We are entering the second serious phase of inflation politics.

The first was the decision in 2022 to raise rates sharply to counter a mounting clamor about delay and misdiagnosis. Central banks pushed through this uniquely comprehensive worldwide tightening despite warnings that they would unleash financial chaos, and in the face of huge losses inflicted on bond markets. They voided the implicit guarantee that was known as the “Fed put”. In so doing they fundamentally reweighted the derisking bargain between central banks and financial markets and took a more or less calculated gamble on the stability of the financial system.

Subscribed

In 2023, inflation is coming down, but not fast enough for those who worry about inflation. So, as is clear from the ECB’s annual jamboree in Sintra Portugal, a new debate has started about the need for perseverance in the face of persistent inflation. Analysts and central bankers are already looking forward to later this year and next. They are staking out their positions on what central banks should be willing to do once the easy part is done and they are in the “last mile”, struggling to bring inflation down from 4 to 2 percent.

This may seem premature, but it makes sense to telegraph positions far in advance in the hope of establishing credibility and thus easing the process. The rationales vary. The BIS is advocating for a combined arms approach, calling on the fiscal authorities to do their bit. The IMF’s Gita Gopinath highlighted the risks to the most indebted countries if interest rates remain high for longer. But before we get to the trade-offs of the “final mile”, what actually is the base rationale for action? A particularly searching answer was offered in mid-June by ECB Executive Board member Isabel Schnabel in a talk she gave in the financial center of Luxembourg.

***

When you think about central bankers and inflation, you might think of a “heroic” figure like the Paul Volcker of lore, “sacrificing his popularity and millions of jobs worldwide to stop a dangerous inflationary surge threatening to undermine the fabric of civilization” – a super hero arriving in the knick of time to save the status quo with a monetary policy hammer.

You might imagine a central banker under a Tinbergen policy assignment, calmly focusing on price stability whilst other agencies with other instruments maximize employment and growth.

Or you might envision the central banker as the technocratic tinkerer carefully picking a point on a Phillips curve, fine-tuning the balance of unemployment and inflation.

What these images have in common is that they portray central bankers as powerful actors who know what they are doing. Who know why it matters and why they are doing it. That at least is the retrospective narrative.

What about today?

Reading Isabel Schnabel’s speech you get a very different impression of the mood and logic of central-bank decision-making. Her characteristically lucid assessment of the limits of central bank knowledge when faced with the problem of stubborn inflation, smacks less of heroism or technocracy than nihilism. And yet this does not lead Schnabel to put in question the central bank and its instrument as a means of inflation control, or even their ability to specify “optimal policy”. It leads her, instead, to double down. In Schnabel’s logic, admitted ignorance, failures of foresight and profound uncertainty become an argument for forceful counter-inflationary action.

***

Schnabel’s point-by-point exposé of the limits of central bank knowledge when it comes to the basic question of how to fight inflation by raising interest rates is remarkably comprehensive.

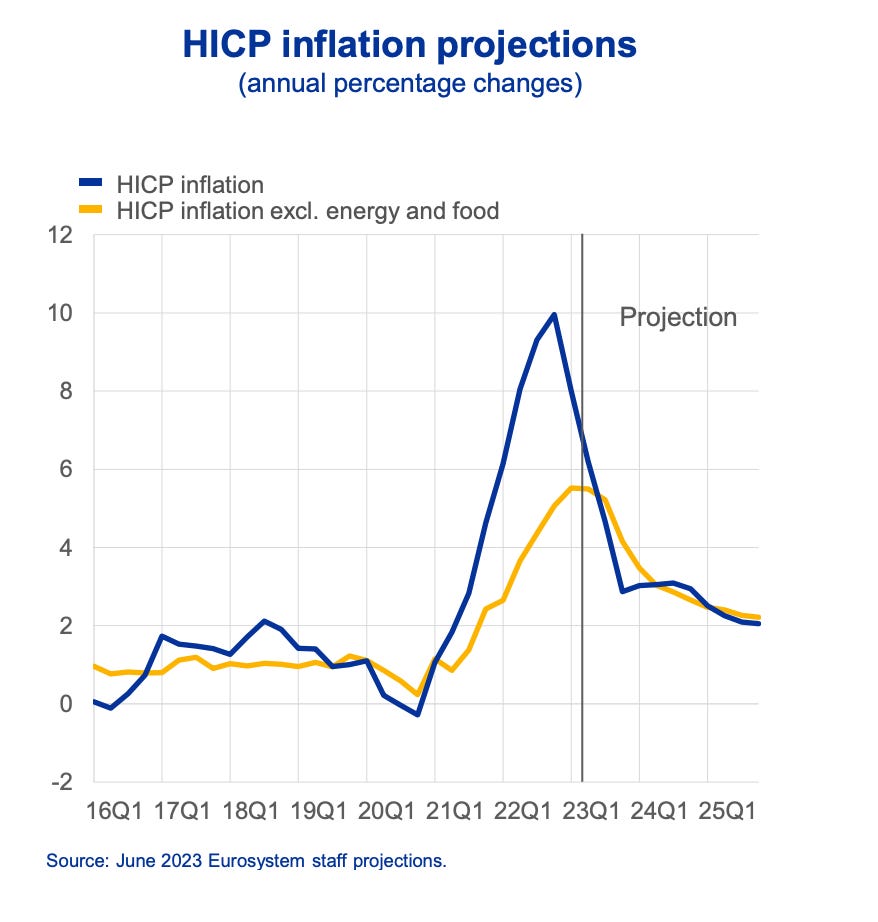

As Schnabel frankly admits, the ECB like other central banks around the world, still doesn’t know how serious the destabilization threatened by the current round of price increases actually is. Their own forecasts suggest inflation will be down around 3 percent by the end of 2023 and fall further thereafter.

There hasn’t been a wage-price spiral. You can fret about it and paint dark clouds on the horizon about the unmooring of inflation expectations. But the threat is hypothetical and is derived by projecting experiences of the 1970s into the current moment without evaluation of the relevance of those historical experiences to the present day. A spiral would imply wages overshooting prices to produce an upward momentum. There seems zero probability of that. But even a dampened, “decaying” series of secondary reactions from prices to wages and back to prices depends, as Schnabel frankly states, on whether firms fight to maintain their inflated profit margins, or simply absorb the relatively modest wage increases.

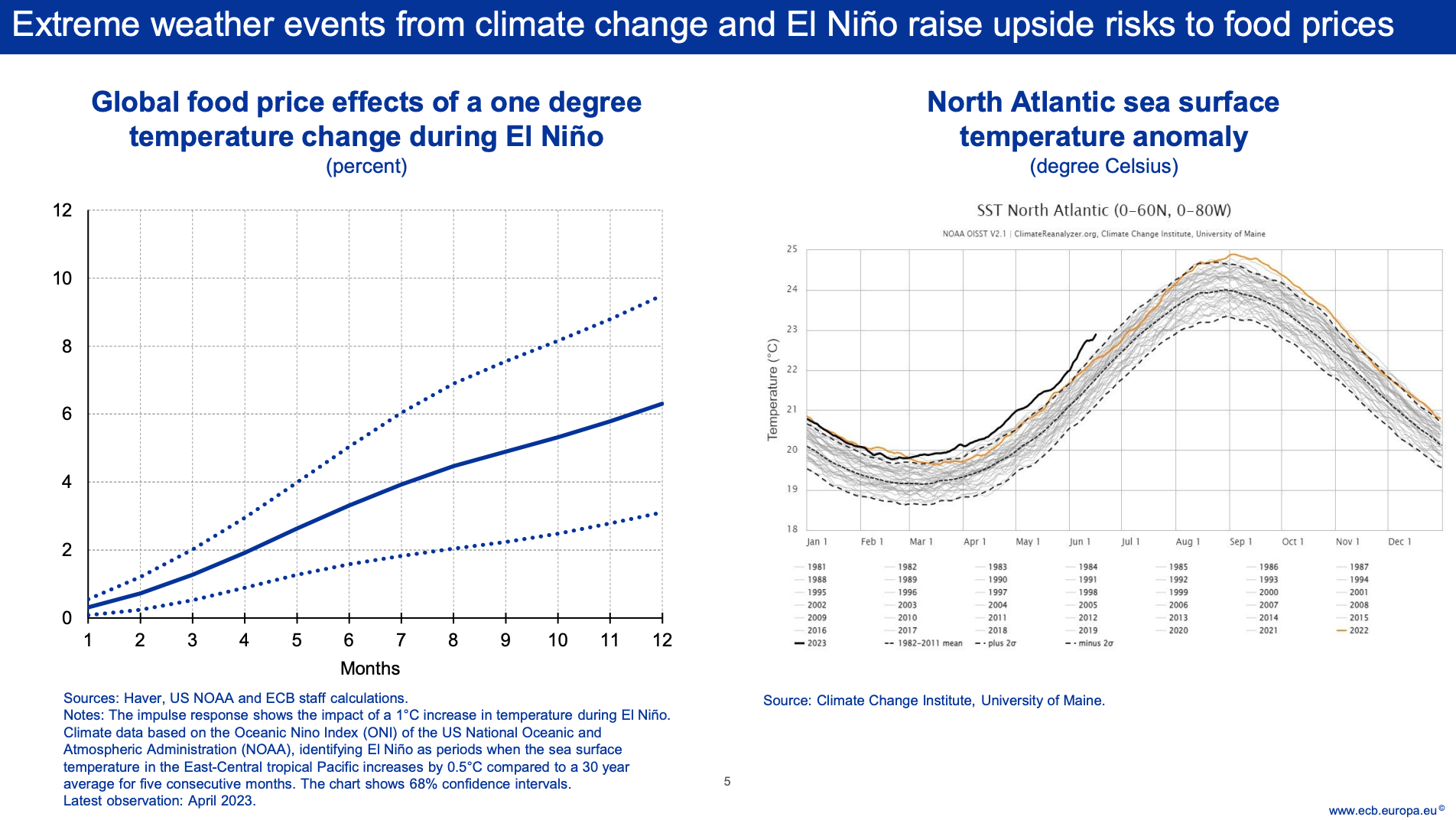

As Schnabel also lays out at some length, the evidence available to the central banks clearly suggests that current and future inflation risks are largely due to factors beyond the monetary system. Schnabel frankly acknowledges the footprint of the polycrisis across the price system. In her talk she invokes El Nino’s impact on food prices.

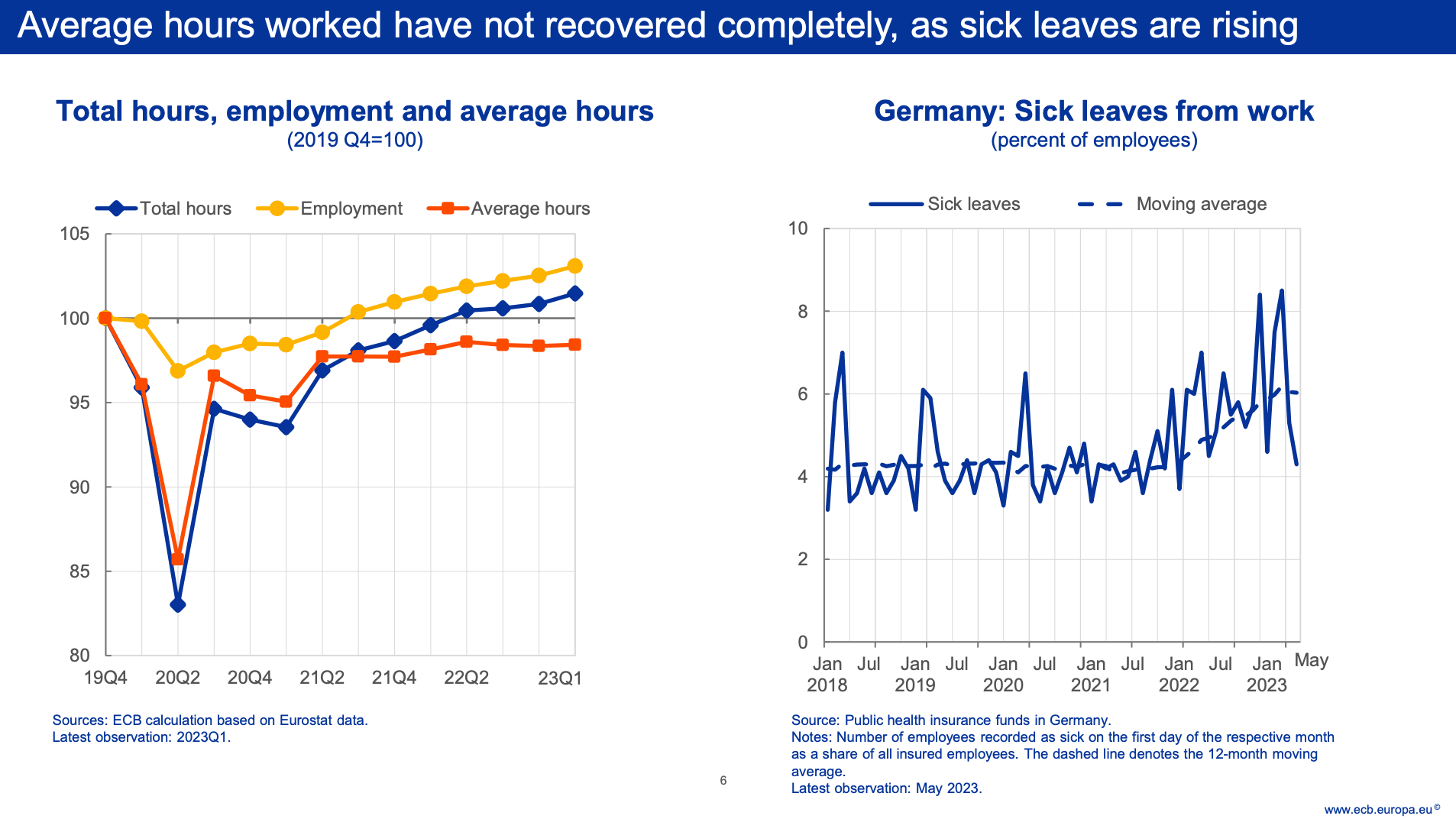

She also produces fascinating data from the German insurance system of the long-run impact of COVID on the rate of sickness in the labour force.

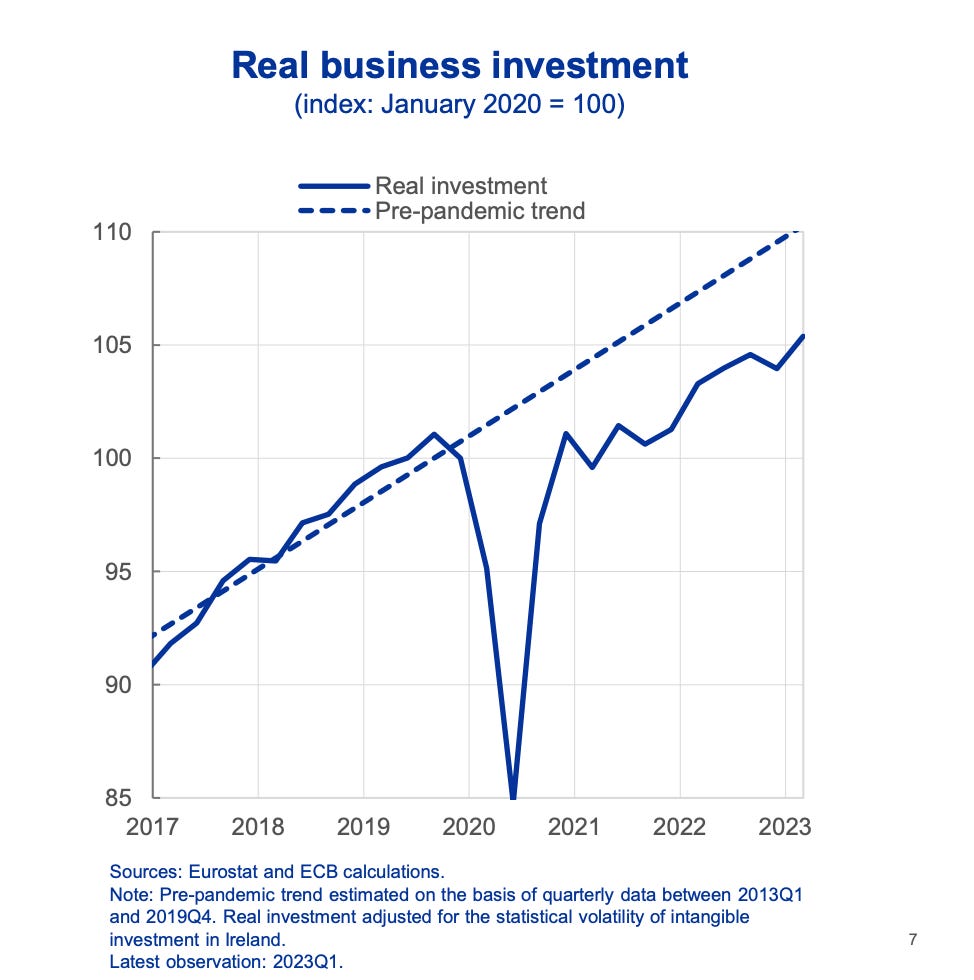

The pandemic delivered a shock to investment from which the European economy has not yet recovered. You would think that this would put a premium on running the economy hot and boosting growth. But as a European central banker that isn’t Schnabel’s brief. Her focus is on price stability and from that point of view less investment means a tighter corridor for growth, more upward pressure on prices, and a greater need for higher interest rates. A vicious circle.

The fact that the supply-side matters in these diverse ways may help to explain why the central banks didn’t accurately forecast the current inflation. You might expect a confident central banker to say that they were busily engaged in new research to correct their errors. And Schnabel certainly cites plenty of research, but only to show that rather than correcting their errors, central bankers i.e. Schnabel herself and her colleagues, are prone to repeating them. This in turn means that to do better in future, they should bracket their own assessments of the situation and any tendency they might have to be over-optimistic about prices. The research they should learn from is the research that tells them that they are bad at learning. As much as it is important to check your biases, one has to ask, is it really a good for decision-makers of any kind to be self-doubting to this degree?

But Schnabel goes on. Not only are central bankers bad forecasters, they may not be very convincing policy-makers either. At least this is what financial markets appear to believe. According to recent surveys, a majority of investors doubt that the current crop of central bankers has Paul Volcker’s mettle and will actually go the final mile. The vast majority of respondents expect the central bank to settle somewhere between 2 and 4 percent. And this, it should be noted, has not led to panic. Nor should that be surprising given that two or three years ago, you would have had your hand bitten off if you offered the markets a scenario in which European (and Japanese) inflation settled comfortably above 2 percent.

Schnabel notes almost in passing that the ECB cannot count on elected politicians to make major adjustments to fiscal policy to fight inflation either. This makes the central bankers feel as though the burden is entirely on their shoulders. You might also wonder, whether if the markets don’t care and the politicians don’t care, a rate of inflation that is already declining really merits all the fuss – beyond the need to protect those most vulnerable against the surge in the cost of living. But that is not a thought that Schnabel entertains. She insists that something must be done. But what?

***

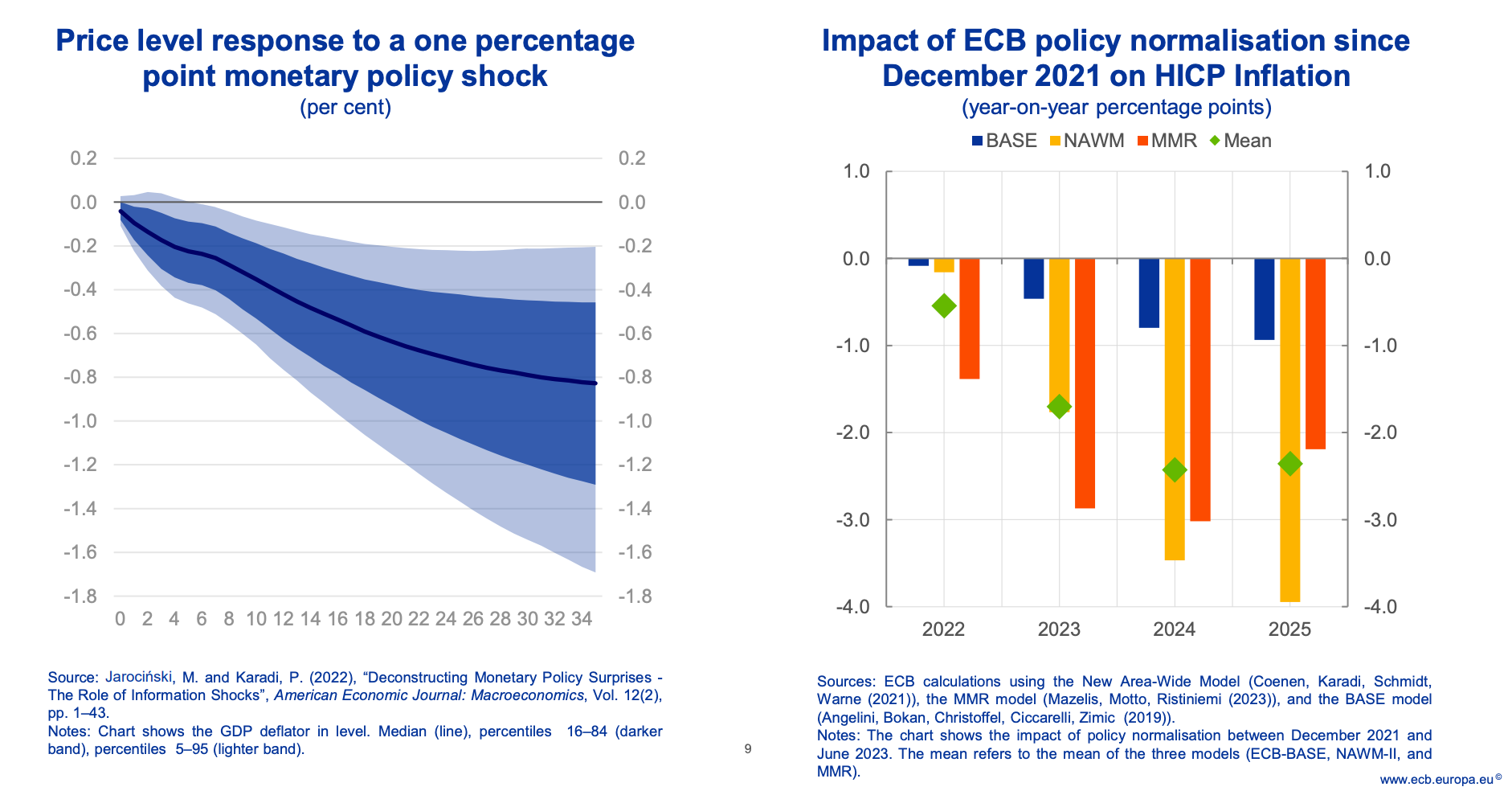

As Schnabel lays out unflinchingly, if the ECB does decide to act, it has little idea to what level it should raise interest rates because different economic models give wildly different answers on the question of how powerful interest rates are in bringing inflation down. According to Schnabel:

the estimated impact on inflation in 2025 of the ECB’s policy actions taken since December 2021 ranges from 0.9 to 3.9 percentage points across three of the ECB’s main macroeconomic models

Even the same model can yield wildly different estimates of the likely effect. As Schnabel reports:

For example, according to a benchmark model from the academic literature, a one percentage point increase in the short-term interest rate could dampen inflation after one year by as little as 0.1 percentage point, or by as much as 0.8 percentage points

As Schnabel acknowledges, there have been a variety of structural changes in the European economy that make it less likely that interest rates will have any major effect on the economy – the structural shift to services since the 1970s, accumulated cash balances and the strength of the labour market. As Schnabel admits the most important transmission mechanism for policy is the labour market and so far robust demand has meant that higher rates have not slowed it down appreciably. Though with the news of a recession building in Germany, that may be about to change.

In any case, what matters most for the effectiveness of policy is not so much the interest rate itself, as the expectations of businesses and consumers with regard to future inflation. Expectations about the future mediate how economic agents respond to any signal, whether it be prices or interest rates. The problem is that in technical terms, expectations are hard to track.

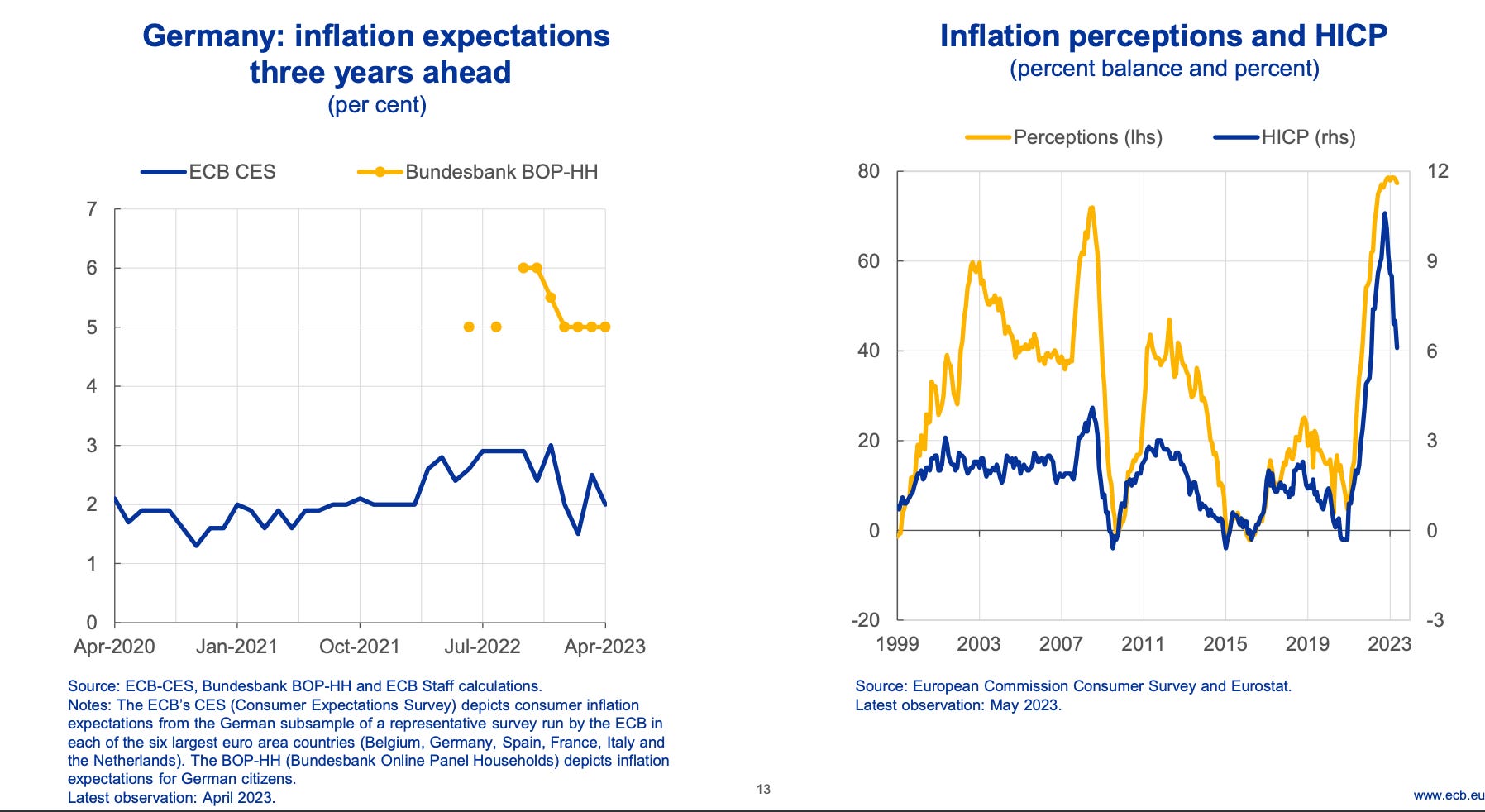

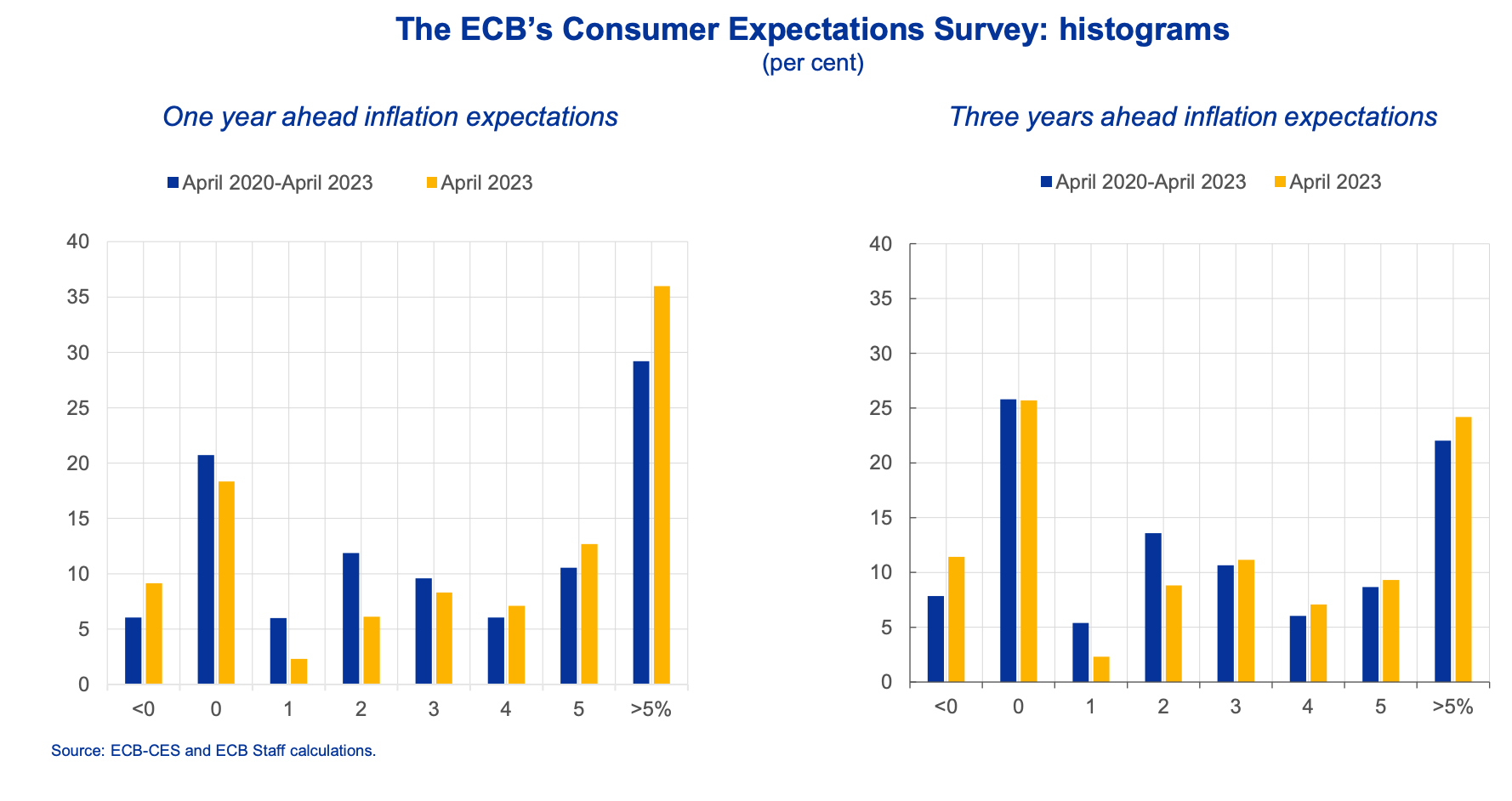

Different surveys by different agencies yield hugely different results as to the state of expectations in the eurozone. The Bundesbank finds much higher rates of expected inflation in its surveys than does the ECB.

If you look into the data and unpick the average numbers, many consumers and businesses appear to pay no attention to inflation at all.

Counter to all experience, substantial minorities expect prices to remain unchanged for the foreseeable future. Meanwhile, many of those that do pay attention tend to have totally unrealistic ideas about the actual level of inflation. One survey that has made headlines in Germany recently shows respondents declaring inflation to be running at over 16 percent, well-nigh three times the level reported by official statistics for the Eurozone.

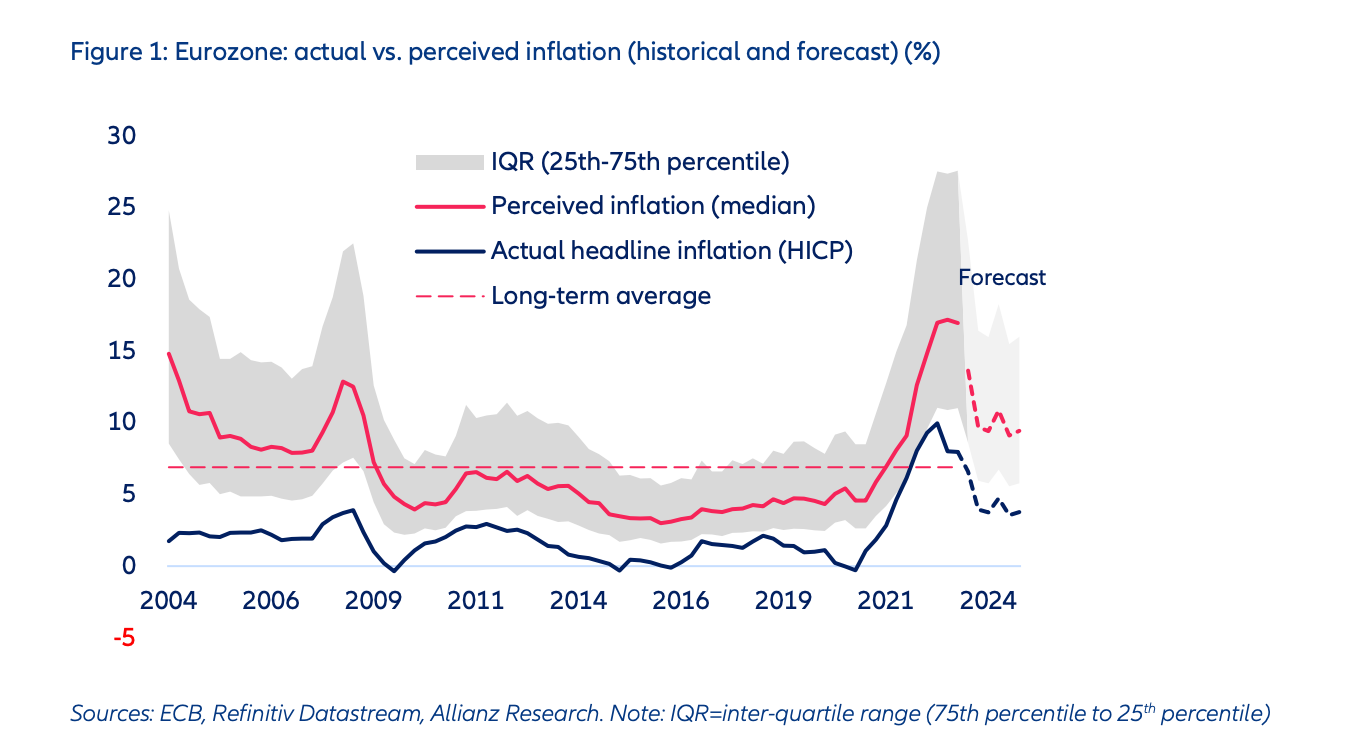

Source: Allianz-Trade

This is bamboozling, but if you bear in mind that the best monetary economists in the world cannot agree on a model that yields reasonably consistent predictions about the impact of interest rates on prices, ordinary consumers and businesses may be forgiven for being confused. It is a giant hall of mirrors where, as Robert Armstrong recently pointed out in the FT, we don’t know whether the array of short-term and long-term interest rates summarized by the yield curve is a causal factor in slowing down or speeding up the economy, or predictive because the rates that emerge from buying and selling bonds summarize a vast array of market forecasts, or whether as a widely watched indicator, the curve functions like a self-fulfilling prophecy inducing a deceleration or an acceleration of economic activity because of the anticipation of actions conditioned on it.

***

So what emerges from this fog of uncertainty and negatives? A case for restraint? An argument for using other policy instruments to manage prices? No. Despite her sobering admission of fundamental ignorance about practically every important parameter of the problem, the conclusion that Schnabel arrives at is that the “optimal policy” for the ECB – an audacious characterization if there ever was one – is to adopt a more aggressive tightening stance and to hold it for as long as core inflation is not decisively turned downwards. Why? Because, if they are wrong it is apparently relatively easy to unwind the mistake, whereas if they are slow to act, it will take longer to redress the mistake and the ultimate outcome will be worse. One wants to object that this neglects the need to consider the trade-offs. What will the price be in terms of unemployment and canceled investment? What about the mounting evidence that the European economy is beginning to turn into a recession? Furthermore, how, in light of the underlying uncertainty of the models, can one reasonably talk about ”optimality”?

But Schnabel sticks to her guns:

A monetary policy stance that errs on the side of determination “insures” against costly policy mistakes caused by inflation being more persistent than expected. Such an approach is called “robust”.[35]

The ECB should keep raising rates and in doing so it should be guided not by unreliable forecasts of the future, the future in which its rates will actually affect the economy – or not – but by one key piece of immediate data – the core inflation rate. It is not, after all, the ECB’s mandate to strike a balance between objectives – as in a dual mandate – but to secure just one – price stability. Of course, the ECB is concerned about obtaining its goal as efficiently as possible – at the minimum cost to the economy – but to weigh the question too publicly is dangerous in that it reinforces doubts in the market that the central bank is willing to act.

Thus the combination of operating in a fog whilst needing to maintain the appearance of credible commitment to a single mandate becomes a recipe for one-sided tightening regardless of the cost: Ignorance becomes a justification for action.

But what kind of logic is this for decision-making within one of the most powerful agencies of government? Rather than either the heroic political actor or the calculating technocrat, one gets the impression of an insecure and half-blind “night-watchman”, thrashing around in the hope that this will frighten off whatever threat may or may not be out there. Knowing how limited their vision is and how uncertain the means at their disposal, the central bankers act with whatever tools they have to hand. At the very least they avoid any further criticism for having tried to be too clever, having tried to weigh or assess the actual threat.

Any fuller effort at realism – in the sense of trying to balance the full range of means to carefully weighed ends – is simply too demanding and too risky. Rather than encouraging a search for imaginative and cost-effective policy alternatives, acknowledging a polycrisis serves to justify conservatism.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you will receive the full Top Links emails several times per week