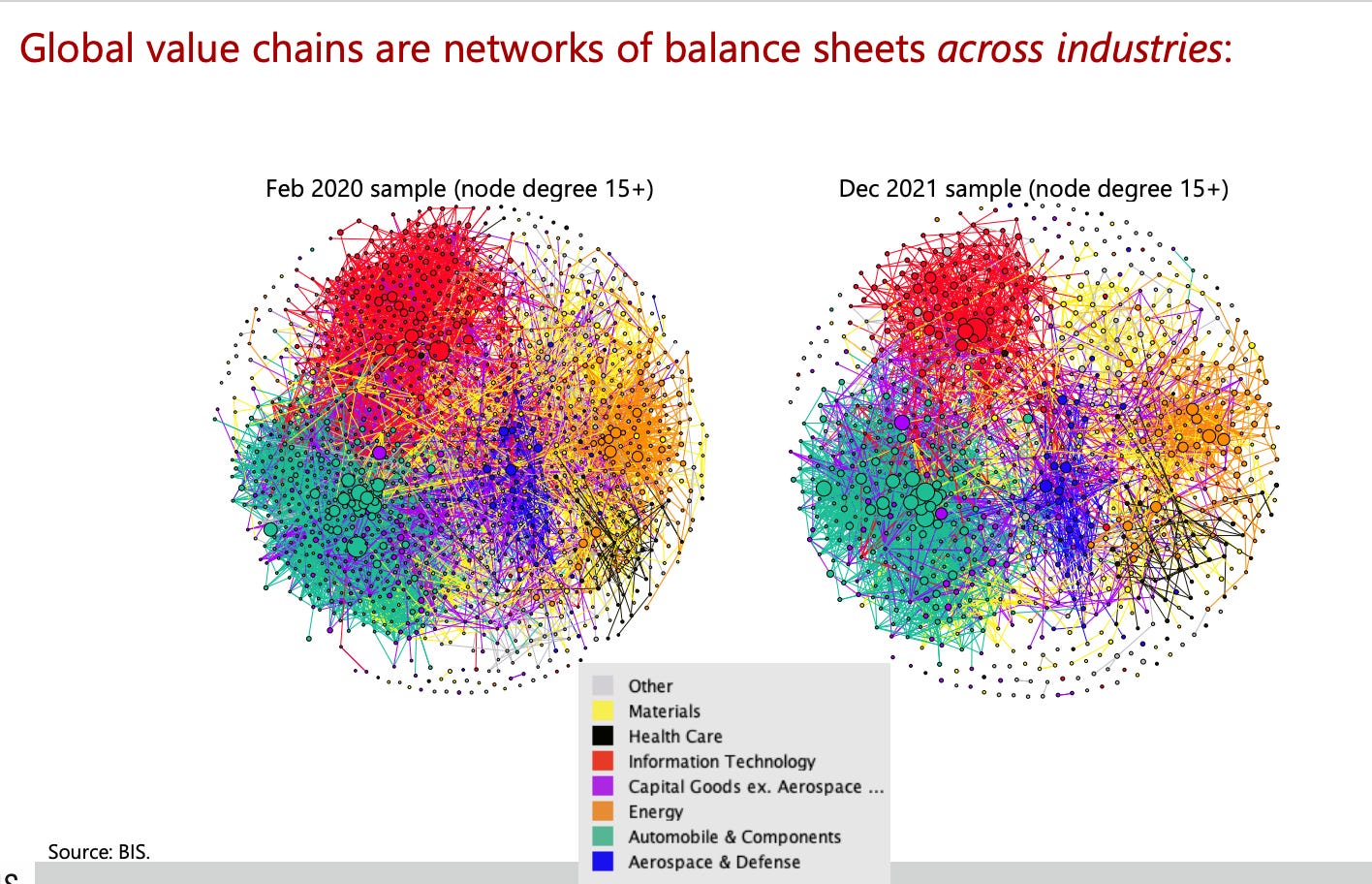

Zhang’s paper based on data for February 2020 thus suggests that the automotive model of globalization may be more resilient than that of IT. And that is what the more recent data presented by Shin in his recent paper seem to confirm.

Comparing the network of firms in February 2020 with that in December 2021 it would seem that the automotive industry network remained largely stable whereas that for Information Technology was subject to significant contraction.

Whether or not these trends continue, it is tools of this kind, covering both real and financial interconnections that will enable us to trace future trends in globalization.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, click here: