Speak to anyone with close connections to China and one of the main topics of conversation, if not the main topic, is the double challenge of finding well-paid jobs and the outlook for real estate. Wealth accumulation through real estate supported by buoyant earnings, social mobility and income growth were key components of the China dream. They all now seem in doubt. And this comes as a shock.

It is worth stressing how novel both the China dream and its crisis still are. Homeownership in China surged from the early 1990s from very low levels to near universality by the 2010s.

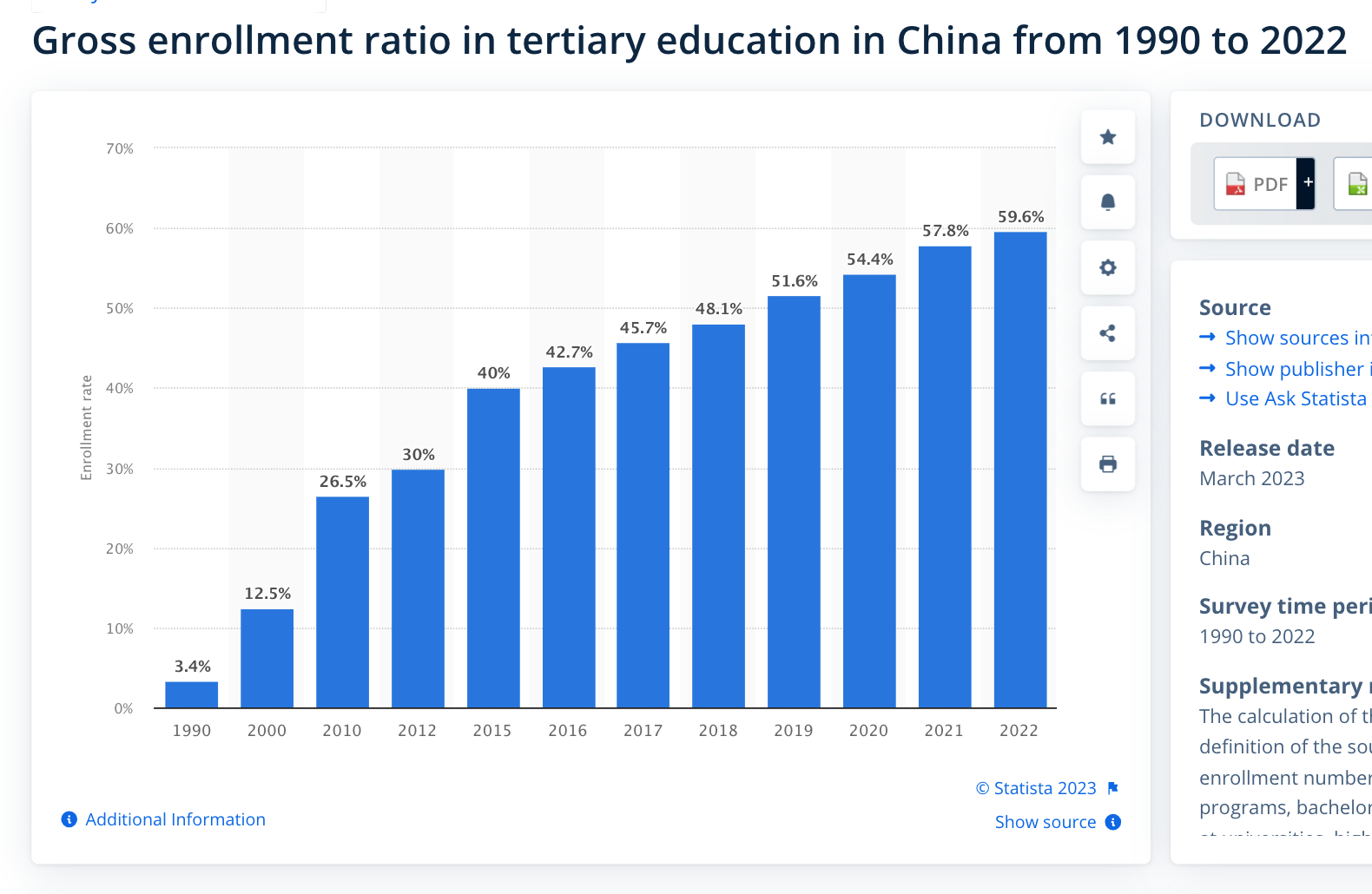

Trailing homeownership by a decade, access to higher education in China has expanded spectacularly. In a single generation between 2000 and 2022, tertiary enrollment in China has surged fivefold, from 12 % to 60 %.

Subscribed

This explosive, 25-year transformation in socio-economic circumstances has not been without its shadows. It is easy to forget how serious was the shock to the system in 2015-6, as reflected in home prices.

Over-construction has been a well-reported threat for many years. Many young people who bought apartments at peak prices are far from realizing large capital appreciation and know it.

The pressures in the educational system and in the workplace are notorious. Protests against 996 – a working culture of 9:00 am to 9:00 pm, 6 days per week; i.e. 72 hours per week were one of the cause célèbre of 2019.

But the current malaise feels different. The housing system seems broken, but apartments remain unaffordable in many Tier 1 cities. For those in the most desirable jobs, the pace is relentless and is compounded by the highly insecure prospects facing many in their middle age. For those entering the labour market right now the situation is even more bleak with unemployment for those between 16 and 24 well above 20 percent and thus worse, at least on the basis of a superficial reading of the data, than in the troubled economies of the Eurozone.

These numbers have to be interpreted with care.

Clearly, a lot of young people between 16 and 24 are in education. To be precise, right now there are roughly 96 million 16- to 24-year-olds in China, of which two thirds are in education and not included in the labour market numbers either as employed or unemployed. The unemployment rate of 21.3 percent rate refers to the 33 million who have ended their education and entered the labour market, of whom 6 million are still looking for jobs.

One common connection made in reports on Chinese youth unemployment is that the surge in unemployment is due to the huge numbers pouring out of China’s vastly expanded University and College system. 11.58 million university graduates will enter the job market this year. Those numbers are very impressive. They are truly ominous for those from second or third tier universities, many of whom are first generation college students whose families have everything riding on their academic success.

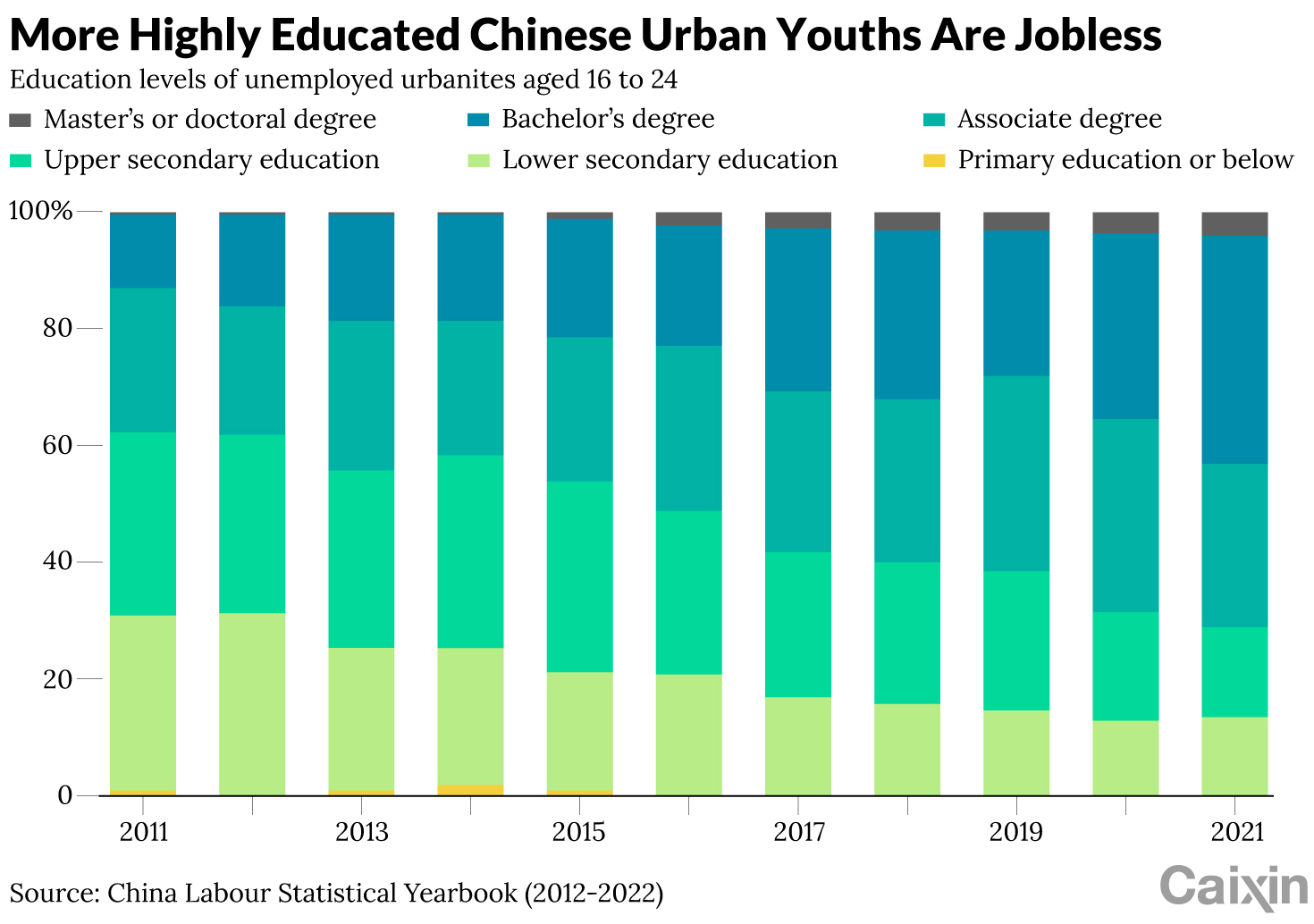

Unemployment for graduates comes as a shock. College-educated unemployed in China’s cities is a relatively recent phenomenon. Ten years ago the majority of young unemployed in cities had no College degrees. By contrast, in 2021 more than 70% of jobless Chinese urbanites aged 16 to 24 had a degree from a higher education institution, and over 42% had earned a bachelor’s degree or above.

Even those who do land jobs often face disappointment in the location and terms of their starting position. Location is crucial. To give some sense of scale, imagine graduating from a good College in the US and applying for jobs in a labour market that is the size of the US, Europe and Latin American combined. Where you land your first job really matters!

Since COVID, graduate expectations of starting salary and conditions have been drifting steadily down. With newly hired graduates in recent years commonly receiving no more than 6,295 yuan ($868) per month according to the recruitment agancy Zhapoin. Combined with considerable employment insecurity that hardly offers the chance to set up an independent household or marry. Many are abandoning the private sector altogether and crowding into civil service exams where the success rate is now 1 in 70.

But the focus on the labour market difficulties of urban, college-educated unemployed in China reflects more than just the numbers. Transnational class biases are at work. The people who write and read these stories worldwide are themselves college-educated. What this obscures is a deeper and in many ways more ominous trend at work in China’s labour market.

Two thirds of the young people entering the labour market in China right now below the age of 24 are not college-graduates, but have high school education or less. This reflects the fact that forty percent of Chinese young people do not make it into tertiary education. Indeed, a substantial minority barely finish high school and they make up the majority of people who enter the labour market “early”.

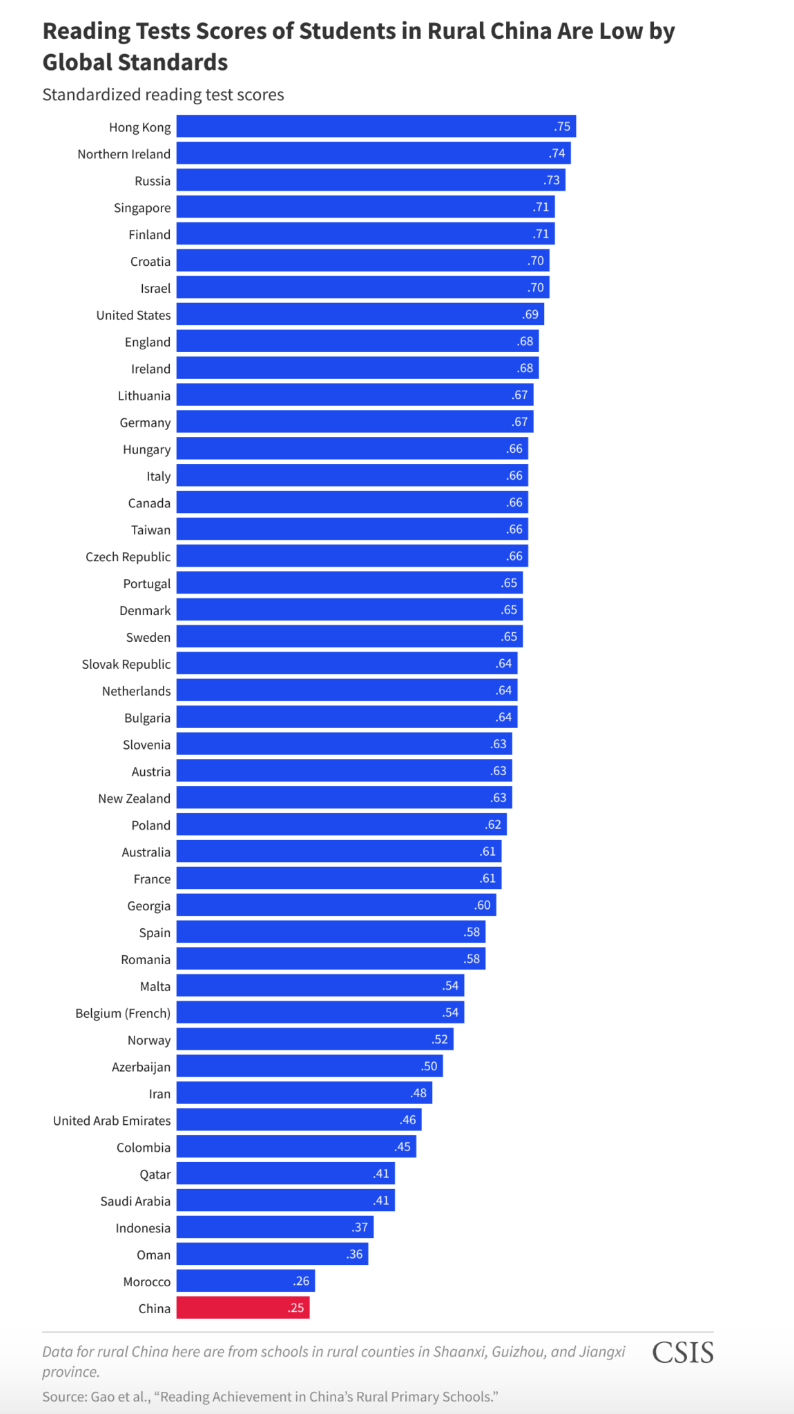

Whilst China’s skills machine has produced a spectacular surge in postgraduate training, particularly in STEM fields, in the rural areas of China, schools fail to teach even basic literacy skills. Admittedly, reading Chinese is hard, but in global rankings China’s rural schools come bottom, below even Latin America’s failing schools.

This educational failure in rural areas severely limits the labour market opportunities of tens of millions of young people. Where do they find employment?

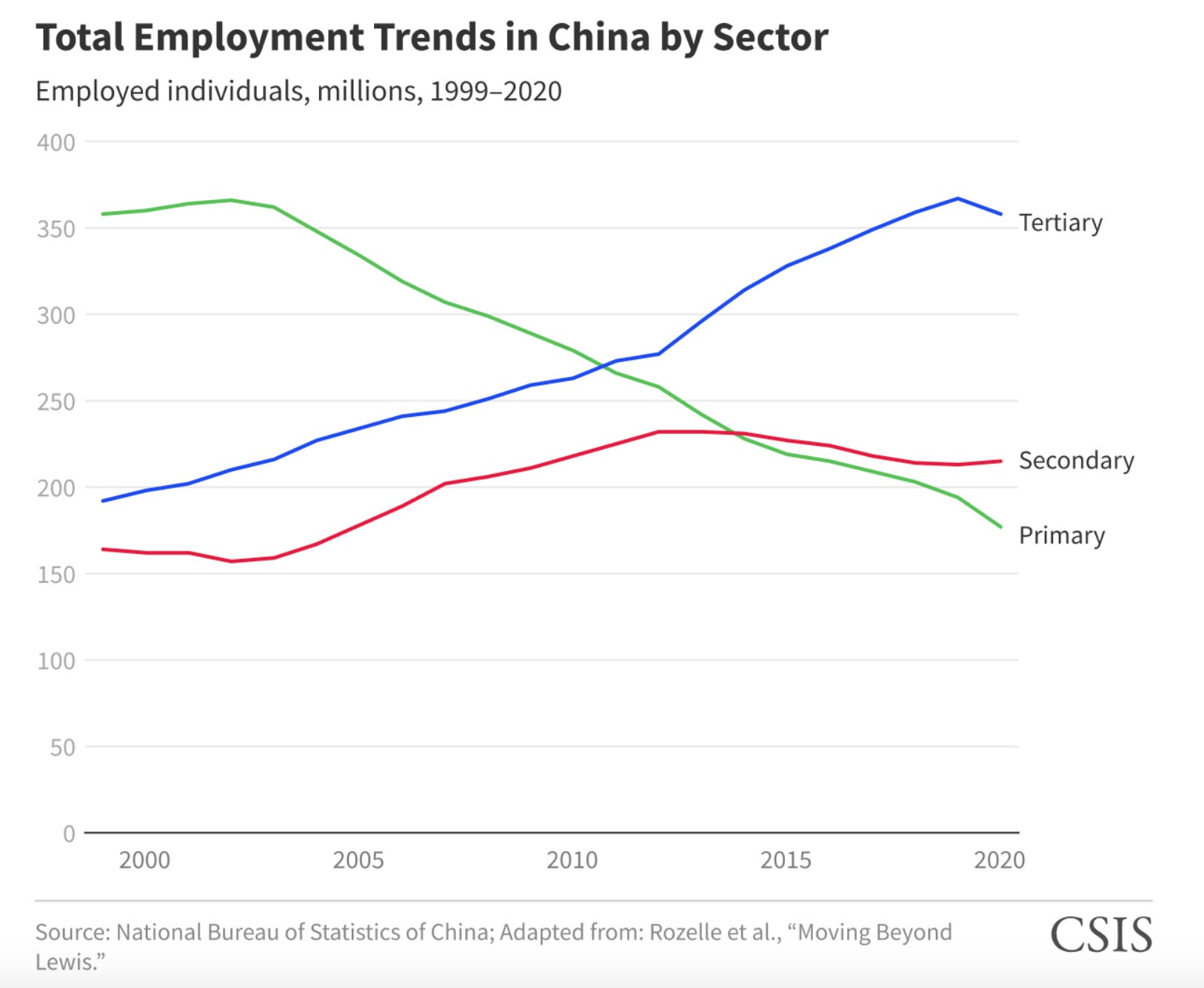

One might imagine that young Chinese with elementary schooling flood into jobs either on farms or in factories. But employment in industry and agriculture in China is declining, in both relative share and absolute size of employment.

Source: Big Data China CSIS

China’s industrial workforce is aging as young workers are shut out and stay away.

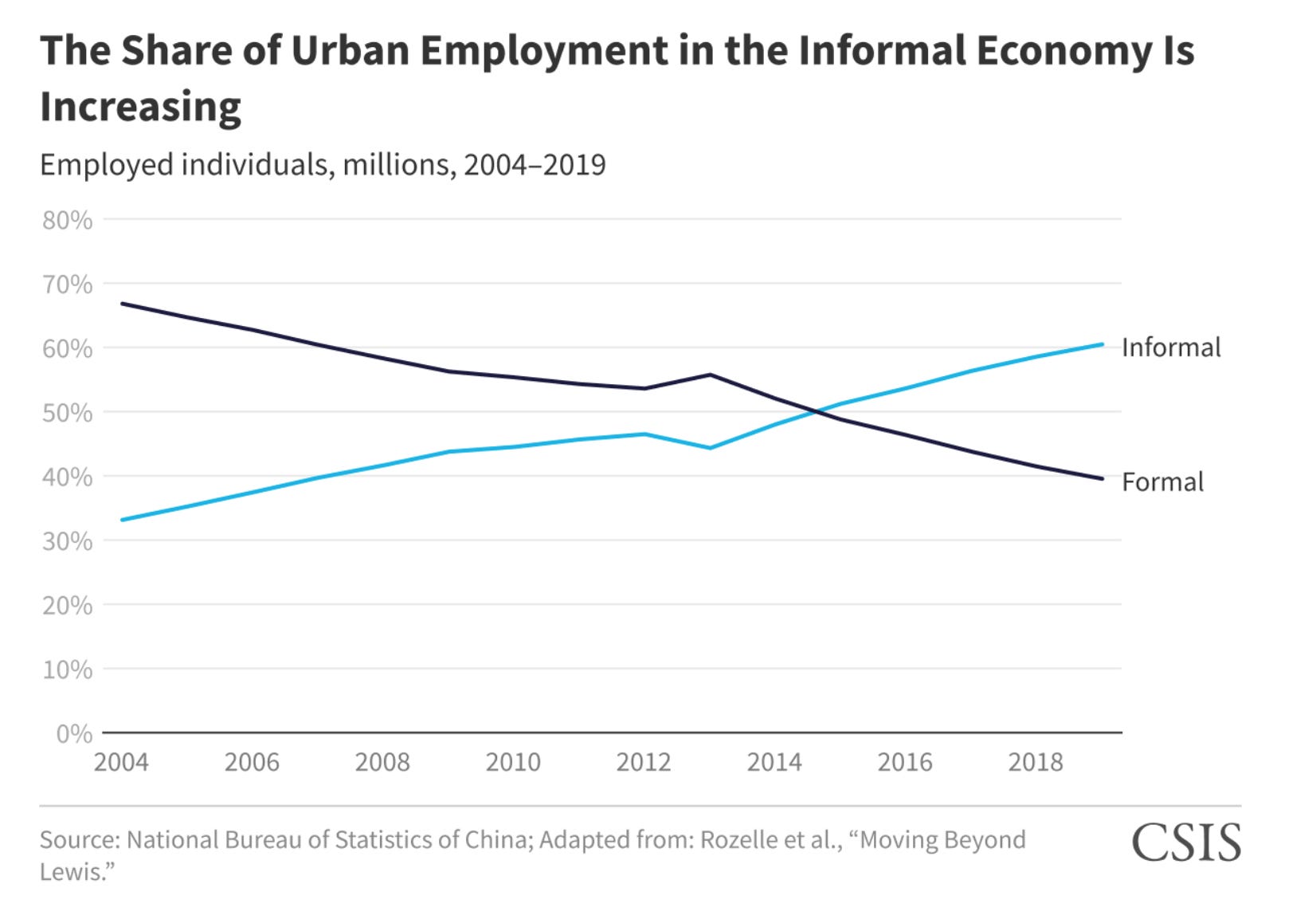

Instead, young workers at the bottom of China’s social pyramid are concentrated in low-wage, labour-intensive “flexible” or informal sectors. These include construction, often thought of as the “classic” employer of migrant workers. But, in fact, informal sector employment is not mainly in construction or industry. Two thirds is in labour-intensive services. All told, according to China’s own data confirmed by no lesser figure than Premier Li, China’s flexibly employed has reached more than 200 million, which constitutes roughly 14% of the total population and 27% of the entire working population. According to outside estimates the figure may be closer to 250 million. Rather than decreasing as China becomes richer, the share of informal sector employment is actually increasing.

These sectors were hard hit by COVID, by the general slowdown in consumer spending and not just construction but the entire real estate sector. They were also badly hit by the regulatory crackdown on the big platform businesses. According to data in Caixin analysed by Zhang Ziyu , a total of 13.2 million market entities — including corporations, partnerships, as well as self-employed people and households — deregistered in China in 2021, up nearly 30% year-on-year.

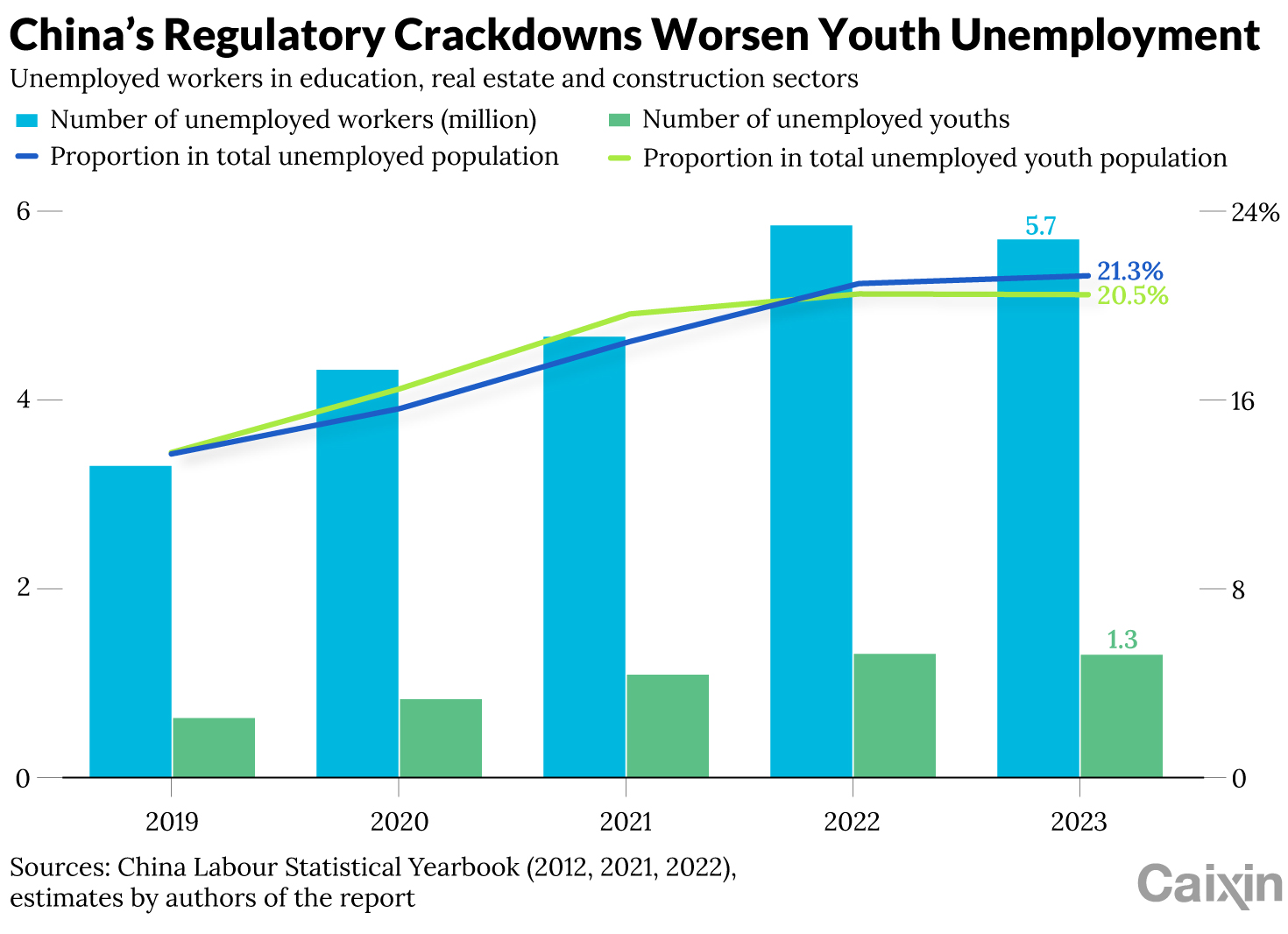

China’s crackdowns on overexpansion in for-profit tutoring, technology and real estate, has also hammered the labour market. According to analysis from Caixin, in 2023, 5.7 million people in the education, property and construction industries are expected to be jobless, a 73% surge from 2019. Of them, some 1.3 million would be young workers, more than double the number from four years ago.

But standing back from the sectoral and cyclical detail what appears to be going on is a fundamental shift in the operation of China’s growth engine. This at least is the diagnosis of Stanford’s Scott Rozelle and his coauthors Xia, Frisen, Vanderjack and Cohen in their 2020 paper: Moving Beyond Lewis: Employment and Wage Trends in China’s High- and Low-Skilled Industries and the Emergence of an Era of Polarization

As they describe their results:

One of the defining features of China’s economy over the two decades between 1995 and 2015 was the persistent rise of wages for workers and professionals in nearly every segment of the economy—with wage rates for labor-intensive jobs in manufacturing, construction, and the informal service sector rising the fastest. Recently, however, the economic environment in China has begun to change … Our findings indicate that China may have entered a new phase of economic development in the mid-2010s. According to the data, in recent years, wage growth has begun to polarize: Rising for professionals employed in formal skill-intensive industries; and falling for workers in the informal labor-intensive service sector. We attribute this increase in skill-intensive wages to an increase in demand for skill-intensive employment, due to the emergence of a large middle class in China, for whom the demand for high technology, finance, banking, health, and higher education industries is increasing while, at least in the recent short term, the supply of experienced, high-skilled professionals has not kept up. The employment/wage trend in the informal (low-wage) service sector, however, is following a different pattern. While there is a rising demand for services in China’s economy, the growth, due to a number of factors (e.g., large shares of GDP targeted by policymakers to investment; high rates of savings by consumers), is relatively slow. In contrast, due to a number of economic forces, including globalization and automation, the supply of labor into the service sector of the informal economy is being fueled by the flow of labor out of manufacturing and construction (two industries that that have experienced employment declines since 2013). These supply and demand trends, in turn, are leading to the fall in the growth rate of wages in the informal service sector.

China’s giant platform businesses are both drivers of these polarization trends and arenas in which they play out. It is tempting to call them a microcosm of these developments, but they are far too big to be called a microcosm.

One recent report by a Beijing-based venture capital firm credits China’s digital platforms with with employing altogether no less than 200 million workers out of a workforce of roughly 880 million. Another estimate by the China Information Economics Society puts platform-related employment at 240 million or 27 per cent of the working-age population in 2021. Either number means that far more people are employed directly and indirectly by China’s platforms than work in the entire US economy.

In the positions of most power in these giant networks sit the corporate elite. Clustered around them are the core corporate white collar workforce. Alibaba’s core workforce consists of roughly 230,000 people. Tencent employs roughly 100,000.

In the engine room of China’s online economy are 4 million programmers. Their labour maintains the 3.8 million websites that keep China’s online world humming.

Content for the platforms is created by no less than 5 million influencers each with over 10,000 followers. Their feverish activity stirs the giant streams of consumption which this year are flowing alarmingly slowly.

That spending is what employs the tens of millions who directly and indirectly depend on the platform economies.

In the lead come 16.5 million truck drivers. “70 per cent of China’s truck drivers receive at least half of their cargo volume from more than 2,500 truck-hailing platforms nationwide”.

7 million ride-hailing drivers depend on the platforms for gigs. More and more young Chinese are turning to taxi driving. “The number of new licences granted to drivers increased by 32.6 per cent in 2022, and the country has been adding new drivers this year at a daily rate that is five times higher than last year’s … some Chinese cities have stopped issuing operation permits to prevent an overflow of drivers.”

Then there are the delivery riders on mopeds – 5 million of them.

Whilst economic growth and wage growth for every part of the Chinese economy is slowing down, those at the top of the corporate hierarchy earn globally competitive salaries running into the hundreds of thousands of dollars and their salaries continue to increase above GDP trend. By contrast, as Rozelle et al’s data show, those in the informal sector see incomes dragging behind ever-diminishing gdp growth.

If we combine these various analyses of China’s labour market situation it would seem useful to distinguish at least three challenges facing Beijing.

The most obvious is simply the problem of growth: lower growth leads to a slackening of labour market demand and lower wage growth. It is commonly estimated that when China’s real GDP growth accelerates by 1 percentage point, it leads the surveyed urban youth jobless rate to drop 1.2 percentage points. That gives an idea of why the 5 percent growth target matters.

The next question is how to ensure that a growth revival does not compound the emerging structural imbalances in the Chinese economy and society. This requires expanding not industrial or construction activity but supporting the growth of higher-value and higher-skill service sector jobs, in sectors like education and health care. That in turn requires a model of growth driven by “consumer” spending rather than heavy investment. The most obvious way to do this would be why of an expansion of China’s thoroughly inadequate welfare state, across the full range of social services. This is the program of structural adjustment that Michael Pettis and many others inside China have long been arguing for.

Finally, Rozelle et al’s diagnosis points to the need not to back away from China’s expansion of higher education but to improve, broaden and deepen it. Compared to its peers, China does not suffer from an excess of skill in relation to its GDP level – as might be suggested by the headlines on graduate unemployment numbers – but rather the opposite. China needs more skills.

The good news is that China has open to it a fairly clear win-win path: great investment, not in physical but in human capital. The question is whether the regime realizes the scale of this opportunity and is willing to take the plunge.

Premier Li Qiang is making overtures to the Big Tech firms. There are a range of subsidies available to stimulate employment of young workers. Beijing is also subsidizing targeted vocational programs, and amending relevant law to elevate the status of vocational education. But in China today there is a sense that the direction has to come from the very top and Xi’s rhetoric has been both tough and largely beside the point. He has called on graduates to “eat bitterness”. His economic policy priorities are mainly focused on national security and strategic competition with the United States not the service sector, where modern Chinese actually work.

But as out of touch as Xi seems, It would be a mistake to over-personalize this impasse. Or indeed, to see it as a specifically Chinese problem. Only a handful of relatively small economies – the likes of South Korea and Ireland – have successfully navigated the kind of structural impasse, which Rozelle et al’s work points to. Nor are the problems confined to countries we think of as caught in the “middle-income trap” – Mexico, for instance. The logic of polarization that is beginning to play out in China, is powerfully at work in the UK, Germany and the United States. And we can hardly say that any of them has come up with a good answer. Instead, perversely, leadership on both sides – in both the American-led West and in China – are locked in on a range of industrial policy programs that may (or may not) matter for grand strategic competition, and may shape the energy transition and the high-tech frontier of the future, but have an indirect bearing on the sectors in which the vast majority of their citizens earn their livings in the 21st century. It is not just in politics but in economic policy too that the new era of polycrisis – climate, geopolitics & worries “blue-collar” work – seems to be taking us all back to the future.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you will receive the full Top Links emails several times per week.