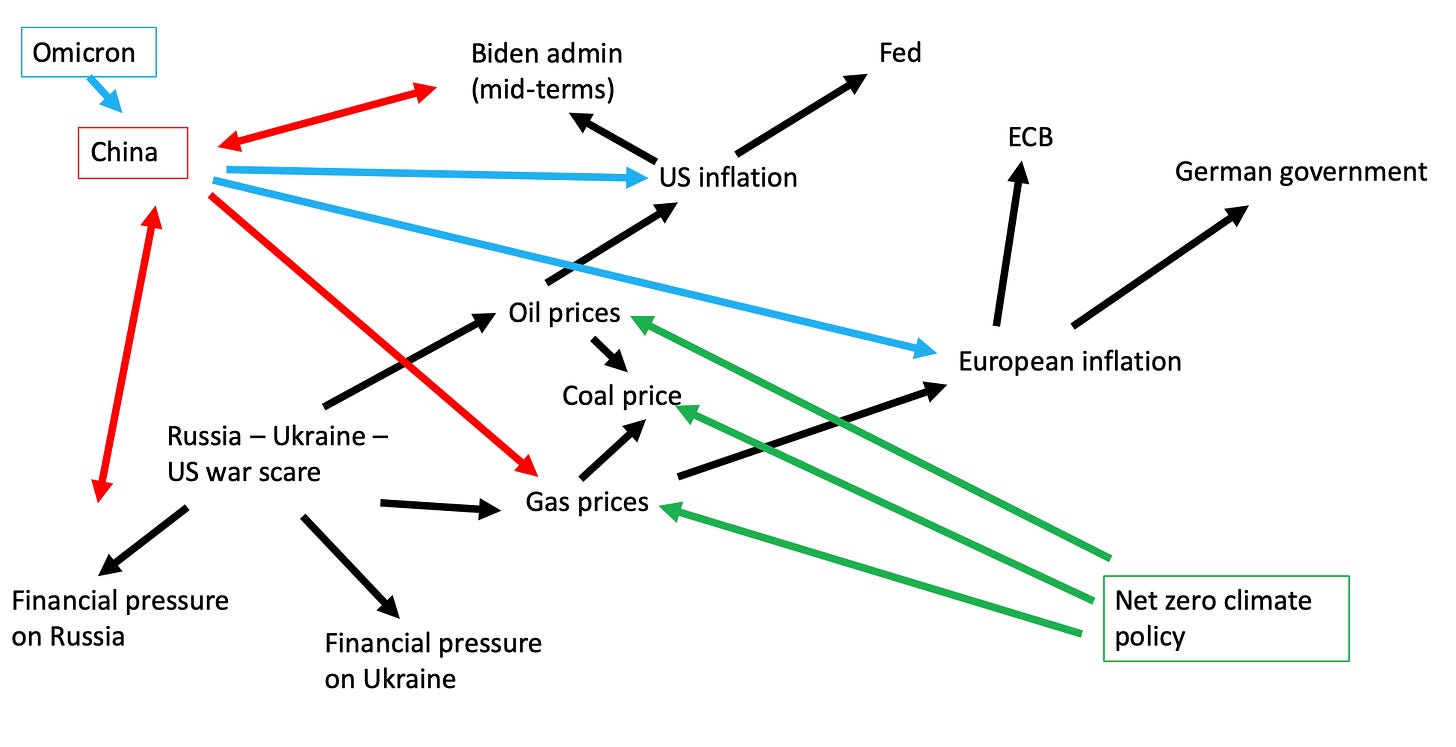

In Chartbook #73, back on January 21st this year, I proposed Krisenbilder – crisis pictures – as a way of making sense of what then looked like a complicated pattern of stresses around the world scene.

I proposed the schematic because it seemed a useful way of mapping interconnected forces in a heuristic way. As it turned out, it succeeding in capturing quite a lot of the dynamics that have subsequently convulsed the world.

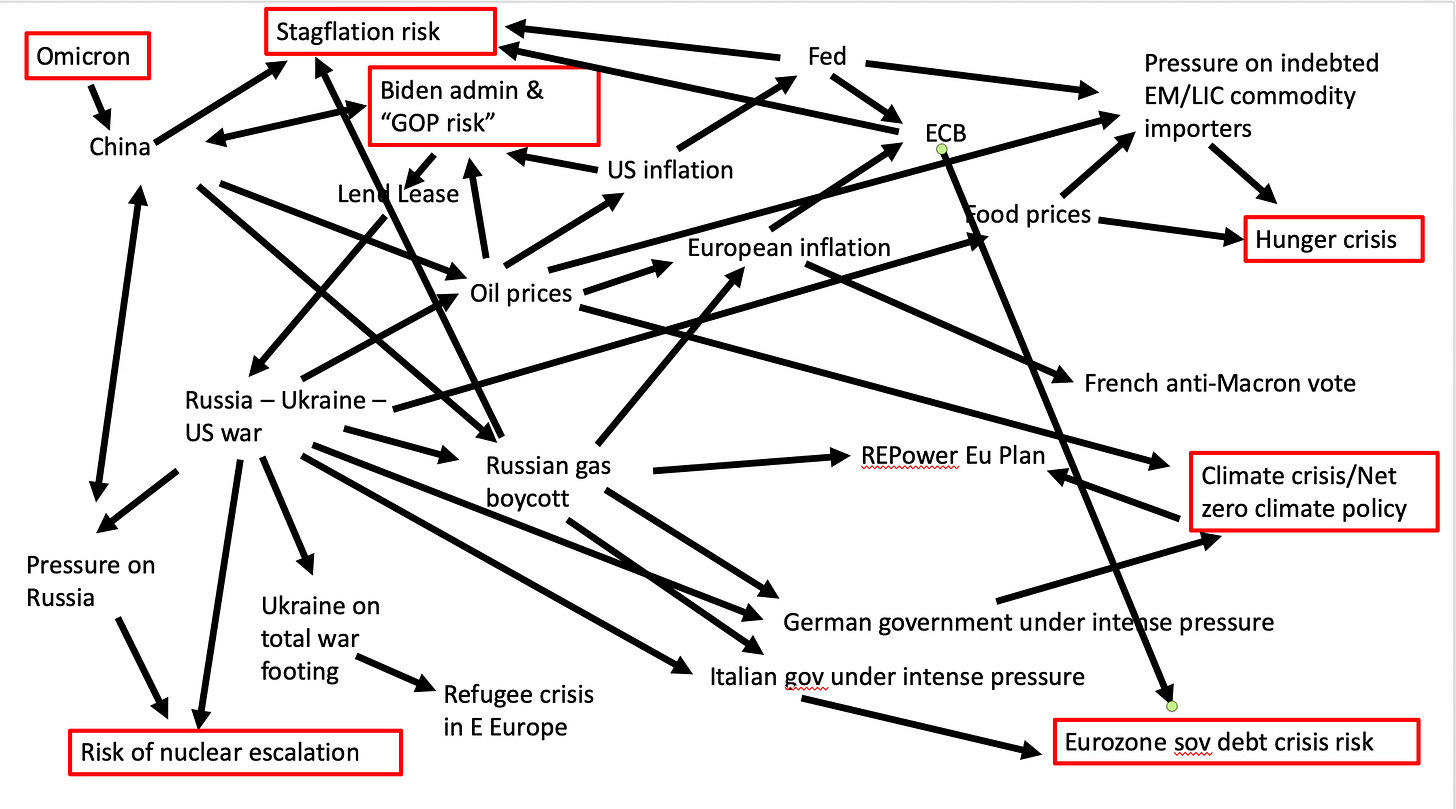

That was January 21st. The war unleashed by Russia on February 24th has added spectacularly to the scale of tension and the complexity of the interconnections.

What was once a relatively legible map has become a tangled mess.

I don’t claim any originality for the exercise. All of these connections are routinely discussed in intelligent analysis. But pulling all these well-known influences together in a single chart does convey a sense of what a complex situation we are dealing with.

To make matters even more complicated, this synchronic presentation obscures the historical genesis of these forces. Stresses in energy and food markets were already very evident in 2021. The war has had the impact it has because it has exacerbated existing tensions. Food prices were already rising in 2021 and provoking warnings of a crisis to come. Energy markets were stressed well before the war broke out. Now both stressors are knotted together with the war.

I have highlighted in red what emerge as a series of macroscopic risks, all of which may come to a head in the next 6-18 months.

All of them, from the risk of nuclear escalation to global stagflation, are familiar from public commentary on the crisis. The selection is debatable. Should the EM/LIC debt crisis be classified as a macroscopic risk? Perhaps.

What seems worthy of note is, first of all, how many radical challenges there are on our radar. I count seven, without even including a debt crisis in several EM/LIC.

Second, what is striking is the deep uncertainty that surrounds several of them (e.g. new COVID variants, or nuclear escalation). These are tail risks which can no longer be ignored but to which it is hard to attach a real probability.

Thirdly, they are all happening at once and several of them reinforce each other. By early 2023 it is entirely possible that we will see a dangerous new COVID variant that defeats even the best vaccines, a shift to active use of nuclear weapons in the war in Ukraine, a rampant Republican party under the banner of MAGA, global stagflation and a fossil fuel ramp up to meet escalating energy shortages, furthermore in Europe the breakup of Mario Draghi’s coalition in Italy, helping to trigger surging spreads in the Eurozone met by an inadequate response from the ECB.

We would be unlucky if all of those things did happen. But it is well nigh inconceivable that at least one of them will not. The defeat of the Democrats in the US, is surely the most likely outcome in the upcoming midterm elections.

Some of these crises are what you might call overarching. A lethal new COVID variant would be a game-changer in ever respect. The same could be said for a move by Russia to the use of nuclear weapons.

Other forces of crisis tend of offset each other. A new wave of COVID-lockdowns in China would likely help to break momentum in commodity markets and tend to push prices for things such as oil and iron down downwards, easing inflationary pressure.

Other effects are more ambiguous. If a Trumpite GOP storms back to power in Washington that will likely reduce the pressure in Congress to up the ante in the struggle with Russia. On the other hand it may make the Biden administration more aggressive, since foreign policy will be one of its only trump cards (no pun intended), and one around which it might find majorities in the Senate.

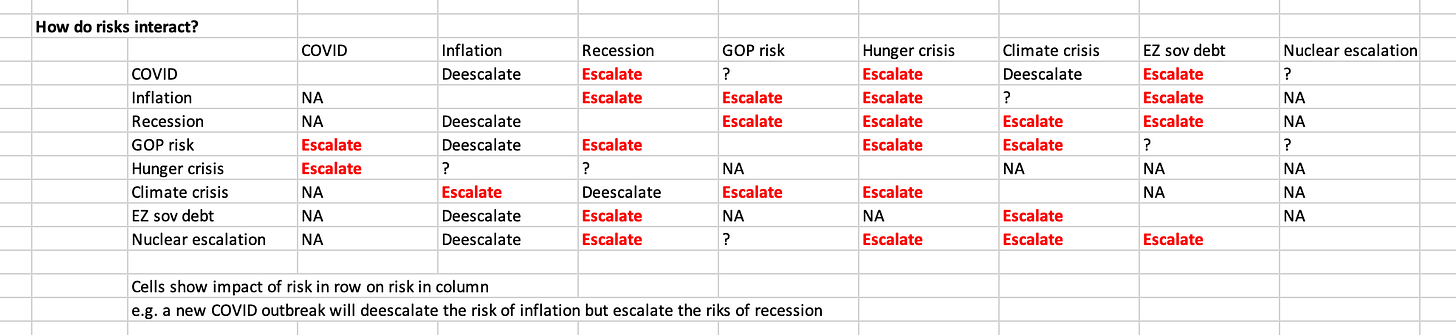

To try and summarize these effects I compiled the following, entirely provisional and highly debatable matrix of interactions between the different macroscopic risks facing us over the next 6-18 months. The question that the table asks is how do the risks listed in each row of column 1, affect the risks laid out from left to right across the table.

For sake of clarity I have divided the stagflation risk into a risk of recession and a risk of accelerating inflation.

What this matrix helps us to do is to distinguish types of risk by the degree and type of their interconnectedness.

The risk of nuclear escalation stands out for the fact that it is not significantly affected by any of the other risks. It will be decided by the logic of the war and decision-making in Moscow and Washington. A food crisis does not make a nuclear escalation any more, or less likely. On the other hand, a nuclear escalation would, to say the least, dramatically escalate several of the other risks.

Continuing inflation will likely function as a driver of several other risks, but those risks in turn (COVID, recession, EZ sov debt crisis) will likely deescalate the risk of inflation. I would not say that this is a forecast, but it does bias me towards thinking that inflation will be transitory. Most of the big shocks that we may expect, tend to be deflationary in their impact.

Conversely, a recession seems ever more likely in part because the effect of most of the bad shocks we may expect – from COVID, mounting inflation, or a fiscal deadlock in Congress – point in that direction.

The obvious next step is to ask whether the feedback loops in the matrix are positive or negative. So, for instance, a recession makes a Eurozone sovereign debt crisis more likely, which in turns would unleash serious deflationary pressures across Europe. Conversely, inflation in fact seems self-calming. The effects it produces tend rather the dampen inflation than to feed an acceleration. At least as I have specified the matrix here.

A global hunger crisis seems alarmingly likely in part because all the other major risks will exacerbate that problem. A hunger crisis, however, will largely affect poor and powerless people in low-income countries, so it is unlikely to feedback in exacerbating any of the other major crises. It is an effect of forces operating elsewhere, rather than itself a driver of escalation.

To this extent the matrix becomes a way of charting the power hierarchy of uneven and combined development. Some people receive shocks. Others dish them out.

I am not committed to this sketch, or this matrix in anything other than a heuristic way. The analysis could be multiplied and expanded in many directions. With regard to the hunger crisis, for instance, our conclusions of its likely impact would be different if we add in the question of migration.

Several of the interactions I have labeled are highly debatable. Some I have simply left blank, NA or marked with a question mark. Is it right, for instance, to assign an escalatory effect to the climate crisis on inflation? In this case I am invoking the greenflation concept of which I am somewhat skeptical. Likewise I say that a recession would exacerbate the climate crisis because I expect it to lead to a recession in green investment. But these effects, their scale and sign are up for debate.

Overall, what the combination of the crisis picture and the matrix help us to see is that not only do we face multiple macroscopic risks hedged with great uncertainty, but their interactions tend to be escalatory.

This is not inevitable, this is not a prophecy of doom. But it is an assessment of multiple and compounding risks.

It may perhaps be taken as the definition of the polycrisis, the concept borrowed by way of Jean-Claude Juncker, that I invoked in my book Shutdown.

A polycrisis is not just a situation where you face multiple crises. It is a situation like that mapped in the risk matrix, where the whole is even more dangerous than the sum of the parts.

****

I love putting out Chartbook. I am particularly pleased that it goes out for free to thousands of subscribers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, press this button and pick one of the three options: