The Turkish financial crisis has shot into the headlines in recent weeks. It has been a long-time coming.

The entire time I was writing Crashed, the “Middle East” was threatening to bleed into a crisis narrative that I was trying to centered on the US-EU-Russia-China axis. I started working seriously on the Crashed project in the fall of 2013 in the wake of the taper tantrum, the Gezi riots, and Erdogan’s early outbursts about the interest lobby. That fall we were also digesting the implications of the military coup that crushed the Arab spring in Egypt, repressing the Muslim brotherhood which had once been welcomed as a democratic force, nowhere more so than in Turkey.

In 2014 I taught a segment on the fickle Western analyses of the Muslim brotherhood, in a Yale MA course on the History of the Present. By that point ISIS was on a rampage in Syria, the West was havering over intervention, Russia did intervene and then in 2015 the “refugee crisis” eclipsed every other issue in European politics. The AfD, formerly an anti-Euro party, mutated into the leading voice of anti-immigrant sentiment in Germany. Merkel, the dominant figure of the Eurozone crisis and the key to European diplomacy in the Ukraine crisis was thrown onto the back foot. It took a deal with Turkey to stabilize the situation.

At the time I was drafting an essay about the history of NATO and found myself thinking a lot about the role of Turkey during the Cold War in forming a cordon sanitaire between Europe and the Middle East. This helped to segment two distinct spheres of international relations, a division which Crashed was replicating just as it was being called into question by hundreds of thousands of desperate refugees fleeing through Turkey to Europe.

And then in the summer of 2016 the coup broke, sending Erdogan spiraling ever deeper into authoritarianism.

At this point I decided Crashed had to have a Turkish-Middle Eastern component. If it did not, it would not properly encompass the rippling global effects of the credit cycle even in Eurasia. Events like the “refugee crisis” and its ramifications would remain exogenous, rather than being made intelligible as endogenous to the complex of power and money that the book was trying to describe. Europe’s failure to craft an adequate response to the question of the Mediterranean, which frames the entire problem and compounds the disaster of American policy in the Middle East, would remain unaddressed. The result would be that I would be confronted by the objection, “but the “populism” crisis wasn’t due austerity, it was due the refugees”, without being able to give a systematic answer.

So, as I began the main writing push in the summer of 2016, I set myself to widening the base of the book so as to be able to encompass a Turkish thread through to 2015/2016. This would involve discussing European and American engagement with Turkey and North Africa since the early 2000s, the surge in FDI in Turkey, Egypt, Libya and Algeria, the commodity price cycle etc. Six months later, as the difficulty of making this encompassing move became obvious and at the urging of one of my editors, I abandoned the Turkish strand of the narrative.

At the time it was a considerable relief. Crashed was already capacious enough. Ukraine would serve as my geoeconomic/geopolitical bellweather. The decision no doubt contributed to Crashed being finished on time for the summer of 2018. On the other hand it also meant that publication coincided with the “Turkey crisis”, which had clearly been brewing for a decade, but which Crashed no longer addressed. And yet there I was being asked to appear on TV to talk about … Turkey.

Unpicking the warp and weft of uneven and combined development is a matter of fine judgments. Here, for what they are worth, are some fragments of the missing Turkey thread.

I

Since 2013 the so-called emerging markets have been facing waves of uncertainty and fluctuating capital inflows. Since 2016 they face the prospect of a sustained rise in Fed interest rates. After years of low rates, this makes dollar funding more expensive and sucks investors back into the US. That pressure is further exacerbated by the prospect of dollar appreciation. Since 2014 relative to DM and EM currencies the dollar has appreciated by 20-25 percent.

When one weak link in the chain of emerging markets breaks, this spreads fear throughout the entire category of assets. This happened with Argentina earlier in 2018. “As risk comes off” you can see those shocks to an entire class of assets affecting everyone e.g. South Africa.

Added to this since 2016 there is the scatter shot effect of Trump’s shotgun “diplomacy”. Mexico, Russia, China and Turkey have all been caught by these blasts. But none of these general factors accounts for the severity of the shock that Turkey is suffering in the summer of 2018. There is no doubt that at the heart of Turkey’s financial crisis is Erdogan’s highly idiosyncratic rule. Turkey’s crisis in the particular configuration of the summer of 2018 is made in Turkey. But that begs the question. How do we narrate Turkey’s recent history?

In recent years the Erdogan story has been cast in terms of the emergence of authoritarian, post-liberal, “populist” regime. In the background there is the question that all too readily surfaces, of the compatibility of democracy and Islam. But both of these story lines taken in isolation are reductive and misleading. Not only do we need to sidestep the cultural clichés, to get some grasp on Turkey’s trajectory we need to factor in international and domestic political economy and the geopolitics of Turkey’s fraught position in the Eastern Mediterranean, between Europe, Russia and the Middle East.

II

It is worth recalling how recently Turkey, Erdogan and the AKP still nestled within an end of history narrative of convergence with the West. In the Cold War Turkey had stood guard against Russia as NATO’s southeastern sentinel. In the same role it had also provided a seal between Europe and the violent politics of the Middle East. It was a momentous departure, therefore, when in 1999 at the European Council meeting in Helsinki, Turkey was announced as a candidate for EU accession.[1] The EU was formulating an expansive new agenda for accession and security policy. The Turks for their part seemed eager. After a “lost decade” marked by a brutal counter-insurgency in Kurdistan, internal political polarization culminating in the “bloodless, postmodern” coup of 1997, and spasms of economic progress marred by rapid inflation, Turkey’s elites were desperate to keep pace with the regional transformation being steered by Brussels. Turkey did not want to be left behind by former members of COMECON.

In the hope of stabilizing the economy, the Turkish elite adopted an IMF program. This would bring inflation down from over 45 % in 2002 to 8 % in 2004. But the immediate effect of stabilizing the exchange rate was painful. As the Turkish economy crash-landed in 2000 and 2001, the political class of the 1990s was swept away and the door was opened to the reborn Islamic political movement, rebadged as the AKP party. Made up of a broad-based coalition of formerly outlawed Islamist movements and moderate conservatives, the AKP presented itself as the representative of the Anatolian middle class, pro-European and pro-American. Both positions, the AKP leadership hoped, would shield it against intervention by the military guardians of Atatürk’s secularist legacy.

The AKP’s strategy succeeded brilliantly. In the wake of 9/11, Turkey would come to stand as an example of a liberal Islamic future that combined market economics with electoral democracy and the conservative cultural values of mainstream Sunni Islam. It was an answer both to Iran and Al-Qaeda. And this became all the more important as the invasion of Iraq descended into a shambles. The apparent willingness of the AKP to reach a settlement in Kurdistan was a godsend for the US, which needed to work closely with the Kurds of Northern Iraq if it was to have any hope of stabilizing Mesopotamia. The AKP seemed bent and using Kurdistan and the Kurdish migrants in Turkeys major cities as a vote bank. Erdogan appointed Kurds to key positions. Mehmet Mehdi Eker, agriculture minister between 2005 and 2015, and Mehmet Şimşek, finance minister from 2009 to 2015 both represented Kurdistan in his administrations.

But Washington’s vision went further than using Turkey to solidify the Northern flank of Iraq. In a remarkably public endorsement in July 2004 at the end of a NATO summit hosted in Istanbul President Bush announced that Turkey was “Europe’s bridge to the wider world”. Turkey’s “success is vital to a future of progress and peace in Europe and in the broader Middle East … America believes that as a European power, Turkey belongs in the European Union. Your membership would also be a crucial advance in relations between the Muslim world and the West, because you are part of both. Including Turkey in the EU would prove that Europe is not the exclusive club of a single religion; it would expose the ‘clash of civilizations’ as a passing myth of history…”.[2] As Robert Kaplan – of Mars and Venus fame – put it with characteristic aplomb: “Erdogan’s moderate, reformist Islam now offers the single best hope for reconciling Muslims—from Morocco to Indonesia—with twenty-first-century social and political realities.”[3] The Bush Administration had understood this too late to properly cultivate AKP support prior to its invasion of Iraq. Now it was up to the Europeans.

With strong US and IMF backing and the prospect of EU membership beckoning, AKP-led Turkey embarked on program of major institutional changes, ranging from abolishing the death penalty to establishing a powerful and “independent” bank regulator and pushing through a wave of privatizations. The opening of formal accession talks was rewarded by a remarkable surge in FDI. In 2006 Turkey attracted close to $ 20bn in FDI, putting it ahead of Poland, Mexico and Egypt in the Emerging Market rankings. Of this unprecedented flow, 60 % or more of came from EU/EFTA sources, with the Dutch, Greeks, French and Germans in the lead.[4][5] Amongst the leading sectors was the Turkish banking system that saw over $ 10 billion dollars of investment, overwhelmingly from European banks. Fortis, Dexia, Unicredit and National Bank of Greece all bought into Turkey, as did GE Capital.[6]

Between 2002 and 2007 the AKP presided over a period of 7.5 % per annum growth. Turkish incomes surged to a level that exceeded that of the poorer EU members. Nor was this ever merely about personal incomes. It was about Turkey’s global standing. In 2006 Prime Minister Erdogan declared that by 2023 Turkey should become the tenth largest economy in the world. Turkey envisioned itself as a regional economic power. Exports to booming Gulf economies surged. Turkey was a prime supplier of the gigantic construction sites in Dubai as well as the American military in Iraq. Trade with South Eastern Europe and particularly with EU members Romania, Bulgaria and Greece flourished.

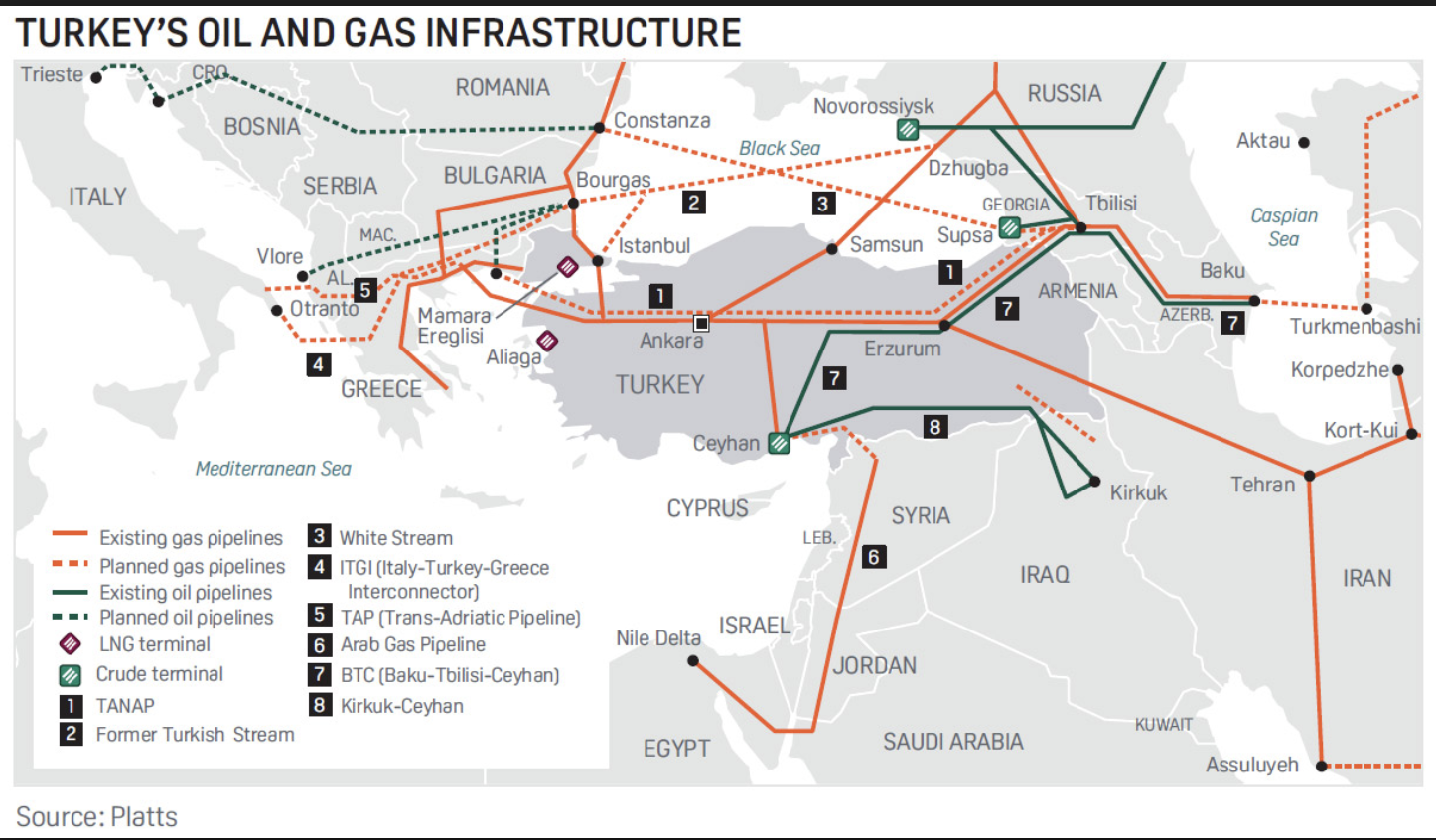

Already in the 1990s Turkey had emerged as a major energy hub between the Caspian and Western markets. It was crucial to the US vision of a East-West Energy Corridor, by-passing Russia and Iran. The $ 4 billion Baku-Tbilisi-Ceyhan pipeline opened in May 2006 was one of the largest in the world, pumping 1 m barrels a day. And in the complex energy politics of the post-Cold War period Turkey played all sides. It needed to. After China, Turkey’s demand for electricity was growing more rapidly than anywhere else in the world. In the early 2000s, 64 % of Turkey’s gas supply came from Russia. The Blue Stream pipeline built by a partnership between Italy’s ENI and Russia’ Gazprom came online in November 2005 after a ceremony attended by Berlusconi, Putin and Erdogan.[7]

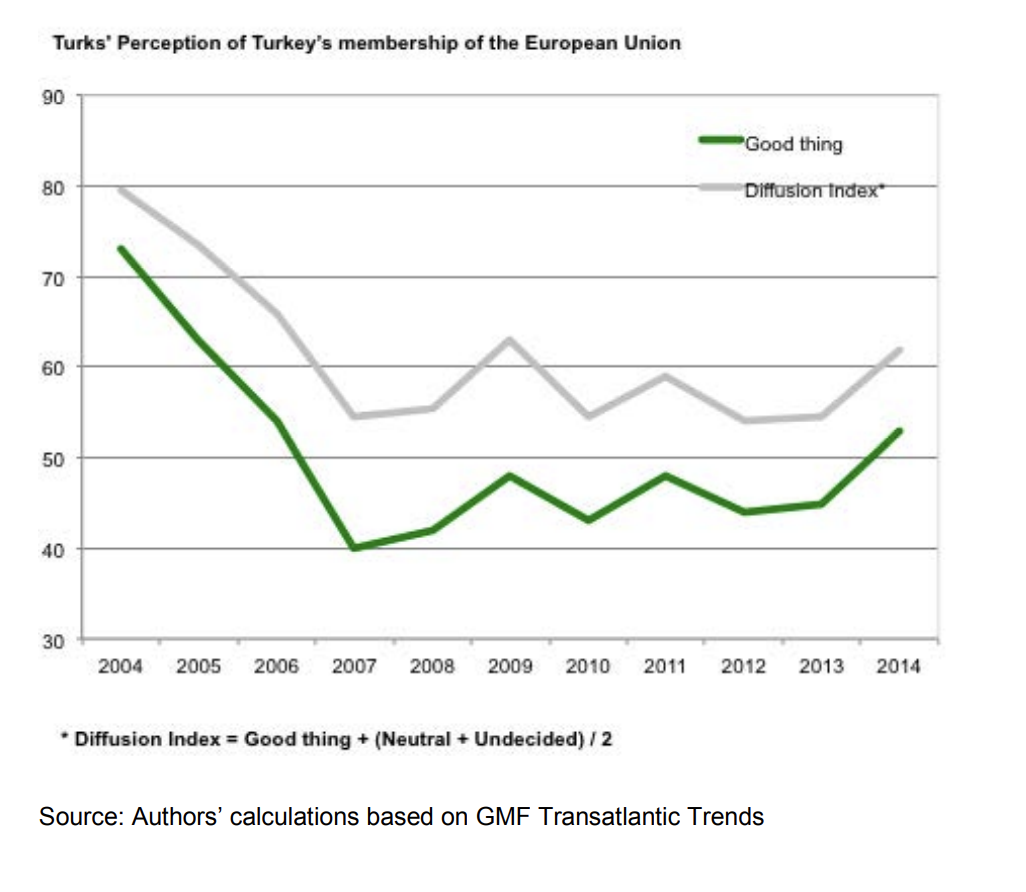

There was thus a compelling logic for Turkish EU accession. Carl Bildt, who became Sweden’s Foreign Minister in 2006, strongly supported Bush’s expansive vision of European engagement with the Greater Middle East. Turkish EU membership “ would give the EU a decisive role for stability in the eastern part of the Mediterranean and the Black Sea, which is clearly in the strategic interest of Europe”, he declared.[8] Poland and the UK took a similar view. But powerful voices spoke against. The right-wing populists ruling in Austria and Angela Merkel’s newly elected CDU-led government in Germany preferred negotiations leading to privileged partnership short of membership. Paris was strongly opposed to Turkish entry into the EU. Whilst Turkey’s relations with Greece were transformed beyond recognition, Cyprus remained a sticking point. Disastrously, the EU admitted Greek Cyprus in May 2004 as a full member without requiring it to come to terms with the breakaway Turkish North. In December 2006 at the behest of Cyprus, the EU slowed down negotiations with Turkey. As 2007 began EU expansion commissioner Oli Rehn was warning of a “train crash” in the negotiations. And the block against Turkish membership was further reinforced with the election of Sarkozy in France. EU hesitancy in turn reinforced hostile voices in Turkey. Though the AKP leadership remained nominally committed to pursuing membership, the opposition was increasingly skeptical. Amongst the wider Turkish public, support for EU membership plunged from 63 % in 2005 to only 40 % in 2007.[9]

Source Acemoglu and Ucer 2015

The AKP’s strategic gamble came to a head in 2007 when after having proposed a notably Islamic candidate for the Turkish presidential elections, they were faced with rumors of a military coup and renewed action against them in the courts. Rather than backing down, the AKP went to the polls, won a crushing victory over its rivals and rode out the legal attack. In the wake of this victory, Erdogan no longer needed the EU to cover him against the threat of a coup. Even if it would not culminate in EU accession, international economic integration seemed to be delivering the goods in economic terms. Ironically, Turkey’s rapid economic growth, supercharged by the expectation of progress towards stabilization and EU membership, made Erdogan and the AKP leadership more comfortable with the idea of “going it alone”. Euroasianism emerged as an alternative to the European turn. In grandiloquent terms, Turkey’s foreign policy guru Ahmet Davutoglu declared that based on its size, population and deep history and cultural power, Turkey could claim a place alongside Brazil, India and China as one of the new powers of the global system.[10]

For the Americans, the EU’s failure to embrace Turkey, was a telling sign of the incoherence of European strategy. As US Defense Secretary Robert Gates put it, if Turkey was drifting out of the Western orbit, it was “in no small part because it was pushed, and pushed by some in Europe refusing to give Turkey the kind of organic link to the West that Turkey sought.”[11] This was a fair comment, but it conveniently ignored the devastating impact on Turkish public opinion of America’s War on Terror. If the Turkish public were no longer as enthusiastic as they once were about the EU, they were by a large margin the most hostile to the United States within NATO. What Washington was lamenting was the failure of European incorporation to offset the unpopularity of America. Instead, the two together managed to trigger a general anti-Western turn.

III

Turkish conformity to Western expectations that marked the period from 2001 to 2007 was far-reaching and found its concentrated expression not just in the flow of foreign investment but in the surprising stability of the lira exchange rate, which remained level against the dollar for most of a decade.

That stability did not last. Since 2010 the lira has drifted progressively downwards, before entering its current precipitate decline. What combination of economic, political and geopolitical factors contributed to this break?

The turn by Europe against Turkish EU accession in 2007 and the AKP’s decisive domestic political victory, were the first of a series of shocks that broke the dream of the AKP as the vehicle for convergence between Turkey and the West.

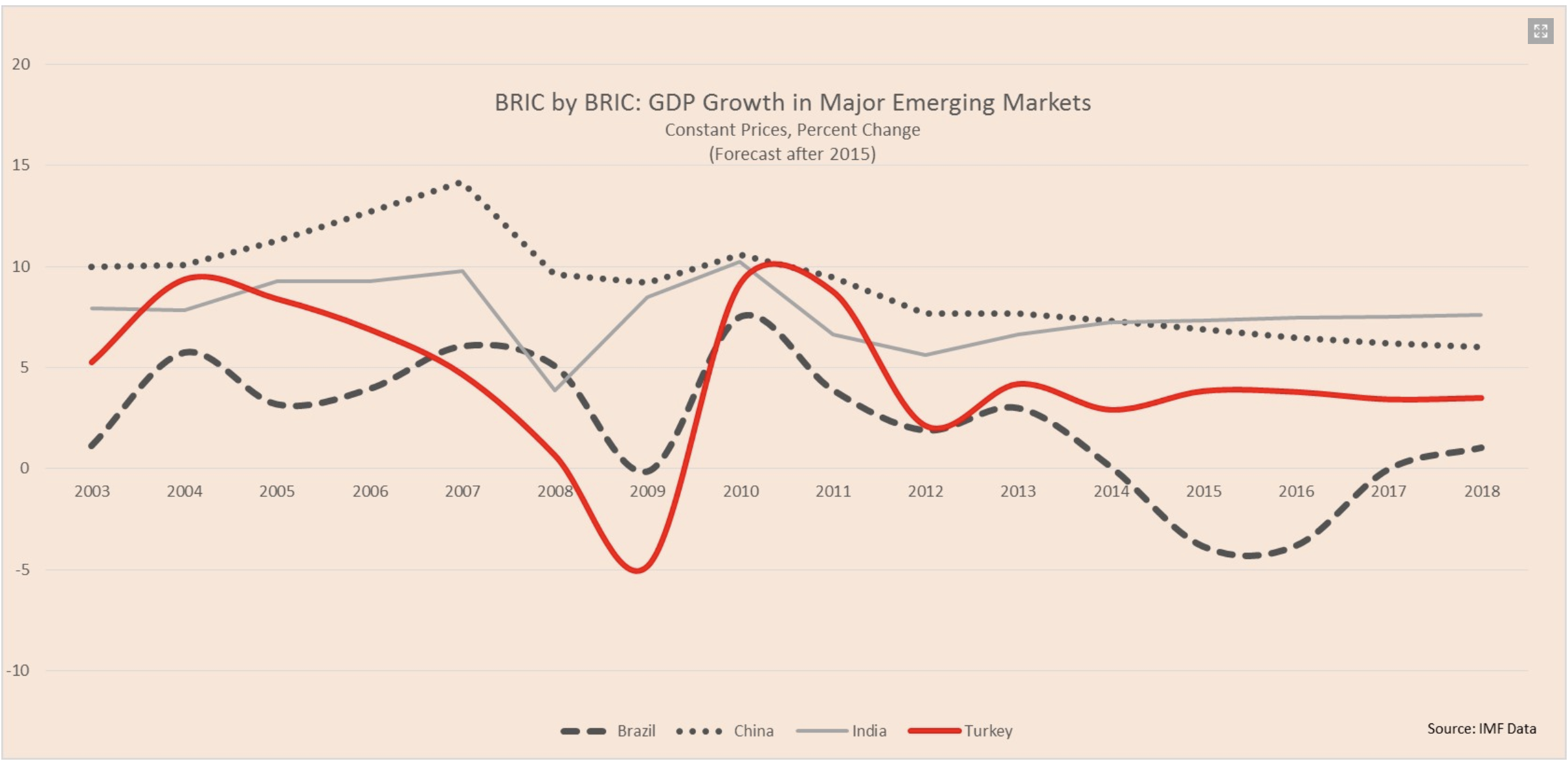

The 2008 financial crisis hit Turkey hard. Turkish GDP declined by as much as 14 % between 2008 and 2009. It was a worse crisis than the stabilization crisis of the early 2000s.

Source: GED

The Arab spring of 2011 turned into a disaster for Erdogan. Ankara was one of the chief backers of the Muslim brotherhood in Egypt, who were ousted from power by the military coup of 2013.

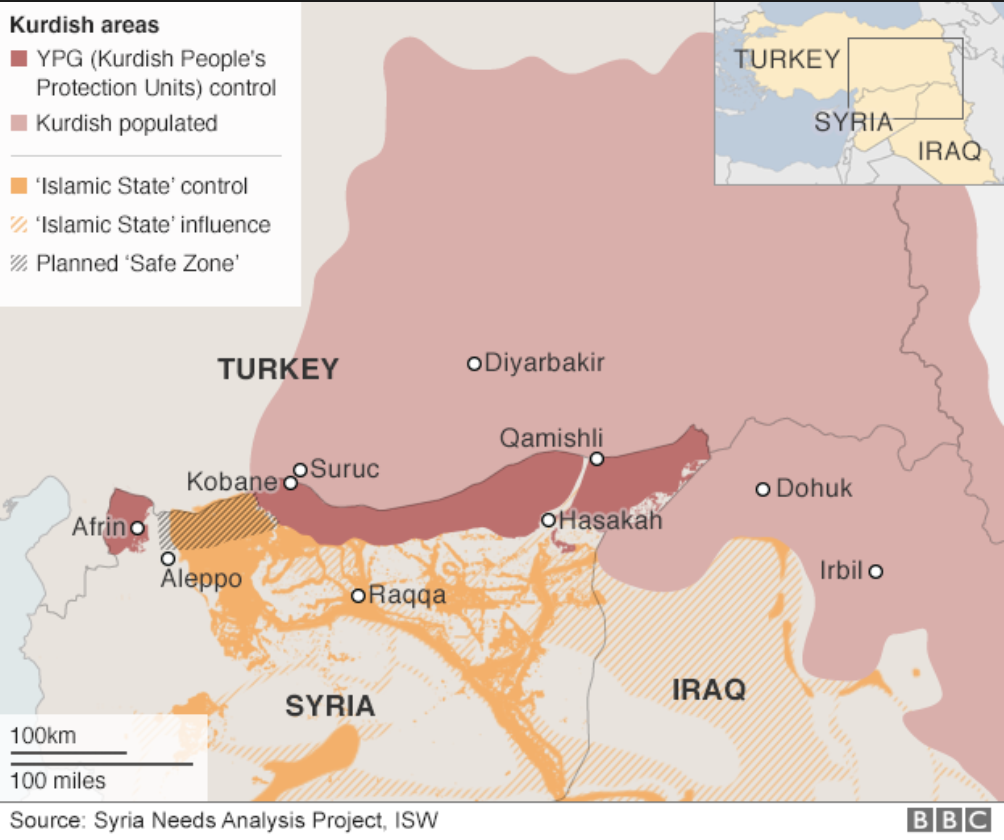

If Egypt was a setback, in Syria the Arab spring turned in a far more dangerous direction. As the protests in Syria escalated after 2011 into a bloody civil war, Turkey found itself facing a series of threats:

(a) Assad’s regime refused to fold and, instead, eventually sucked Russia back into the region as a major player.

(b) The best-organized anti-Assad forces in the North of Syria, along Turkey’s border was the Kurdish insurgency heavily backed by the United States, over Turkish protests.

(c) Islamic radicalism spread from the battlegrounds of Iraq. Turkey originally sought to instrumentalize these forces as a weapon against Assad and the Kurds (in cooperation with the CIA and Saudi). But ISIS developed into a lethal independent movement.

(d) The escalating bloodshed across Syria unleashed a truly gigantic flow of refugees for whom Turkey became the principal safe haven. The stresses it has faced in coping with an inflow of 3.5 million people of which almost 900,000 are children dwarf any “refugee crisis” experienced in Western Europe.

On top of these external pressures and setbacks, Erdogan faced serious domestic political threats including the emergence of HDP party as challenger for Kurdish votes and the wave of nationwide protests emanating from Gezi park in 2013.

Erdogan’s increasingly defiant attitude towards the West, already visible after the 2007 showdown, was reinforced by this series of shocks and by the repercussion of his own inept maneuvering.

In political terms, from 2011 he pushed a more aggressive campaign against the opposition. Initially this was backed by Fethullah Gülen’s religious movement, which was a useful weapon to wield against both Kemalists and the left. The most radical aspect of this campaign was Erdogan’s decision to break open the Kuridsh question. From the summer of 2015 the Turkish military ended the ceasefire with the PKK and dramatically escalated the war in Kurdistan. This unleashed devastating counter insurgency warfare on both sides of the Turkish-Syrian frontier.

These factors help to explain Erdogan’s lurch towards authoritarianism and his increasingly belligerent attitude to Western markets and analysts. The taper tantrum unleashed by Ben Bernanke’s comments about Fed interest rate policy in the spring of 2013, coinciding with the Gezi protests and the Sisi coup in Egypt was as far as Erdogan was concerned no coincidence. It was clearly a power play by the West to humble Turkey along with the other EM upstarts. By 2015 Erdogan was openly courting alliances with Russia and China.

What set up the conditions for the current crisis was the coincidence of this aggressive consolidation of Erdogan’s regime consolidation with its economic counterpart: credit-fuelled growthmanship.

IV

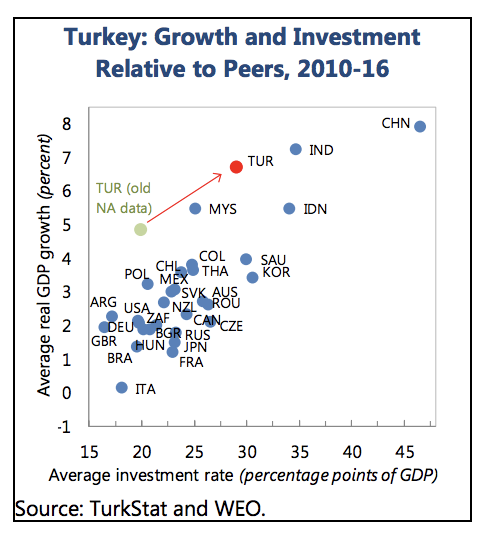

After the shock of 2008 Erdogan was bent on continuing to deliver rapid growth in an environment that was far less propitious. His aim is to raise Turkey’s GDP to $ 2 trillion by 2023. So far that goal is elusive but the reality of economic transformation is undeniable.

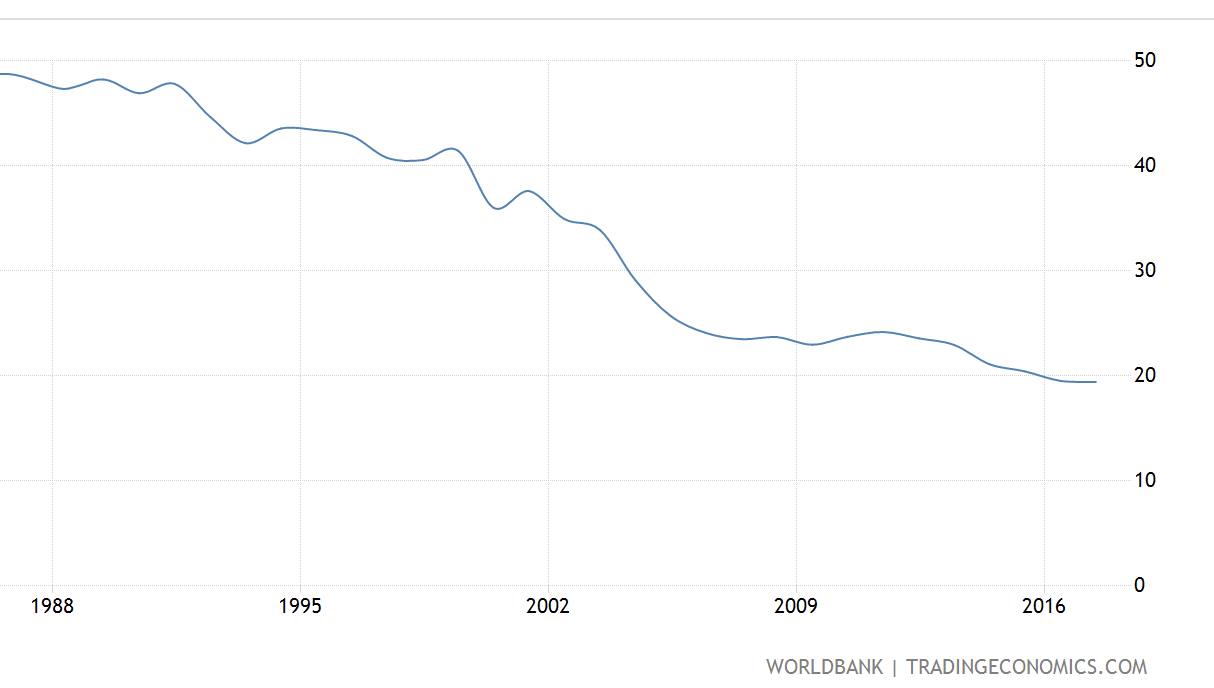

Since 2000 employment in agriculture has halved from 40 per cent to less than 20 per cent; the infant mortality rate dropped from 32 per 1,000 live births to 11. The share of health expenditures in total government expenditure increased by about 6 percentage points from 11% in 2002 to 17% in 2007 and that of education, from about 10% to almost 14%.

Share of agriculture in Turkish employment:

Over the last decade, the principal drivers of Turkey’s growth have been construction and services, not export-orientated manufacturing. Erdogan has pushed forward huge project such as the third bosphorus bridge, a new airport and the spectacular canal project to bypass Istanbul. Earthquake-proofing a large part of the country will cost perhaps as much as $400 bn. There are huge road construction and pipeline projects and a nuclear reactor program.

Source: IMF 2018

Mosque and palace building add symbolic effect, staking Turkey’s claim to be a leading force in Islamic modernism. As an article in Foreign Policy comments: “Turkey’s megaprojects are loaded with symbolism. The Camlica Mosque, a signature Erdogan project, towers over Istanbul on its highest hill. A new opera house being built on Taksim Square is being planned by the son of the architect who designed the cultural center it is replacing. A controversial new Ottoman-style mosque is near complete on the opposite side of Taksim. The Yildiz Palace, once the residence of Ottoman Sultan Abdulhamid II, has been designated Erdogan’s residence in Istanbul.”

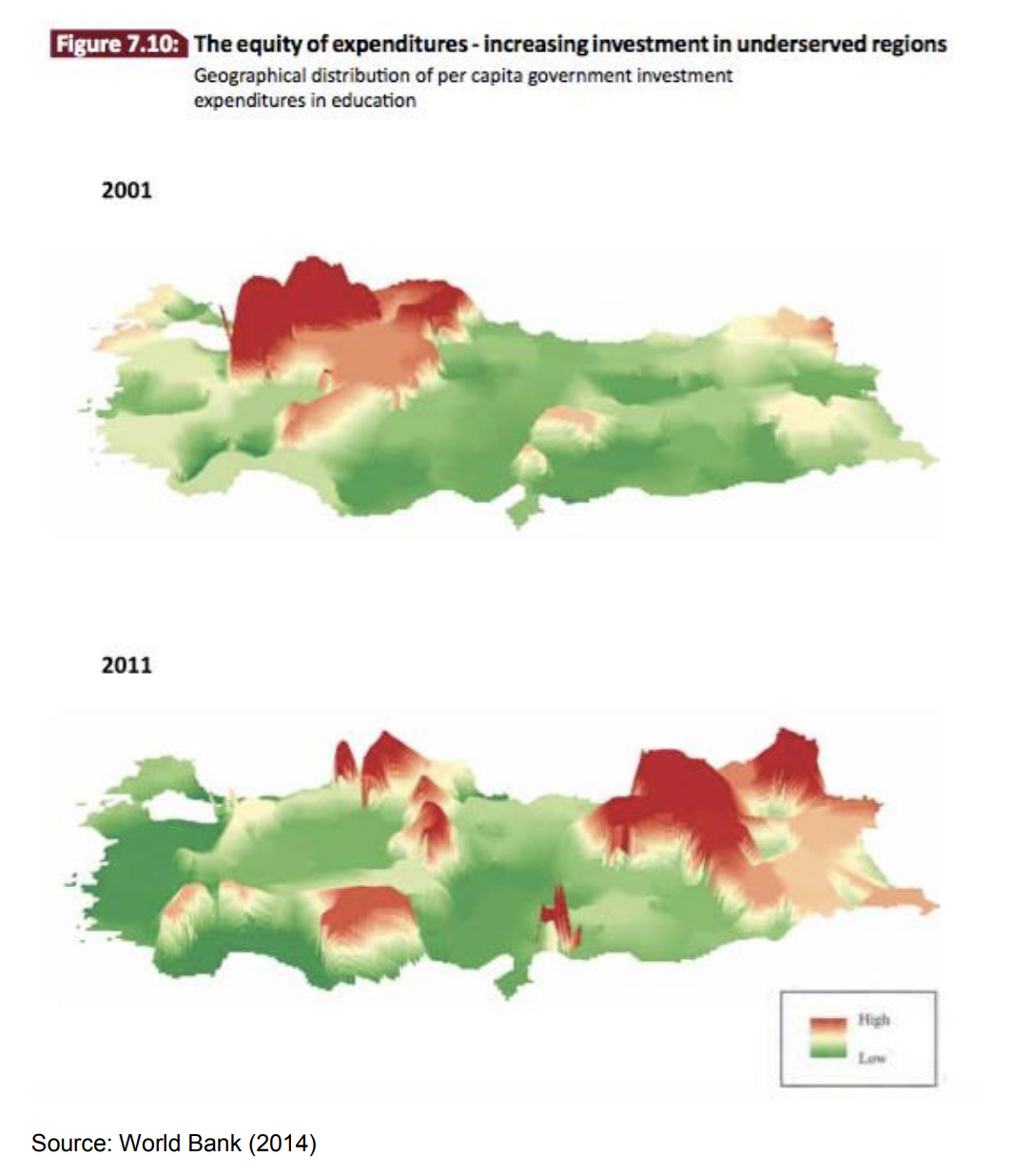

But though Erdogan’s Istanbul projects are eye-catching, the overall balance of public investment has shifted from the West to the East of the country.

Source: Acemoglu and Ucer 2015.

The projects do ideological work, at the same time as they reshuffle Turkey’s political economy. The leading Turkish business conglomerates Koç and Sabançi have done well out of Turkey’s growth, but they look askance at Erdogan’s politics. And Erdogan has reciprocated this mistrust. The AKP has not forgotten the coup of 1997 and the complicity of the elites. Erdogan regularly attacks the spokesmen of the leading business lobby TÛSIAD for their lack of loyalty.

Rather than the established big business interests Erdogan has cultivated entrepreneurs with AKP connections. Construction is a boom area with the firms and their lobbyists feeding of the ambitions of Erdogans regime.

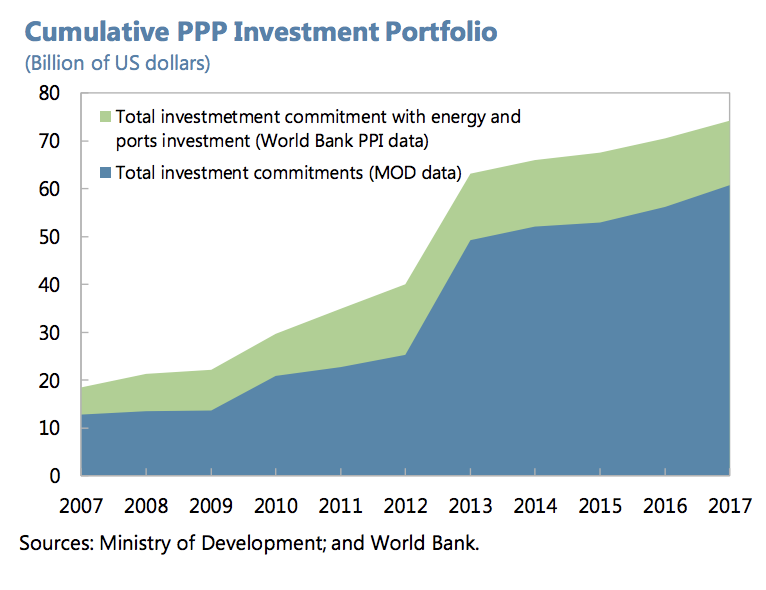

The volumes of money flowing through these public private partnerships are considerable. The last IMF report on Turkey ahead of the current crisis suggests that the stock of public private partnerships has surged from $ 20 bn to over $70bn since the crisis. Such spending generates jobs and profits. But it was also those projects that triggered the Gezi protests of 2013.

In addition Turkey has also been spending heavily on the refugee crisis has. According to official figures, this has required spending of $30bn since 2011. The WHO puts health service spending on the refugees at $10bn , making Turkey the largest spender on refugee health care in the world. Unlike most recipients of refugees Turkey has adopted a non-camp approach to accommodating the refugees and has relied on central government spending rather than NGOs to assist them. Economic studies have found substantial multiplier effects from this expenditure.

All of this added up to a considerable extension and deepening of the regime’s grip. But this was a private sector boom. Turkey did not run huge public deficits or pile up a vast sovereign debt. The current crisis in Turkey is not about sovereign debt. Even Erdogan’s big infrastructure project are public private cooperations. What propelled the economy was a private sector boom, fuelled by private sector credit.

This had the effect of increasing Turkey’s vulnerability to external shocks precisely as Erdogan’s regime was becoming increasingly embattled in international terms. This would have been moderated if Turkey was an export-driven success story or its balance of payments was propped up by long-term FDI. But it is not. Exports and FDI, both lagged eastern europe. Deep integration into value chains was limited to motor vehicles. Rather than playing on cheap labour costs, Erdogan’s regime has lifted the minimum wage rendering Turkey less competitive than the lower cost EU member states especially in the wake of the crisis.

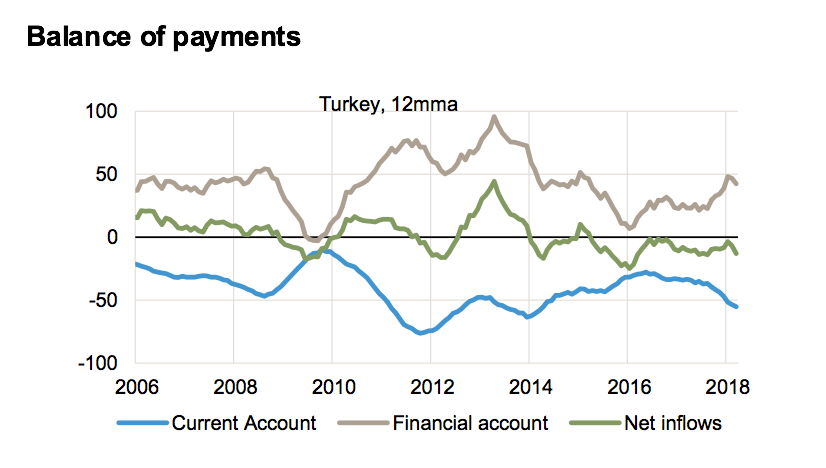

The combination of relatively weak exports and booming domestic demand has been a large and persistent current account deficit funded by capital inflows, much of which are short-term.

Source: Paul McNamara GAM

A key element in this deficit is imported oil and gas. Turkey has virtually no energy resources of its own. So any growth that boost energy demand results in a larger import bill. Upwards of 60 percent of Turkey’s current account deficit is accounted for by the deficit in energy alone.

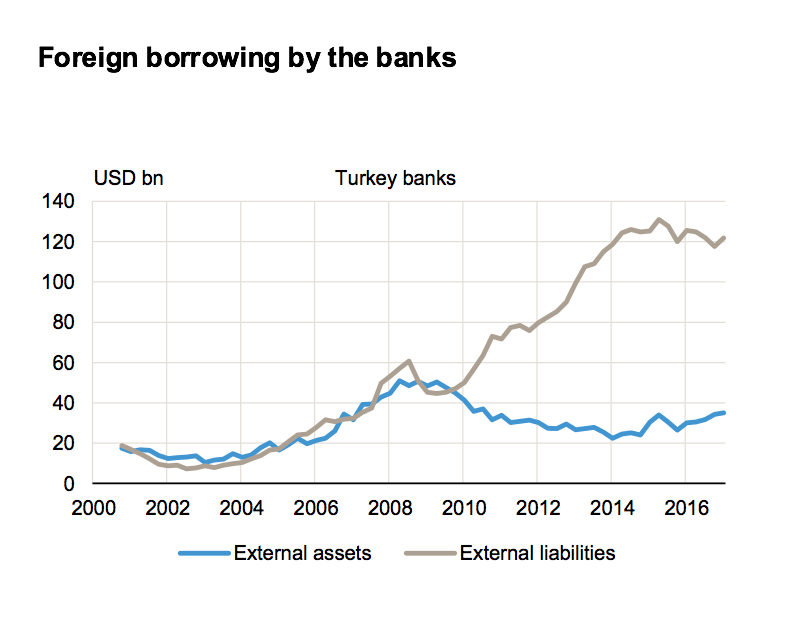

Added to these trade-driven flows, Turkey’s corporate sector has been borrowing on a large scale in dollars. Turkish banks drew in cheap foreign funding on a huge scale. Whilst European banks were dialing back their dependence on dollar funding, Turkey’s banks gorged.

Source: Paul McNamara, GAM

The contradiction in this combination of nationalist politics underpinned by a private sector boom is that it tends to increase your interdependence with the world economy. Turkey’s foreign-funded private credit boom and current account deficit make it vulnerable to a “sudden stop” shock to external financing. When dollar funding is cheap and oil prices are depressed, Turkey’s economic balance was sustainable. It was only a matter of time however before conditions turned. But Erdogan remained belligerent. “Erdogan seems to think that advanced industrial democracies and their greed protects him from any exposure,” says Selim Sazak, a Washington-based fellow at the Delma Institute, an Abu Dhabi think tank. “He says, ‘If the Dutch don’t like it, let Unilever close shop. If France doesn’t like it, Renault can leave.’”

V

2016 began with news of the Turkish army’s extraordinarily violent campaign in Kurdistan. The cities of Diyarbakır, Şırnak, Cizre and Nusaybin were made into war zones. Entire urban areas were being razed to the ground. Questions were asked about how far Erdogan would go. And then on 15 July 2016 came the coup. The political crackdown that followed has been amply reported. The economic policy response to the coup is the immediate backdrop to the current crisis.

Turning on its former allies in the Guellenist movement Erdogan has not just arrested his regime has expropriated large number of alleged plotters.

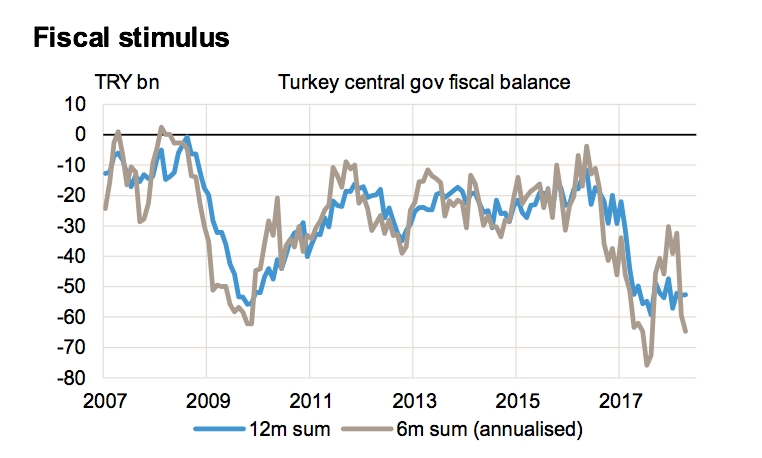

To offset the fall in consumption and investment, Ankara launched a fiscal stimulus. Inflation accelerated and expectations have become unanchored. Even tough interest rates no longer have much affect in slowing price increases.

Source: Paul McNamara GAM

Meanwhile to bolster the AKP base, the regime has offered a credit guarantee scheme for loans to small businesses, piling bad debts onto the balance sheets of banks and the accounts of the loan guarantee fund.

Trump’s election in November 2016 in the immediate aftermath of the coup, put Turkey in the crosshairs of market speculation. If US interest rates went up, pressure was predictable. But far from backing down, Erdogan ramped up the rhetoric about the interest rate conspiracy and continued his push to politicize Turkey’s relations with the world economy. Rather than seeking to calm markets Erdogan exacerbated fear. He appointed his son in law as finance minister. Mr. Albayrak, holds an M.B.A. from Pace University in New York, but his chief recommendations are his family connection and the fact that he worked as the United States representative for Calik Holdings, a construction and trading company that belongs to the inner circle of AKP-linked businesses.

Erdogan has never been afraid to intimidate the Turkish central bank. Overriding appeals from TUSIAD, from the summer of 2018 he effectively placed the bank under Presidential oversight giving himself the power to appoint its head. Meanwhile, trusted figures in the West such as Simsek, were dropped from the reduced cabinet.

You might ask why markets have been patient and why banks have continued to lend. The answer is profit. Turkey’s economic growth is real. There are profits to be made. The bank through which contagion is most likely to spread from Turkey to Europe is Spain’s BBVA, which has a controlling interest in Turkey’s number 2 bank, Garanti. It is worth recapping how it ended up with that stake.

Historically, Garanti’s controlling Turkish owner was the Dogus group. In 2005 they welcomed an investment by GE capital. GE capital was badly hit by 2008. It was looking to consolidate its business and in 2011 sold out to BBVA at a profit. BBVA then progressively increased its stake acquiring a controlling stake in 2017. Dogus, which was a major participant in Erdogan’s boom, was happy to release capital for investment elsewhere. BBVA for its part saw an attractive opportunity. In 2017 BBVA earned an interest margin of over 4 % on its Turkish business in 2017 as compared to 1 % back at home in Spain. At the end of 2017 it reported that Its Turkish franchise accounted for almost a third of its pre tax profit. Now, if it were to be wiped out in Turkey, BBVA would need to raise capital. It has become the chief channel for contagion talk in Europe.

VI

For me the analogies between Turkey and Ukraine are strong, not in the sense that Turkish and Ukrainian politics are similar, but in the sense that their sensitive geopolitical location makes them very different from other fragile EM borrowers.

Brazil, South Africa and Argentina may follow the same financial cycle, but they are not in zones of great power contest. The analogies sometimes drawn between Turkey and Russia are the most misleading of all. Not only are Russia’s foreign reserves far greater, but Russia is one of the players in the drama of great power contest, whereas Turkey has become one of the objects in the force field that Putin has created. Erdogan would like, of course, to be seen as a player in his own right, but, so far, his efforts have been frustrated at every turn.

It is this intersection of finance and geopolitics that explains why the chronologies of the Turkish and Ukraine crises are aligned. After 2013 both felt the force, first of the tightening of global credit conditions and then the stepping up of Russian power politics. But the alignment goes back to 2007-2008. Not only were they both hard hit by the global financial crisis. But this was also the moment at which the ambitious program of Eastern expansion of NATO and EU ground to a halt. From that point on, the disparity between dynamic financial integration in a zone of great power contestation with unclear geopolitical boundaries became ever more explosive. Turkey and Ukraine became predictable flashpoints as financial contagion merged with high stakes geopolitics.

For help with background reading for this post I would like to thank

Paul McNamara, GAM

and Cemal Burak Tansel.

[1] New empire, 216-7.

[2] Tugal, Cihan. The Fall of the Turkish Model: How the Arab Uprisings Brought Down Islamic Liberalism (Kindle Locations 58-62). Verso Books. Kindle Edition.

[3] http://www.theatlantic.com/magazine/archive/2004/12/at-the-gates-of-brussels/303623/

[4] New empire, 136.

[5] http://www.faz.net/aktuell/wirtschaft/die-tuerkei-zerstoert-ihr-wirtschaftswunder-14354387.html

[6] http://businessperspectives.org/journals_free/bbs/2007/BBS_en_2007_4_Bumin.pdf

[7] New empire, 217.

http://www.cfr.org/turkey/turkey-energy-crossroads/p17821

https://www.cer.org.uk/sites/default/files/publications/attachments/pdf/2011/essay_turkey_energy_12dec07-1381.pdf

[8] http://www.nytimes.com/2006/12/11/world/europe/11iht-sweden.3860723.html?_r=0

[9] new empire, 168.

[10] new empire, 110.

[11] http://www.spiegel.de/international/world/the-anatolian-tiger-how-the-west-is-losing-turkey-a-700626-druck.html