Over Christmas, I was lucky to have chance to review Brett Christophers essential new book on land privatization in Britain –The New Enclosure. The Appropriation of Public Land in Neoliberal Britain (Verso) – for the FT.

It was an unlikely gig, you might think – discussing a hard-hitting piece of radical geography in the spirit of Doreen Massey published by Verso in the pages of the premier newspaper of global capitalism. But to their great credit FT’s excellent finance blog Alphaville had already run a guest column by Brett and the FT’s broad-minded literary editor Frederick Studemann was easily persuaded. And with good reason.

The New Enclosure is an essential contribution to the political economy of the UK and to our understanding of neoliberalism more generally.

Credit to the FT for giving it the space it deserves. As a reviewer it is gratifying to continue the boundary-crossing conversation about contemporary capitalism in the pages of the FT that for readers of my generation goes back to the 1980s dialogue between Marxism Today and the FT when folks like Martin Jacques and Charles Leadbeater formed the link.

In a recent review of Quinn Slobodian’s outstanding book about the post-Habsburg roots of neoliberalism, Globalists, I came to the conclusion that we needed to go beyond the history of generalized ideas about economic order, the kind of thinking to which Hayek wanted to limit economics, to investigate:

“the engines both large and small through which social and economic reality are constantly made and remade, tools of power and knowledge ranging from cost of living indicators to carbon budgets, diesel emission tests and school evaluations.”

This is precisely what Brett Christophers delivers. If you had not previously thought of public land management as a strategic site of power, the New Enclosure will blow your mind. In unforgettable passages Brett documents the squeezing of Britain’s civil servants into more and more claustrophobic cubicles.

Source (I kid you not): HMRC

If there is a sweet spot between Das Kapital and The Office that’s where you will find Brett’s book. My new fantasy would be for Armando Iannucci to do a film version.

But day-dreaming about the satirical genius of In the Loop was productive also in another sense. I loved the New Enclosure as an account of the operation of government under the imperative of neoliberalism. But what I craved was a deeper integration with economic history.

One angle that Brett clearly recognizes is the possibility of reading the entire process of privatization since the 1970s in terms of a logic of class enrichment. He notes this possibility but then does not explore it. As I remark in the review:

“As a historical analyst, Christophers is remarkably restrained. There is no doubt that property developers benefited enormously from privatisation. Those developers are big donors to the UK’s Conservative party, the major advocate of privatisation. Parliament is full of landowners, great and small. Christophers does not deny that profiteering by a new class of private and corporate landowners is one likely explanation for the privatisation drive. But he does not go down that muckraking path. One can only hope that others, building on Christophers work, will do so.”

In the last couple of days Brett has posted a piece – How Developers Bought the Tory Party – which fills the gap. It is great reading.

But I find it striking that in his book Brett adopts the restrained approach that he does.

As he says, one main obstacle to exploring the class enrichment angle is the lack of evidence. Dirty deals are done in the dark. And that is where they want to stay. You have to have the skills, connections, impulses and professional mission of an investigative reporter to go after them. It involves a certain amount of intellectual, personal and professional risk. If you get the wrong end of the stick you end up drifting off into the territory of crude “conspiracy theory” and, in the UK, quite possibly in court.

As I read Brett he prefers to offer his readers what he feels he can document for certain. He assembles his argument from material that is out in the open. Doing that is, in a sense, a higher intellectual game – we are all playing with the same pieces. And what Brett is able to show us is, after all, damning enough.

But does this kind of reconstruction go far enough? Don’t we need muckraking? Do we end up with a narrative that is overly clean?

I think Brett does a great job of making clear that his entire argument is operating within self-imposed limits. It is an analysis of the realm of government and governmental discourse. As such it makes a huge contribution. It provides a frame within which many other histories can be written. But reading Brett has left me worrying about the sanitizing effect of this kind of methodological choice. It has left me worrying because, as I am all too aware, the same criticism can be made of my book Crashed.

Is it too clean? Too respectable? Too locked within the discourse produced by the machinery that it seeks to anatomize? Not distanced enough? Too top down? Not angry enough? All these questions have been asked. And my answers would be even more inadequate if it were not for the interventions of close friends and brilliant readers of the manuscript who insisted that my version of the financial crisis and its aftermath should be dirtier. You know who you are!

One could, of course, defend oneself by arguing for a division of labour: “I’ll lay out the macrofinancial processes. Somebody else, who is good at it, can do the muckraking.” And I find this reasonable as a first line of defense.

As a stronger defense I would argue that explaining the financial crisis in terms of criminality, deceit and fraud actually has an ambiguous political effect. On the one hand it arouses indignation – “how did the bastards get away with that!”.

But by the same token the search for the evil doers can easily shade into a rotten apple theory when what we should be talking about is the barrel itself and the orchard the apples are harvested from (As the Marx of the “Paris manuscripts” might have said: rotten apples aren’t simply products of “nature”).

Seen in this way an explanation of the crisis that is as sanitized as possible serves a critical purpose. It focuses attention on the mechanisms that were perfectly legal and normal, but nevertheless produced disaster. The crisis was a feature not a bug.

But I cannot say that these defenses entirely satisfy me. At a personal level, I wonder about my tendency to flinch away from the dirtier and messier side of the historical drama. Is it significant that I prefer spy dramas to murder mysteries? Why did I write my first book about statistics in the Third Reich in part as a critique of Götz Aly’s much grubbier account of similar processes, consciously holding the Holocaust at bay? I exorcised some of those demons with Wages of Destruction, which is plenty grubby. But even there the pivotal figure is Albert Speer the ultimate Teflon-man.

Obviously, this isn’t just my personal problem. But I cannot deny that I feel it involves me personally, it touches something about my identity. And it is hardly surprising, given my personal trajectory in institutional and social terms, my class position and the folks I’m in conversation with.

Could one resolve this dilemma with a two-pronged approach – muckraking working side by side with macrofinance? Read one, then the other. Get the big picture and then delve into the dirty details. That delivers a one-two punch, which can, no doubt, be effective. But it begs the question of synthesis and comes with its own ideological risks.

Separating the two approaches, the clean and the dirty, reifies as a methodological alternative a social distinction that is an artefact of our legal system. This is why the critical investigation of “game playing” around banking regulation and tax evasion (both areas which Crashed slighted) is so important. Exploring how the boundary is crossed again and again reveals rather than reifying the constructedness of the distinction between legitimate and illegitimate, legal and illegal, normal and abnormal.

If one were to extend the argument of New Enclosure in this direction one might imagine a development that explores the blurred line between the offering of general reasons for land privatization, which Brett explores so brilliantly, and the pursuit of profit by developers. How were think tanks funded? Which MPs and ministers spoke when on which issues and who stood immediately to gain. It is the stuff of the good, old-fashioned critique of ideology. In our current world, we cannot do without it.

But I also wonder whether there is not another means of bringing the two sides together.

On the one hand you have the juxtaposition between the investigation of generalized governmental discourse and procedures, which is what Brett does so brilliantly, and the particularized, individualized business of deal-making and the extraction of profit by a variety of interests. But reading the New Enclosure what I really craved was not so much the investigation of individual shady privatization deals, but the broader macroeconomic context.

At this point I want to insert a typically apposite suggestion from Anusar Farooqui aka Policytensor. In response to the post on facebook he suggested:

“Doesn’t Minsky offer the connection you seek between the financial cycle and muck? The corruption and swindling is not random but a systematic feature of every mature cycle. One is almost tempted to say it is diagnostic. Like the construction of the tallest building, it makes for an excellent systematic short signal.”

I think this seems spot on. I dont use Minsky enough!

In any case, the shift to the macroeconomic level speaks to my usual preference for the macroscopic big picture. It has been said that “Tooze likes a good graph”.

The formal order that statistics impose on reality exercises a magnetic attraction, at least it does on me. And I would also defend the statistical approach as a way of capturing, at a high level of aggregation, the urges to profit and accumulation that muckraking investigations reveals on an individualized case-by-case basis.

A surging upward graph of profits and prices conjures the boisterous turmoil of animal spirits, in the same way that the brushstrokes of a painter evoke a raging sea. And we know that “behind” the graphs, and impelled by the movements they describe is the activity of the economy, where macro and micro merge. Price movements drive the restless activity of the land speculators and developers, which impel price movements.

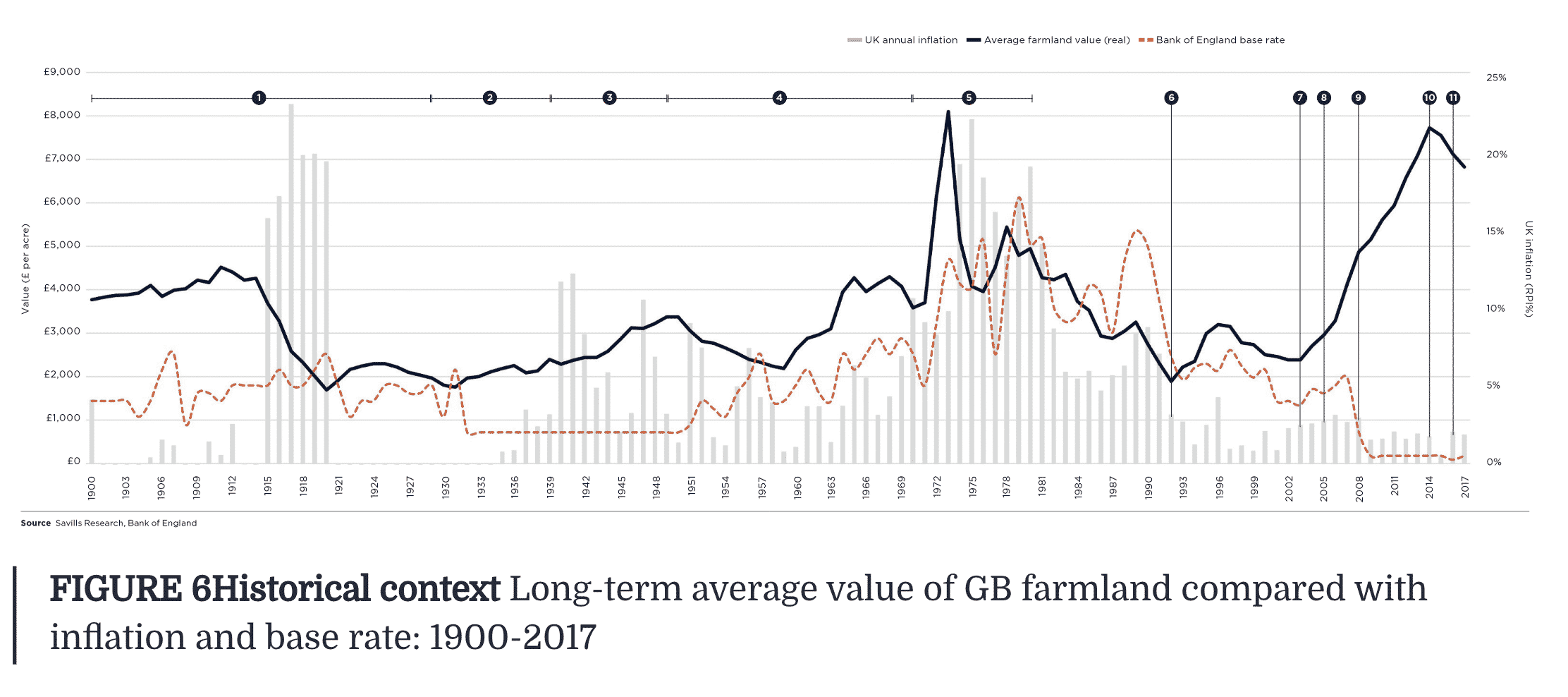

The huge expansion of public land ownership that Brett so dramatically highlights took place broadly between WWI and the 1970s. That is also a period in which farmland and house prices were historically depressed.

Source: Savills

The most widely accessible UK house price index is deeply misleading because it starts in 1952 at the trough of a cycle and show only an upward trend. But this followed after decades of decline that began around World War I. As one Barclays investment report comments, citing data from Neil Monnery and his book Safe as Houses: “the average house price in 1900 was just under £49,000, in 2017 terms. It took about 60 years for prices to rise consistently above that level, adjusted for inflation.”

The question that I would love to see explored, is the question of the relationship between the nationalization of land between 1900 and the 1970s and its shifting valuation. Was the repurposing and revaluing of land, which expressed itself in its price, a precondition for the huge increase in state ownership? Did the state act as a buyer of last resort? How did regulation and market forces interact?

Seen in these terms Brett’s narrative is framed by two great price movements. In the late 19th century it was the globalization of agriculture that sent farmland prices tumbling in Europe and broke the grip of the landed aristocracy. After World War I, the huge surge in agricultural production outside Europe and subsequent dislocation of markets dealt a further blow to commodity prices, from which they took half a century to recover.

From the late 1960s the unfettering of the monetary system and the expansion of credit made land and housing into an inflation hedge and an object of speculation both large and small. This was the backdrop to the massive privatization that began in the 1980s but also, of course, to the housing bubble that fuelled the crisis of 2008 and the narrative of Crashed.

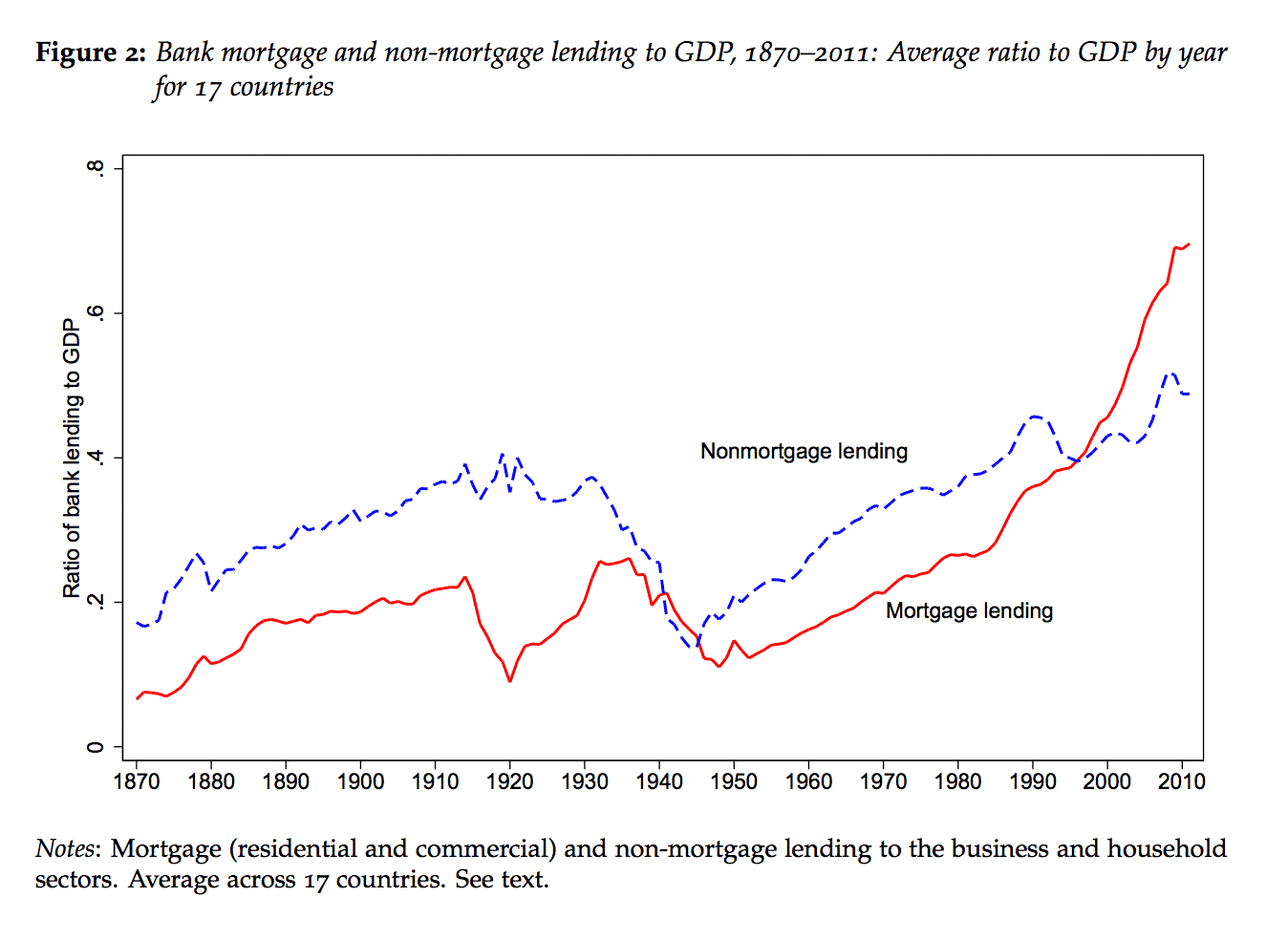

Source: Jordà, Schularick and Taylor NBER

Source: Jordà, Schularick and Taylor NBER

As Jordà, Schularick and Taylor have documented, over the long run, real estate and mortgage credit are key drivers of cycles of leverage in global capitalism. As Brett Christophers shows us, in our “financialized” and “post-industrial” world, land and property remain the most import class of assets and the most important form, therefore, of collateral.

To sum up:

If we want to break out of the constraints imposed on us by neoliberalism’s cognitive strictures, thinking about Quinn Slobodian and Brett Christopher’s books in relation to Crashed suggests three routes: One can flout Hayek by delving into the depths of governmental machinery as Brett does so brilliantly. One can strip the magic from capitalism (entzaubern) by exposing its seamier side and the sheer grubbiness of deal-making. But we also need to defy Hayek’s insistence that the economy cannot be represented or made calculable, his Bilderverbot (the Mosaic ban on graven images). For all their many inadequacies, we must cling to the macro- in macroeconomics and macrofinance. If what we are after is an understanding of the complex forces driving the uneven and combined development of the global economy, there is no alternative.