I don’t normally write much about the UK – my relationship with the country and its politics will never recover from Brexit. But the current turmoil calls for an exception. Sterling’s collapse is of historic dimensions.

Source: FT

I did a short piece for the Guardian on trying to make sense of the crisis.

Like my comrade Daniela Gabor I fear this is headed towards austerity.

In 2010 Greece served the Cameron administration as a boogyman. Now the Truss team has actually managed to manufacture something akin to a bond market crisis.

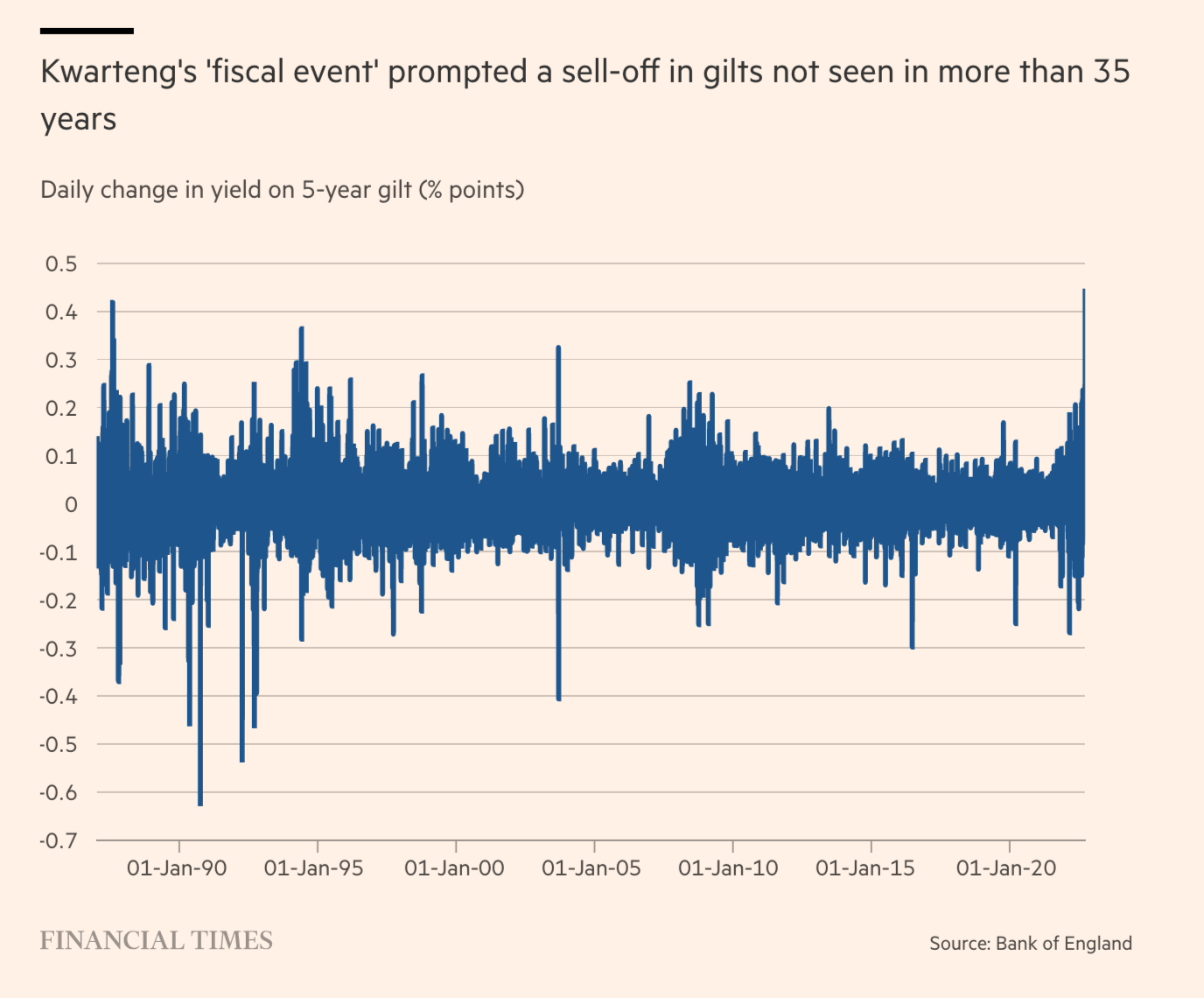

As the excellent Toby Nangle put it in the FT:

“Nothing in gilt markets in the past 35 years — not the UK’s ejection from the Exchange Rate Mechanism, 9/11, the financial crisis, Brexit, Covid or any Bank of England move — compares with the price moves in reaction to the chancellor’s mini-Budget”.

As bond markets sell off UK yields have accelerated past those for Greece and Italy.

And it is the reaction pattern that is so disturbing. For the exchange rate to fall as yields rise ought to be a matter of real concern.

Now, if the UK were actually a well-run emerging market, rather than an atrociously governed advanced economy, it would have foreign exchange reserves, which the Bank of England in extremis could use to stabilized the exchange rate – admittedly a freaky scenario. But, of course, advanced economies like the UK don’t hold substantial reserves.

So some normally sober voices have even discussed the possibility of opening Fed swap lines.

In trying to make sense of what on earth the tories are up to, you end up having to read conservative commentators. This substack by Ryan Bourne @MrRBourne is extremely useful. h/t @duncanweldon

What Bourne’s analysis reveals is that while Truss and Kwarteng see a positive role for supply-side reform and tax cuts and assign the Bank of England the task of keeping inflation in check – the Reaganite policy-assignment. They have no positive vision for the role of public expenditure. So it becomes the residual that must be cut to meet the budgetary constraint. This is the key reversal of the policy consensus since the 1990s.

As a guide to the Tory mind, I have also found the blow by blow commentary by @KateAndrs at the Spectator useful

I’ll admit that it was surprise to discover that Kwarteng has a PhD from Cambridge in economic history. This write up of his work by George Parker in Liverpool and Chris Cook was really interesting.

Some of the economic problems facing Kwarteng, however, are ones he has been considering for some time. His doctoral thesis, titled “Political Thought of the Recoinage Crisis”, is a survey of commentary from the late 17th century around the government of William III’s decision to reissue England’s coinage in 1695-6. Modern concerns over the rising cost of coffee echo the views of Sir Isaac Newton, who then held leading roles at the Royal Mint. Kwarteng cited him noting that a devaluation-induced rise in commodity prices was “Equipollent [equivalent] to a tax upon all other Estates” and tended “to make the Nation weary of the War, and uneasy under the Government”. Recommended Martin Wolf Kwarteng is risking serious economic instability The historical context of Kwarteng’s analysis makes it hard to draw many conclusions about his current views: one of the critical monetary problems at the time was people melting down, shaving or exporting coins for their silver. He certainly does not seem to endorse the position of pamphleteers he cites who feared the monetary monopoly of the then new BoE would cause another civil war. But the thesis does show how comments from his allies over the weekend blaming speculation by “City boys” for the weakness of sterling have a long heritage. Kwarteng notes that, even then, at the very start of London’s financial revolution: “None believed that the interest of the goldsmith and banker was anything but inimical to the wider good of the nation”.

Kwarteng is also the author of an epic history of money and power, in which he reveals his deep unease with fiat money.

Daniel Drezner summarized the plot in the New York Times. For Kwarteng

The history of money is one of oscillation between “periods of monetary chaos,” when governments issue fiat currency, and “periods of relative order,” when currencies are linked to gold. The bulk of “War and Gold” is devoted to observing that things seemed much, much better during eras when currencies were tied to gold. In his introduction, Kwarteng explicitly says he is not advocating a return to the pre-1914 gold standard. Rather than echoing Rand Paul, Kwarteng writes more like a Tory nostalgic for the solidity of Robert Peel in 19th-century England or the Eisenhower era in 20th-century America.

This is a dramatic vista no doubt. Meanwhile, in the autumn of 2022, the UK under Kwarteng as Chancellor now faces the prospect of a recession ahead. The main question is how severe that recession might be.

Critical to this will be the housing market. Real estate prices in the UK are chronically overinflated and this is the flywheel on middle-class and upper class wealth. Practically all mortgages in the UK have adjustable rates with fixed-rate being offered for at most 2-5 years. So the huge hike in interest rates is going to feed through to households in a dramatic way.

The shock to UK households will be huge.

For a country that has long been lingering in a painful stagnation, it is a grim prospect indeed.

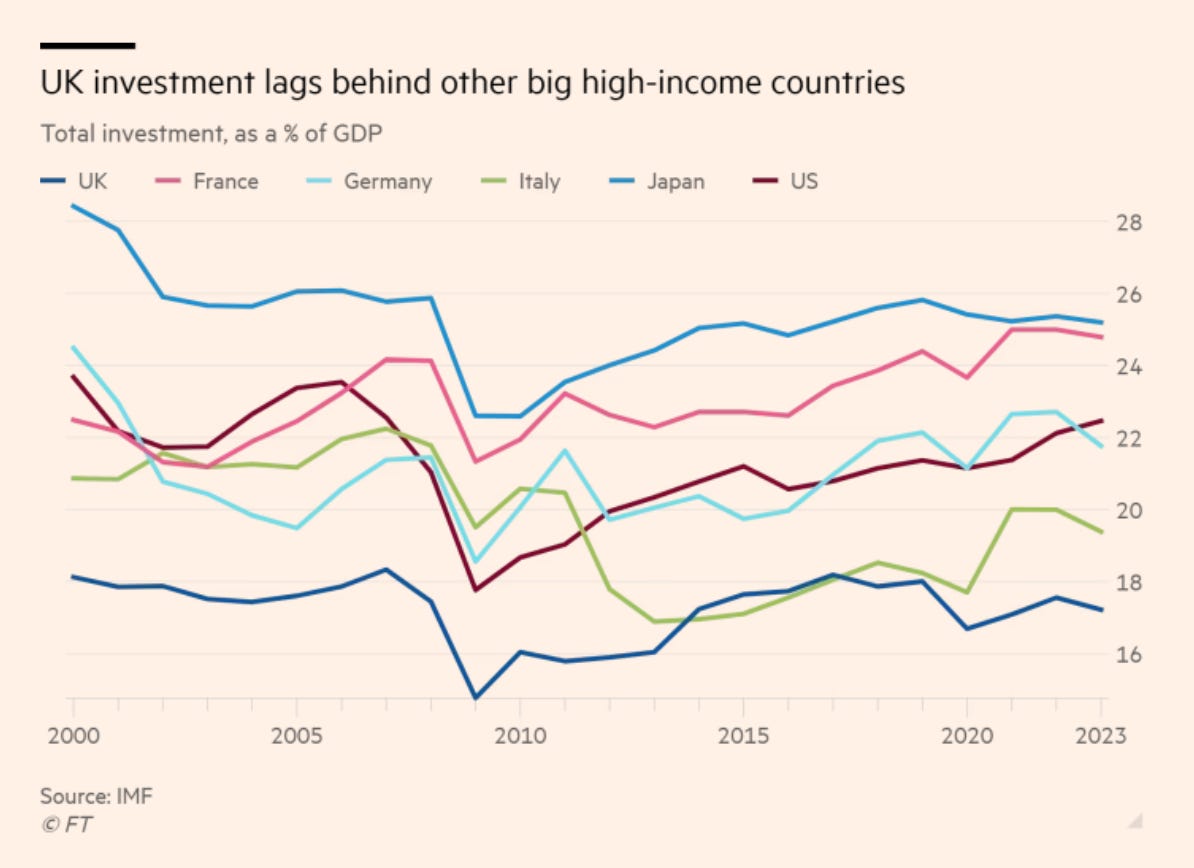

As Martin Wolf pointed out in a powerful critique of the Truss program, what the UK desperately needs is an increase in investment. The kind of drama unleashed in recent weeks in no way helps.

The UK will no doubt get over this shock. But the damage is done. As Toby Nangle puts it, in terms that could hardly be more English, “You can’t unburn toast.”

****

I love putting out the newsletter for free to thousands of readers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, there are three subscription models:

- The annual subscription: $50 annually

- The standard monthly subscription: $5 monthly – which gives you a bit more flexibility.

- Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.

Several times per week, as a thank you, all paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images.