It’s Valentines day. So my first thought was to do a quick piece on Trump, chocolate and NAFTA. You know … can’t build your wall without Mexican concrete. Can’t celebrate St Valentine without chocolate from Mexico. Mexico, …. you know …. the place where the stuff actually came from! But, as I started digging, it just turned out to be far more interesting than that.

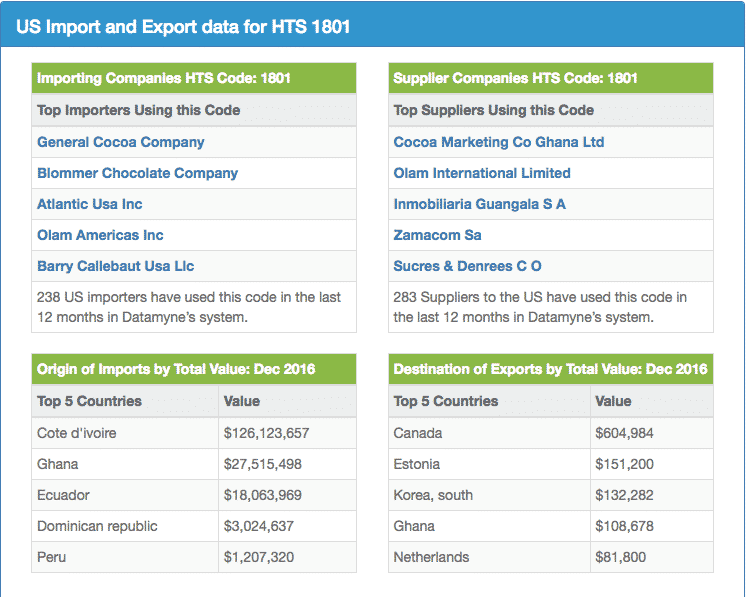

You start by figuring out that the international standard tariff classification for chocolate is HTS 18. Then it turns out there are these amazing databases that allow you to track what comes into the US and where it comes from and who ships it and where they ship it from.

http://www.datamyne.com/hts/18

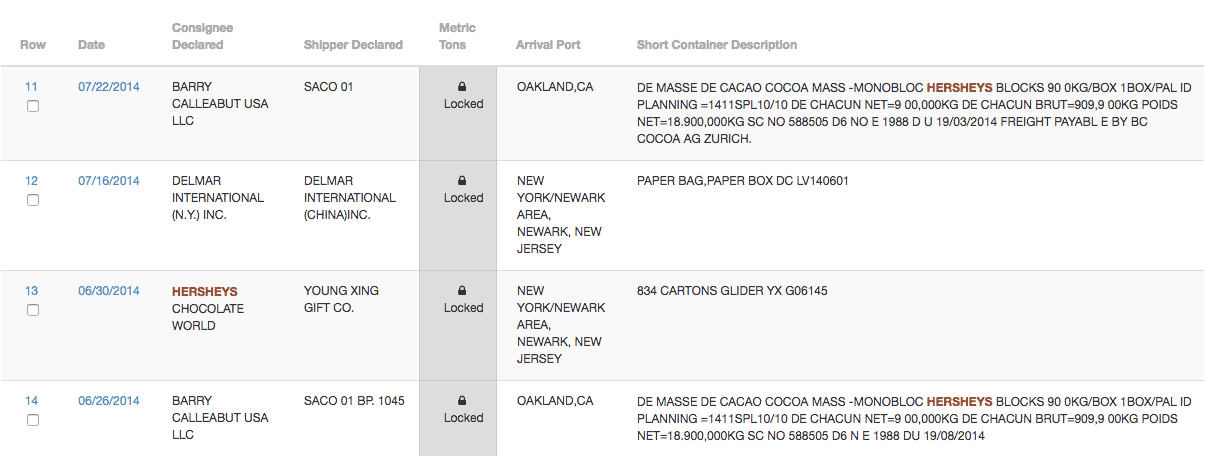

In fact, you can go down to the level of the individual shipment and the firms doing the shipping. The database I stumbled on allows you to enter the name of an importing company e.g. Hersheys. It then itemizes the individual shipments arriving in the US for Hersheys. Below you have a series of containers delivered for Hersheys to Oakland’s container port in 2014. Cocoa mass 18.9 tons at a time … at least I think it is 18.9 tons. 20 tons being pretty standard loading for a container.

To be able to track individual shipments on a public database is pretty mind-blowing. But who or what are Barry Calleabut USA LLC? And where does the cocoa mass come from?

It turns out, shouldn’t really be any surprise I guess, that the major source for cocoa beans for the US is West Africa. Cote d’Ivoire is far away in the lead. In fact, Côte d’Ivoire (1.5 million tonnes), Ghana (842,000 tonnes) and Indonesia (447,000 tonnes) account for 68 percent of the world’s output of c 4.5 m tons per annum. To translate tons of beans into chocolate bars, multiply by a factor of 7250. 4.5 m tons * 7250 … that’s a lot of chocolate bars! Just short of 33 billion.

So this is a classic post-colonial story. Indeed, it may be the classic post-colonial story given the role that the crisis in the cocoa industry in post-independence Ghana after 1957 played in inspiring Kwame Nkrumah’s diagnosis of neo-colonialism. Sixty years on, what is striking is how little the basic structure of this narrative has changed.

At the one end of the story we find a booming global market for chocolate. Us and our chocolate cravings. Total sales are estimated at $ 150 bn plus in 2014. Demand in India and China is surging as new groups of customers discover the taste for chocolate. Currently, chocolate sales in China are a mere $ 1.5 bn. Thats barely more then a dollar per head! Hersheys and others are scrambling to establish new production facilities in Malaysia. Cargill is going into Indonesia to refine beans on the spot. Dedicated teams are taste-testing in Shanghai. It is like a rerun of the transformation of European tastes in the 18th and 19th century on a far vaster and industrialized scale. Currently, Asia which accounts for half the world’s population accounted for only 12 % of cocoa consumption. The room for growth is huge.

At the other end of the story are peasant producers. Cocoa is one of the main global crops still almost entirely dominated by small-scale production. 90 % of cocoa is grown on 5-6 m small farms. The farms, on average are only 2-4 hectares, yielding 300-400 kg per hectare. Under the pressure of demand, total cocoa acerage has doubled since 1980 from 4.7 m to 10 m hectares. This land is farmed by an army of 14 million workers in cocoa production. To put that in perspective, it is estimated that around the world there are currently 9 million men and women involved in the direct production of motor vehicles (only 700,000 of whom are in the US). So cocoa farming is a far bigger direct employer than cars. Altogether, the cocoa farmers and their families make up a population of 50 million, that’s more than the population of Spain. 30 % of Ghana’s population are thought to depend on cocoa income. Most of these farmers live in severe or even dire poverty.

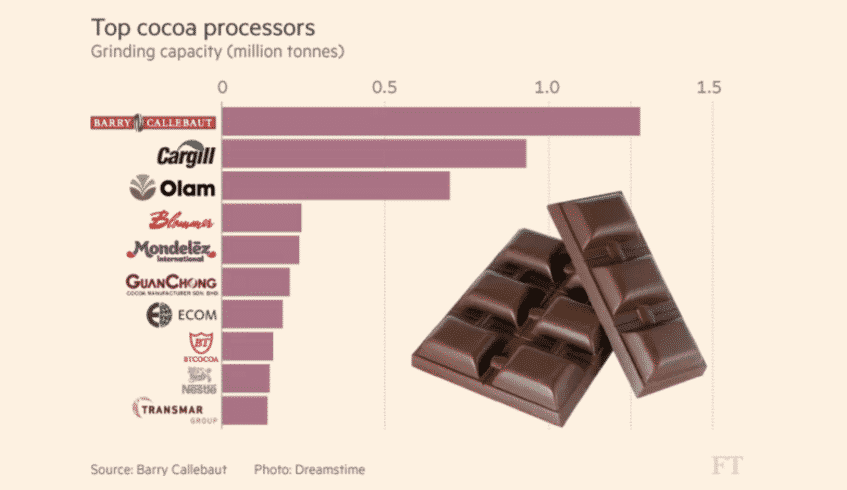

In between the peasant producers and the newly affluent consumers are a small group of highly concentrated global corporations that buy, ship, grind the cocoa beans and then another group of highly concentrated confectionary firms dominate consumer markets for chocolate. At the very top of the list of processors is the mysterious Barry Callebaut, who handled Hershey’s containers of cocoa mass at Oakland. With 1.5 m tons processing capacity Barry Callebaut can refine a third of the world’s total crop. They are thought to buy up c. 40 % of all the world’s beans available for free sale. The company was formed in 1996 out of a Franco-Belgian merger. The parent firms go back to the colonial period . The amalgamated giant is listed on the Swiss stock exchange.

Apart from Barry Callebeaut, many in the list of top cocoa processors are familiar, Cargill (the huge agro-industrial multinational who entered cocoa in the 1990s) and Mondelez (formerly Kraft) are familiar. Olam is a fascinating addition to the global picture. It emerged out of a Nigerian cashew trading business and is now a global agri-industrial competitor based in Singapore. It is heading an aggressive and controversial land grab in highly vulnerable Laos and is clearly a name to watch.

https://www.ft.com/content/f5098c08-e8a0-11e6-967b-c88452263daf

So it’s a remarkable hour-glass shaped industry, supplying the comfort-eating needs of billions of consumers, from the labour of millions of dirt-poor peasant farms, by way of a few dozen gigantic transnational corporate actors.

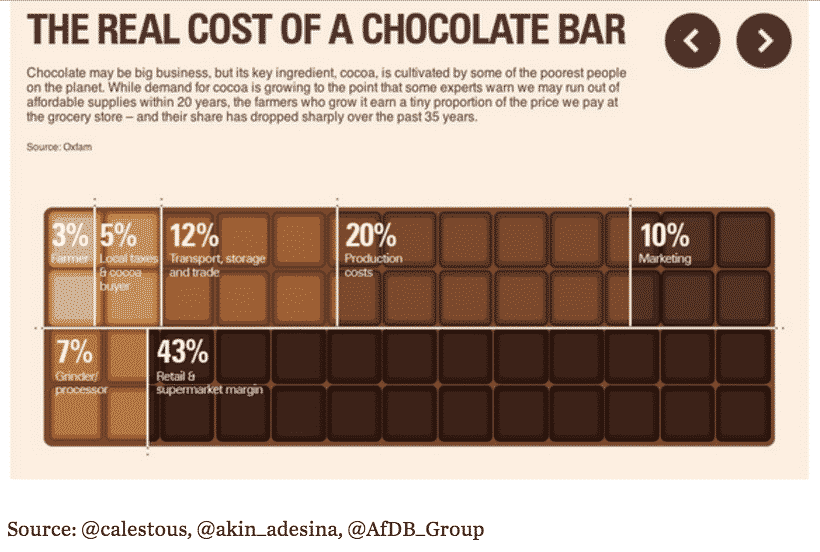

The most obvious and pressing question is one of exploitation. The farmers get a tiny share of the final value of the chocolate bar. The numbers are particularly shocking when viewed in historical terms. “When cocoa prices were high in the 1970s, cocoa accounted for up to 50 percent of the value of a chocolate bar. This fell to 16 percent in the 1980s and today, farmers receive around six percent of the value.” http://www.fairtrade.org.uk/~/media/fairtradeuk/farmers%20and%20workers/documents/cocoa%20commodity%20briefing_online7.pdf

Does the massive concentration in the industry cause farm incomes to be depressed? How can such poor and fragmented producers stand a chance against global multinationals? The question is nagging and pushed hard by NGO such as Fair Trade UK whose report I cite above. The problem from an analytical point of view is establishing causality. The situation of the farmers in Ghana and Cote d’Ivoire is so disadvantaged, in so many different ways that it is hard to isolate the specific effect of corporate market power. The big firms compete against each other. They have to fear potential entrants. Consumers are highly price sensitive.

UNCTAD, which one is used to thinking of as a relatively critical organization, published a surprisingly anodyne report on the subject, recommending general improvements for farming conditions rather than structural change in market power. http://unctad.org/en/PublicationsLibrary/suc2015d4_en.pdf

In the Netherlands, for historic reasons, the issue is particularly urgent. Indonesia is a former colony and it was in the Netherlands that chocolate in its modern form was invented in the early nineteenth century by van Houten. As as a result the Netherlands remains a major production center. Amsterdam is the world’s largest cocoa port. In 2015 the activity of NGO activist groups around the issue of fair trade in cocoa became so impressive that the Dutch parliament commissioned a report from a reputable, but business-connected research institute. http://www.seo.nl/en/page/article/marktconcentratie-en-prijsvorming-in-de-mondiale-waardeketen-voor-cacao/

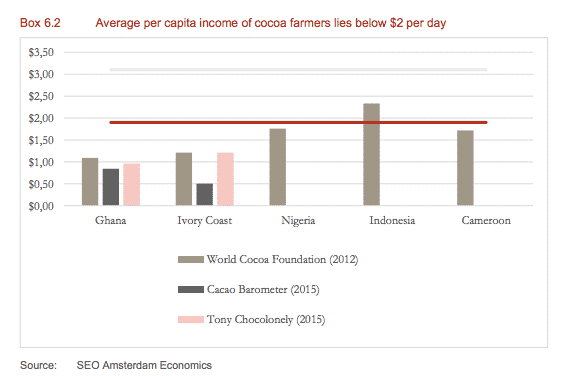

Whether one agrees with its conclusions its analysis is a truly interesting example of an effort to map market power and where it is applied. The crucial take away is that in Cote d’Ivoire and Ghana, by far the largest producers, it isn’t global markets that set the prices that farmers receive. It is local price boards, which stabilize the price paid to farmers, but also tax them, by passing on only a fraction of world market prices. Notionally, the tax is supposed to be reinvested or held in reserve for stabilization. But since these two countries have the lowest productivity of any producers in the global system, the results cannot be said to be encouraging. The politics of this kind of analysis are manifest. Cote d’Ivoire reintroduced price regulation in 2011 after decades of experimentation with liberalization that coincided with political turmoil. But what seems indisputable is that even if prices were raised to the global market level, the condition of the farmers is so desperate that it would not be sufficient to raise them out of extreme poverty.

With the well-known $ 1 and $ 2 per day standards for global poverty of the 1990s having been updated by the World Bank in 2015 to $ 1.90 and $ 3.10 respectively, the numbers for the cocoa farmers are truly alarming. The Dutch study shows that even if West African farmers received the full world market price and doubled their productivity, the most that could be hoped for would be a daily income of $ 2.40 i.e. just above extreme poverty.

Can an industry that relies on a workforce under such intense pressure be sustainable, either in human or environmental terms? Will we soon hit peak chocolate?

The plantations in West Africa are not in good shape. There is precious little margin for investment. The trees are old. So are the cocoa farmers whose average age is 51. In populations as youthful as that of West Africa that is remarkable. In fact, cocoa farming seems to be a business for old men and young children, 2.1 m of whom are used as child laborers in Ghana and Cote d’Ivoire.

But sustainability goes beyond investment and elasticity of supply. The crop is planted where it is, because of the sensitivity of the trees to precise climactic conditions. Currently, cocoa can only be grown 10-20 degrees either side of the equator. But those conditions are changing. The predicted two percent change in temperature may well have a devastating impact on the current production regime. Nor are these worries expressed only by climate change campaigners. Mars the largest US candy firm and Barry Callebeaut the largest processor are serious about climate change as a threat to their business. Nor is the threat long-term. They are reckoning with the distinct possibilities of shortages as early as 2020, as surging demand exceeds capacity growth.

And if climate change doesn’t get us, Frosty Pod and Witches’ Broom probably will. Serious diseases with silly names. They were responsible for largely wiping-out Central America and Latin America as major producers over the last couple of decades. Does ag-tech provide any answers? One of the problems on “improving” cocoa is that the plants take so long to grow. Whereas you can experiment with a new crop of corn three times a year, a cocoa tree takes 2 years to produce a crop and ten years before you can identify traits worth cultivating. But work continues and the main threat to our chocolate habit may in fact come from within, from a new strain of cocoa tree which is hardy, disease resistant and 7 times more productive than heirloom cocoa trees, but whose flavor is described as “weak basal cocoa with thin fruit overlay; lead and wood shavings; astringent and acidic pulp; quite bitter.”

The man with the best cocoa nose in the world, you cant make this stuff up, is a “Mormon grandfather from Hanover, Pennsylvania, named Ed Seguine, who …. in the 31 years he’s spent consulting … ” has “consumed some 300,000 chocolate samples and is so concerned with the potential erosion of flavor that he’s dedicated the remainder of his career to preventing it. He, too, has sampled CCN51 and describes its flavor as “acidic dirt.” NASTY!

Unless we “fight back”, cocoa may soon be going the way of the tomato in other words: plentiful, cheap but hardly worth eating. There is some hope in the form of the strains R1, R4 and R6 developed by the Centro Agronomico Tropical de Investigacion y Ensenanza, or CATIE. They are high-yielding, tough and tasty. But, as everyone acknowledges, the future of chocolate really depends on the African producers where the battle between flavor, yield and resistance is only just beginning. Take away: worry about the spread of the nasty new “mercedes” variety to Ghana and Cote d’Ivoire. Root for TCHO Chocolate Co. of Berkeley, California and Seguine who are trying to help the hard-pressed African farmers to find better options. https://www.bloomberg.com/news/articles/2014-11-14/to-save-chocolate-scientists-develop-new-breeds-of-cacao

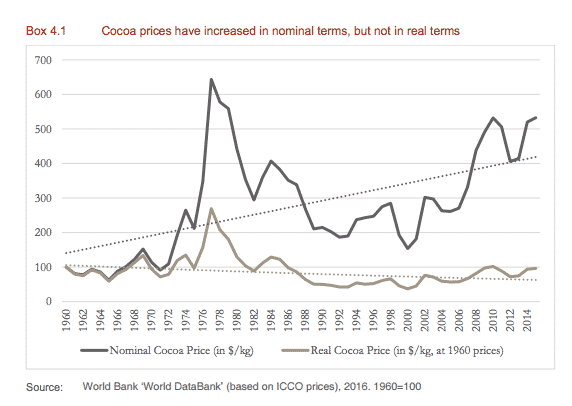

Meanwhile, the commodity market gyrates. With the nominal volatility disguising a long-term stagnation in real terms that is very serious. Cocoa today fetches the same in real terms for the farmers as it did in 1960!

And a further element of risk was added in the summer of 2016 by Brexit. What has Brexit got to do with cocoa you ask? Well, because of Britain’s imperial past, and the importance of Ghana as a producer, cocoa is one of the rare commodities that is priced in pounds sterling. Sterling has been gyrating under the impact of Brexit news. So, how much a poor peasant farmer in Cote d’Ivoire gets paid depends in some considerable degree on the insanity of British politics right now. One major trading house filed for bankruptcy over the new year disrupting supplies and causing price fluctuations.

Punchline 1: We should buy fair trade chocolate if we possibly can. Otherwise, willingly or not, we are consuming crops produced by some of the poorest and most disadvantaged people in the global value-chain. I think the point here is to be as specific as possible. Its easy to become blase about the inequities of the entire global trading system. But the farmers in the cocoa value-chain really are amongst the most disadvantaged of any foodstuff you can easily buy in a first world supermarket.

Punchline 2: Reading the report on cocoa pricing and peasants was like immersing myself again in Weimar Republic-era agronomy. It is astonishing how little the discourse of agrarian productivism and modernization has moved on. And it is presumably open to all the questions that critical historians, anthropologists etc relentlessly pose about this kind of vision of modernization.

Punchline 3: More of a question. How does this snapshot of agro-industrial globalization relate to the hierarchical vision of financial globalization, I’ve been banging on about in earlier postings, founded as that is in a hierarchy that pinnacles in the Fed. It’s a question I am going to gnaw away on in future posts.

In the mean time, happy valentines. This one’s dedicated to chocolate lovers and political economists in love!