One week on from the shock announcement of the UK’s mini-budget, the pound sterling has recovered to the levels it was at before the panic. The UK, however, is far from out of the woods. Sterling may have rebounded, but the gilt market – the UK Treasury market – is on life support from the Bank of England. With interest rates surging, mortgage lending is drying up. The UK economy is heading towards a recession. And it is not just the UK that is under stress. On the other side of the Atlantic too, tremors are running through the US Treasury market, the foundation of the dollar system.

From a week of turmoil in the UK financial markets, we have learned four things.

(1) We are reaching the point in the monetary tightening cycle in which things begin to break. Truss and Kwarteng are clearly counting on the Bank of England to offset the shock to markets by raising rates. And yields have certainly surged as UK bonds have sold off.

But rather than restoring equilibrium, the spectacular collapse in the price of long-dated UK bonds (and the associated rise in yields) exposed a dangerous trigger mechanism in the UK financial system. The problem was the stress unleashed in the pension sector by rapidly rising rates. As interest rates surged, pension funds that hold hedging bets against the possibility that interest rates will fall – so-called liability-driven investment strategies – faced calls to post more capital. As Toby Nangle, formerly a multi-asset fund manager, identified in an excellent Financial Times article in July this year.

… £1.5 trillion of assets held by UK pensions … have been hedged in so-called LDI trades. LDI (Liability Driven Investment) helps to match pension funds’ liabilities (future payments to pensioners) with the schemes’ assets.

As Nangle explains in exemplary style:

The Pensions Regulator estimates that every 0.1 percentage point fall in UK gilt yields increases a conservative measure of UK scheme liabilities by £23.7bn. In the decade to December 2020, long-dated, 25-year gilt yields fell by more than 3.5 percentage points and scheme liabilities increased by £960bn (about 40 per cent of GDP). Pension schemes can’t control wild swings in their liabilities’ value. But they are not completely helpless. They can invest their assets so that they become relatively indifferent to bond market gyrations, and this is where LDI comes in. As bond prices determine the valuation of pension liabilities, moving pension assets into bonds will effectively hedge the volatility of liabilities. The problem is that few pension schemes are well-funded enough to make this trade. Instead, schemes invest a portion of their assets in liability-matching bonds and a portion in growth assets — corporate credit, equities, property. They then hedge the risks of that strategy with derivatives, using bond assets as collateral. The hope is that growth assets will deliver decent returns and make them fully funded while the derivatives will desensitise them to future interest rate swings. The results have been good, but have also left pension funds as counterparties to enormous quantities of leverage in the financial system

That risk was starkly exposed when rates shot up. Added to which, since UK pension funds invest not only in UK gilts but also in foreign bonds, as the pound sterling plunged they faced margin calls on foreign exchange derivatives. When funds try to meet those margin calls they need to raise cash fast. Under normal circumstances UK gilts, like US Treasuries are a safe piggybank of liquidity. But in a fire sale they lose value too. As one market participant observed:

“Gilts are a source of liquidity. Now, the thing is that your gilts are also losing money. So basically, your derivatives are getting worse and worse and worse, and your gilts are getting worse. So, the whole thing is getting really bad. Whatever you want to post for collateral is getting worth less,

These trigger mechanism do not appear to have been on the Bank of England’s radar. This raises once again the nagging question of what the key people in central banks and financial regulators – not just in the UK but around the world – choose not to know about the inner-workings of vital financial markets.

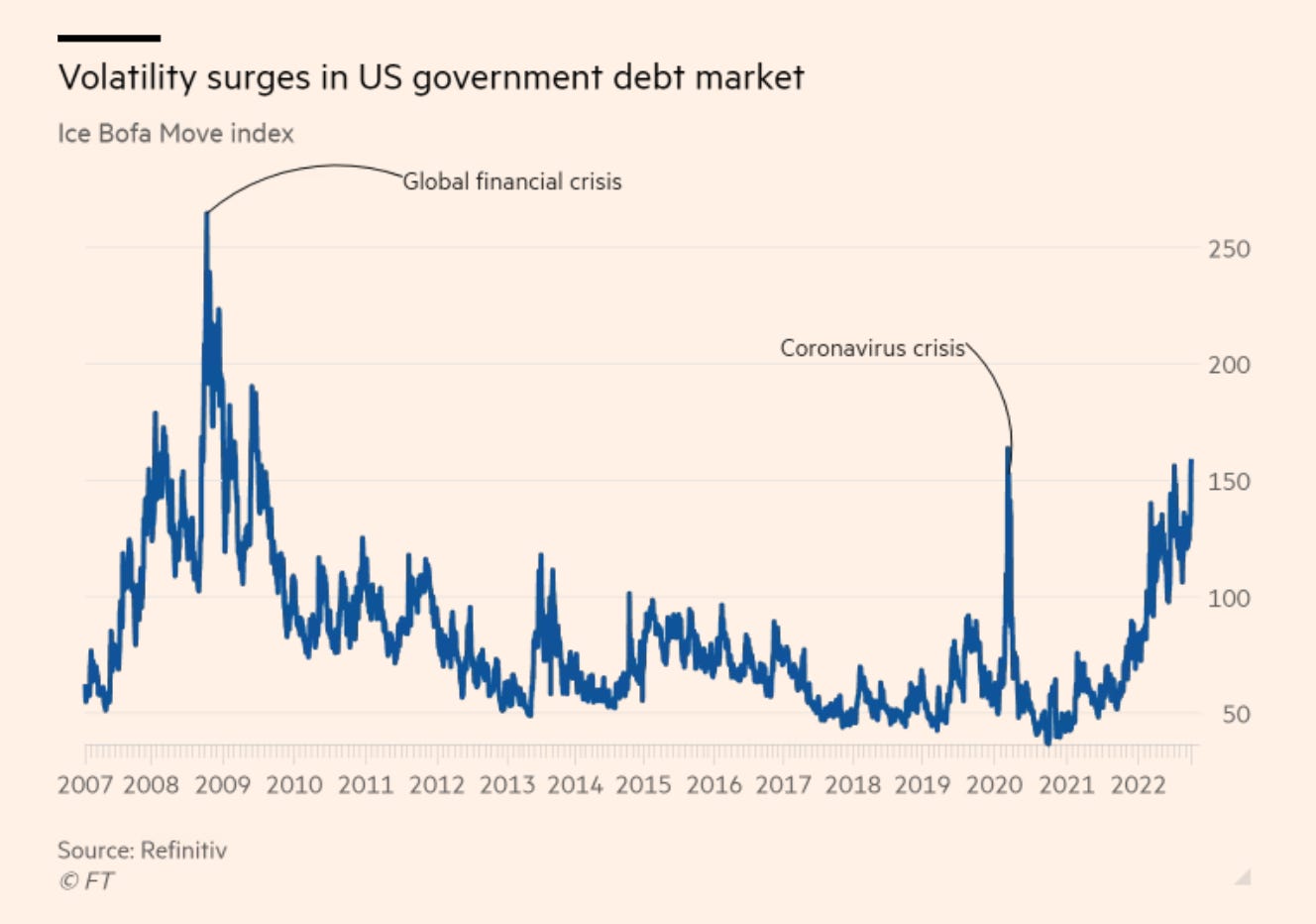

(2) Global bond markets interact in subtle, non-mechanical ways. I underestimated this effect in a newsletter last week where I flippantly declared the UK gilt market too small to matter. In fact, at a time of general nervousness, the spasm in the UK market rippled around the world. The EU felt the impact.

And so too did the US. As one market participant observed: “At the start of the week we were seeing moves in US Treasuries that could only be explained by what was happening in the UK.” In part this sensitivity of US markets is explained by deteriorating liquidity. As Bloomberg reports:

Liquidity in the Treasury market is extremely low at the moment. Liquidity conditions for rates markets this year resemble the conditions seen in the pandemic and the period after the Lehman crisis, JPMorgan data show.

In what the FT dubbed a “volatility vortex”, falling liquidity – fewer participants in the market – leads to higher volatility, which leads to a further withdrawal from the market by major players, which further reduces liquidity, and so on.

In this precarious situation, the news from London had an outsized impact.

As Bloomberg reported Bob Miller, head of Americas fundamental fixed income at BlackRock Inc., the world’s biggest asset manager:

“You can see the footprints of the Gilt market all over the US Treasury market in the past week … The signal value from the price action in the US bond market is being significantly degraded by non-domestic factors.”

Analysts at JPMorgan highlight the fact that US investors have been intently focused on the state of the global market. As Tracy Alloway writes on Bloomberg

average volatility of US rates during Asian and European trading hours has also increased this year.

As one market particpant remarked to Alloway:

“The global nature of the current inflation backdrop, coupled with the emerging globally synchronized policy tightening that is underway, has resulted in much more frequent instances of US rates responding to new information from policy developments abroad … This has led to increased volatility of US rates in non-US trading hours.”

This raises the question of whether there are vulnerabilities in the US market akin to those exposed in the UK. It is hardly reassuring that sales of new Treasury bonds have drawn lack lustre demand and that some market participants were even talking of a ‘buyers’ strike’. And one might ask whether it is truly reassuring when Janet Yellen as Treasury Secretary is forced to affirm that:

“We haven’t seen liquidity problems develop in markets — we’re not seeing, to the best of my knowledge, the kind of deleveraging that could signify some financial stability risks … With the United States moving faster than many other countries, we’re seeing upward pressure on the dollar and downward pressure on many other foreign currencies … To me, these kinds of developments — which represent a tightening of financial conditions — are part of what’s involved in addressing inflation. … I think markets are functioning well.” She added, “The overall environment is one of high inflation in many advanced economies. Central banks are addressing it in almost all countries — other than China — but operating at different speeds and different paces.”

The sensitivity of the US market to the UK, raises the question of the overall fragility of global debt markets. Last week tremors were running through euro government bond markets including the German Bund market. The fear is that as central banks end the long period in which they systematically supported bond markets, deep cracks will be exposed. And that was rather confirmed by events in the course of the week.

(3) If it was as shock in the UK that echoed around the world, it is also true that the Bank of England’s intervention on Wednesday helped to calm the situation. Early on Wednesday the yield on the US 10-year Treasury rose above 4% for the first time since 2010. Then when the Bank of England moved in, the market abruptly changed direction.

Far more nakedly than in 2020, the Bank of England’s hurried interventions in September 2022 have exposed the forces that truly propel central bank intervention in the current dispensation. The policy of asset purchases may look like expansionary macroeconomic policy – a resumption of QE or a coordination of monetary with fiscal policy. They may look like impressive demonstrations of the power of central banks. But they are, in fact, crisis-driven defensive reactions to the spasms of leveraged, market-based finance. What is at stake is not fiscal dominance – the central bank following the lead of the elected government – but financial dominance. The central bank is being forced to act by financial market stress.

By Tuesday 27 September, major players in London were screaming for the Bank of England to act:

A senior executive at a large asset manager said they had contacted the BoE on Tuesday warning that it needed “to intervene in the market otherwise it will seize up”

But the Bank was not yet ready to act. That changed on Wednesday 28th.

“If there was no intervention today, gilt yields could have gone up to 7-8 per cent from 4.5 per cent this morning and in that situation around 90 per cent of UK pension funds would have run out of collateral,” said Kerrin Rosenberg, Cardano Investment chief executive. “They would have been wiped out.”

For the Bank of England it was a shocking pivot. Rather than selling gilts from the portfolio accumulated during the response to the 2020 crisis – Quantitative Tightening – the BoE reversed itself. It began buying long-dated bonds at a rate of up to £5bn a day for 13 working days. As the FT reported:

The bank stressed that it was not seeking to lower long-term government borrowing costs. Instead it wanted to buy time to prevent a vicious circle in which pension funds have to sell gilts immediately to meet demands for cash from their creditors. That process had put pension funds at risk of insolvency, because the mass sell-offs pushed down further the price of gilts held by funds as assets, requiring them to stump up even more cash. “At some point this morning I was worried this was the beginning of the end,” said a senior London-based banker, adding that at one point on Wednesday morning there were no buyers of long-dated UK gilts. “It was not quite a Lehman moment. But it got close.”

(4) Talk of markets at that point become euphemistic and we must ask, beyond the need for “systemic stability”, who are the principal and immediate beneficiaries of these interventions? Who exactly is being bailed out when the Bank of England steps in? The answer is not clear cut. Is it pension policy holders? The economy at large that is spared a catastrophic financial crisis? Or is it BlackRock Inc., Legal & General Group Plc and Schroders Plc who manage LDI funds on behalf of pension clients? The very fact that we cannot give a confident answer to these questions, suggests that we are dealing with a system riven with conflicts of interest. And this poses the question of reform. Does it really make sense to perpetuate a system in which disastrous financial risks are built into the profit-driven provision of basic financial products like pensions and mortgages? Yes the central bank can act as the fire brigade, but why do we such a dangerous situation as normality. Why do the smoke detectors fail again and again? And why is the house not more fire proof? It is time to ask who benefits and who pays the cost for continuing with this dangerously inflammable system.

Amongst the costs this system imposes should be counted the sheer uncertainty it generates. As I hit send on this newsletter – the flight map tells me we are 35,000 feet up, somewhere over Azerbaijan – the CDS on Credit Suisse debt have surged to 2009 levels and the chief economist of the IIF is warning of dollar funding stress. None of us can know what the coming week has in store for us.

But before anyone starts wittering on about irreducible, metaphysical uncertainty, let us be clear. This is nothing of the sort. The hazards that we face in the global financial markets are entirely human-induced, macro-risks. They are the results of a contradictory, incoherent and hazardous profit-driven system, which the status quo underwrites.

****

I love writing this newsletter. It goes out for free to tens of thousands of readers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, there are three subscription models:

- The annual subscription: $50 annually

- The standard monthly subscription: $5 monthly – which gives you a bit more flexibility.

- Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.

Several times per week, as a thank you, all paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images.

To join the supporters club, click here: