Now you see it. Now you don’t. Thinking about the Biden administration’s new industrial policy I am trying to square two realities in my head.

On the one hand the infrastructure, CHIPs and Inflation Reduction Acts seem to be translating into a real investment and construction boom.

All told, according to Bloomberg’s reckoning:

Laws Congress approved last year (2022) together offer about $420 billion in funding to incentivize the domestic production of chips and clean-energy technologies. Add the infrastructure bill Biden signed in 2021, which requires that all iron, steel and other construction materials used in public-works projects be made in the US, and you’ve got about $2 trillion in federal spending over 10 years.

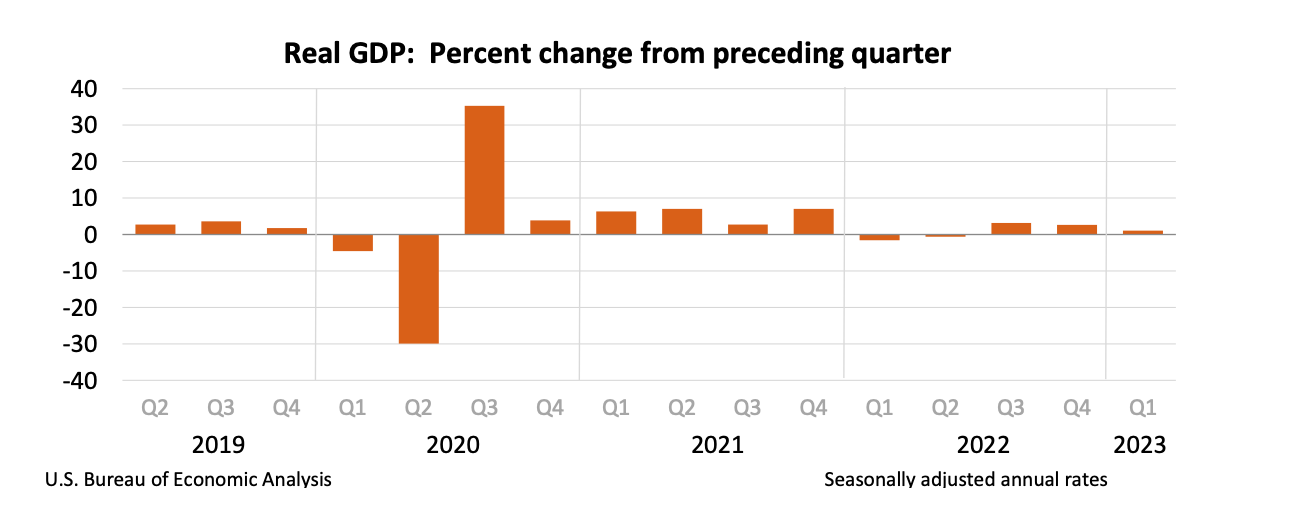

On the other hand, the lack luster figures out of America’s Bureau of Economic Analysis show overall growth slowing fast. Falling investment is retarding America’s growth, not accelerating it. Nor should that be a surprise. It is one of the intended effects of jacking up interest rates to fight inflation.

Source: BEA

Enthusiasts for the IRA cite estimates from Goldman Sachs suggesting that the eventual total of spending unleashed by that piece of legislation alone may run to as much as 3 trillion dollars or more. This conjures up images of an

American

economy and American society transformed, with the IRA delivering the green equivalent of the shale revolution.

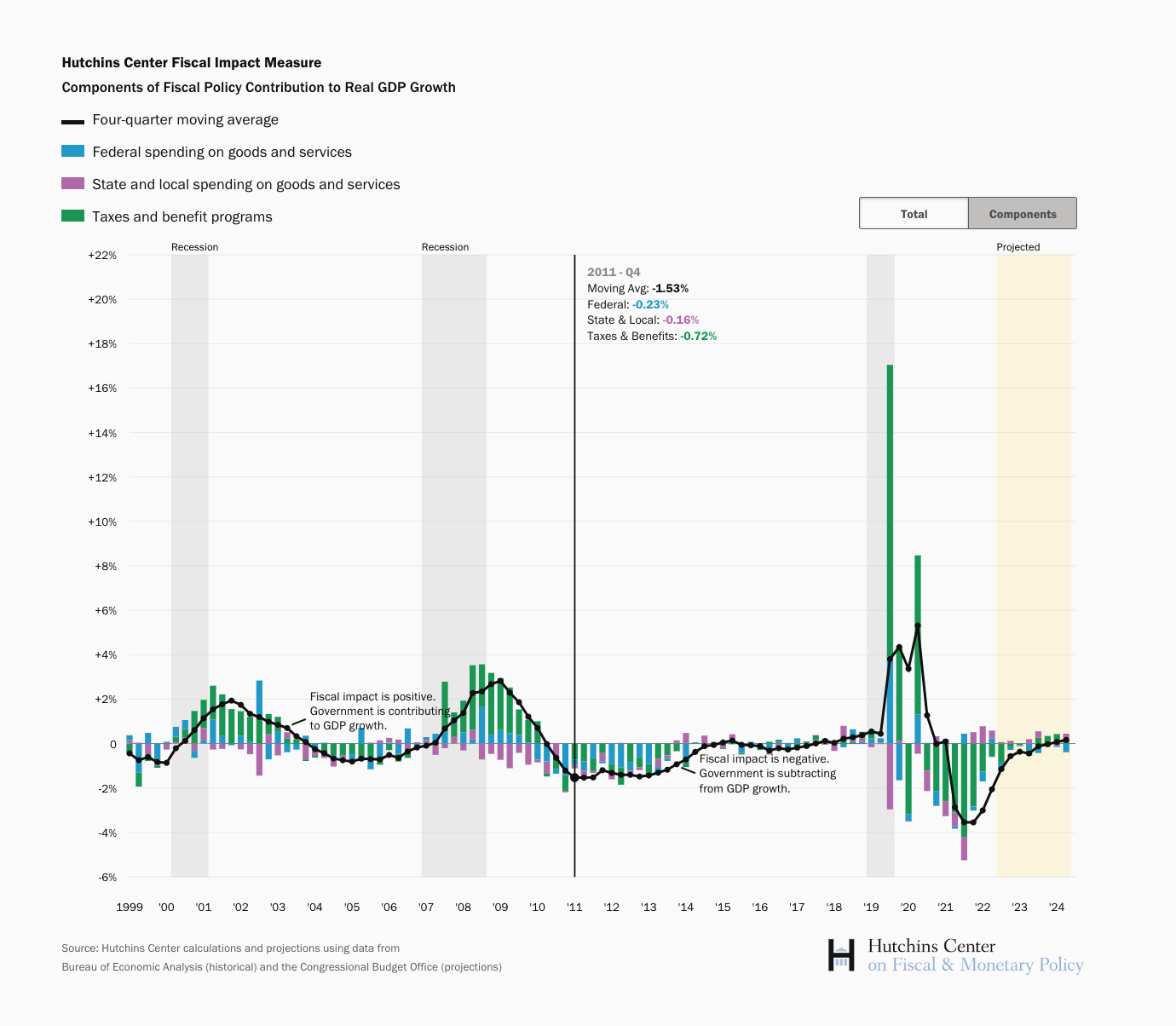

On the other hand we have the estimates from Eli Asdourian, Nasiha Salwati, Louise Sheiner, and Lorae Stojanovic at the Hutchins Center at the Brookings institution which show that since the drama of 2020 and 2021, fiscal policy has moved towards a neutral setting.

In 2020 and Q1 2021 the stimulus packages voted by Congress delivered a huge and economically appropriate stimulus. Then, already in Q2 2021, many months ahead of the Fed’s monetary tightening, the fiscal impact turned negative. By Q2 2022, as the IRA finally passed through Congress and the inflation scare built to its height, fiscal policy was exercising a drag on the US economy to the tune of 4.8 percent. This was counter-cyclically appropriate. And, since then, the pressure has eased. But compared to the COVID-era stimulus programs of 2020 and 2021, the IRA barely seems to register.

This is consistent with macroeconomic modeling of the IRA, which consistently show its effect to be tiny. What then are we to make of this cognitive dissonance? A bright new dawn of industrial policy on the one hand, macroeconomic normality on the other?

This question might be seen as a quantitative extension of the skeptical questions asked by observers like Daniela Gabor about the political economy of the Biden administration’s new industrial policy.

Whilst Daniela Gabor is asking is whether the IRA opens the door to a new political economy, or whether it is merely the old wine of financialized de-risking in new bottles, what I’m trying to figure out is how big the intervention actually is. Even allowing for the possibility that the political economy is new, does the Biden administration’s “new industrial policy” really have the heft to make a transformative difference?

***

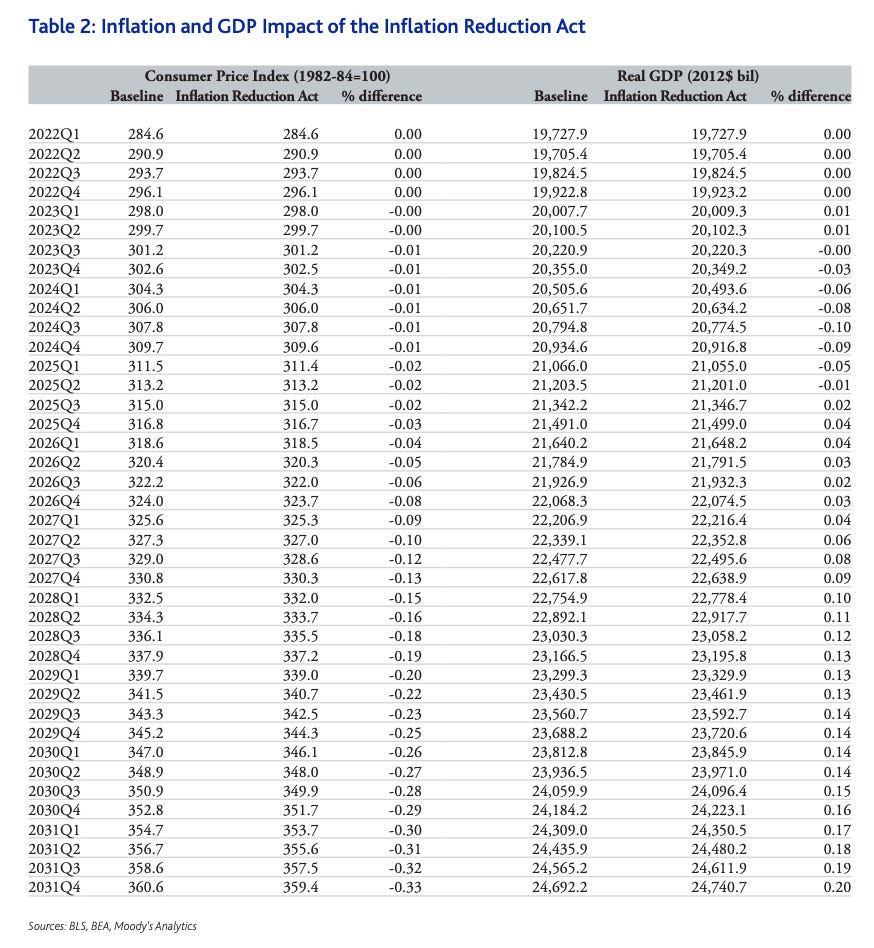

The first macroeconomic evaluation of the IRA I’ve been able to find, that by Mark Zandi’s team at Moody’s Analytics from August 2022, arrived at very modest totals for both the GDP and inflation impact.

The total impact on growth and inflation never amounts to more than a fraction of one percent.

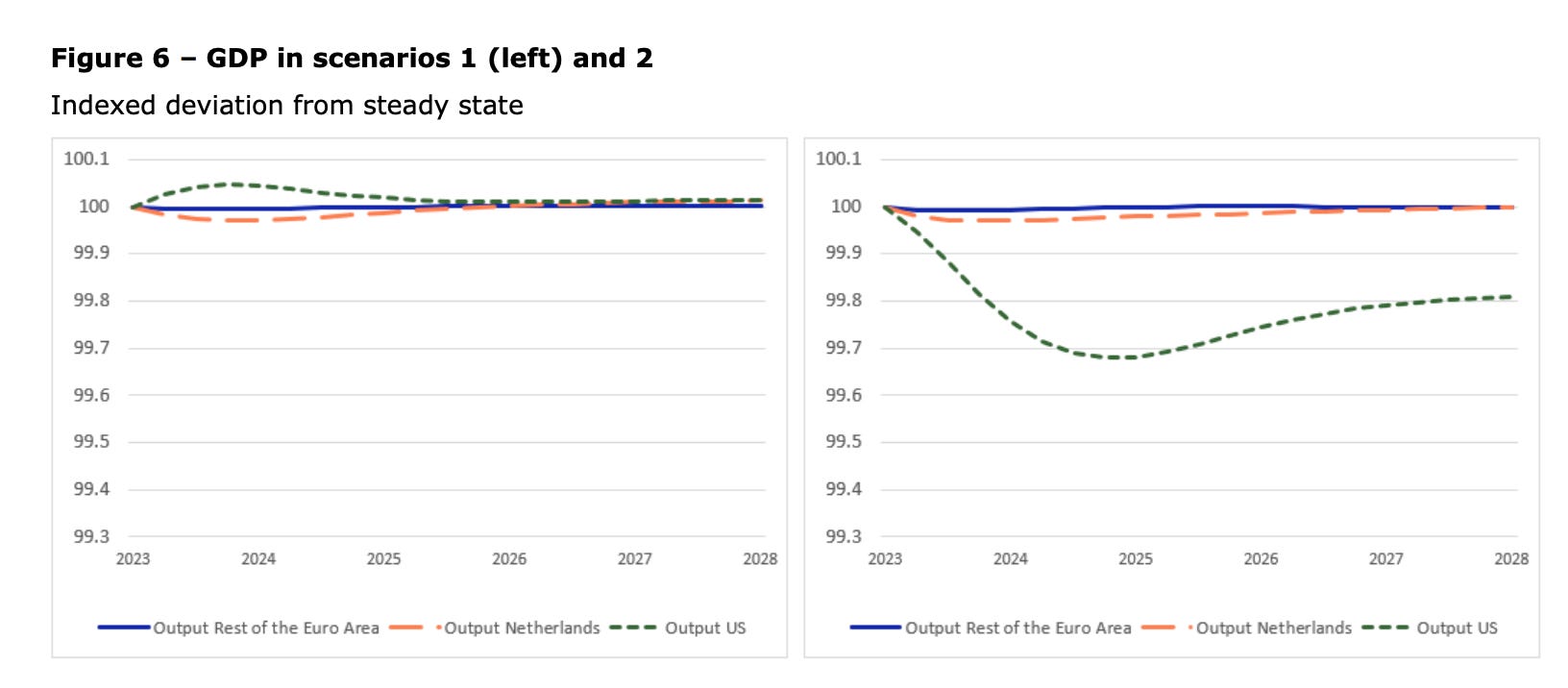

These data were calculated back in August 2022. If you know of more recent evaluations please let me know. When economists at the Dutch National Bank attempted their own macroeconomic analysis of the IRA, published in May of this year, they found nothing to reference other than the Moody’s exercise. The DNB’s results confirm Zandi et al’s conclusions. Using conventional models, the macro impact of the IRA looks negligible.

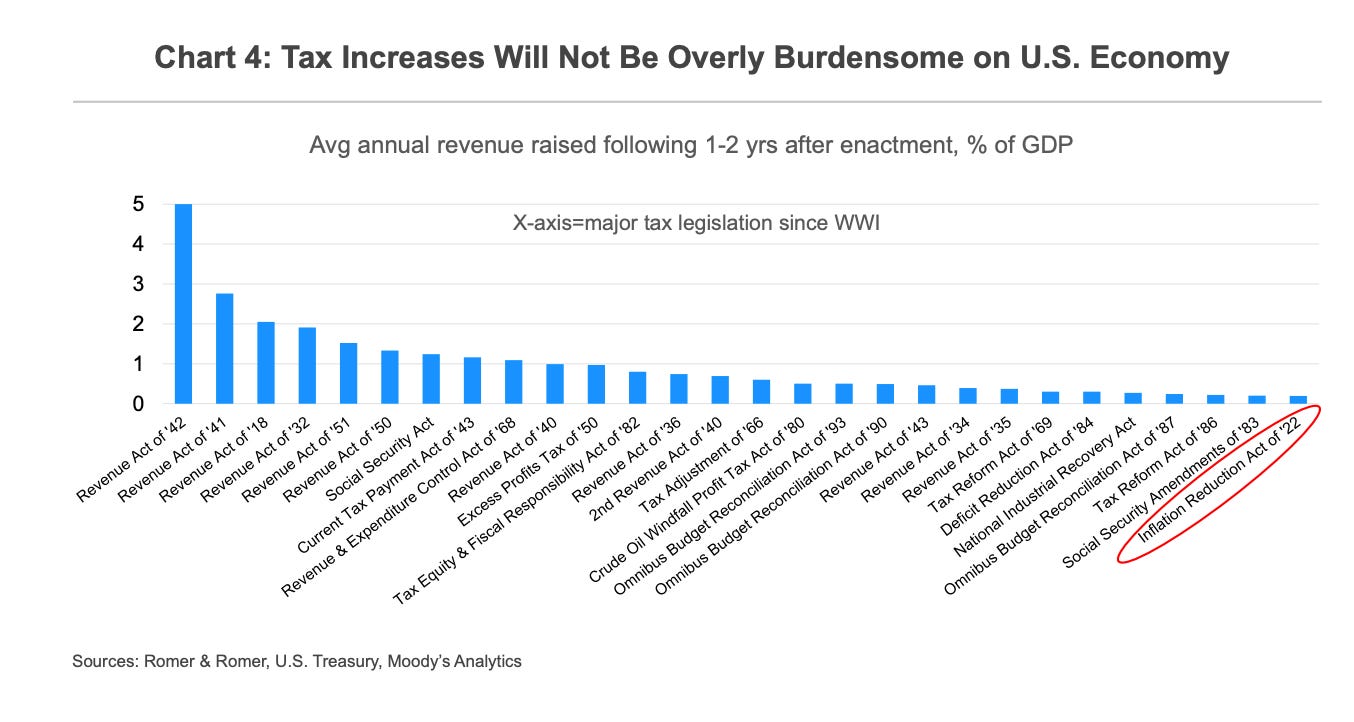

The DNB’s Scenario 2 involves an increase in corporate taxation to pay for the IRA tax breaks. But as Moody’s points out, in historic terms the IRA ranks low amongst tax measures reeform measures.

I have yet to see a macroeconomic evaluation of the entire $ 2 trillion “new industrial policy” trifecta. That is clearly substantially larger than the IRA alone, but, divided over a decade, it amounts to an annual injection of less than one percent of GDP, not allowing for financing costs.

***

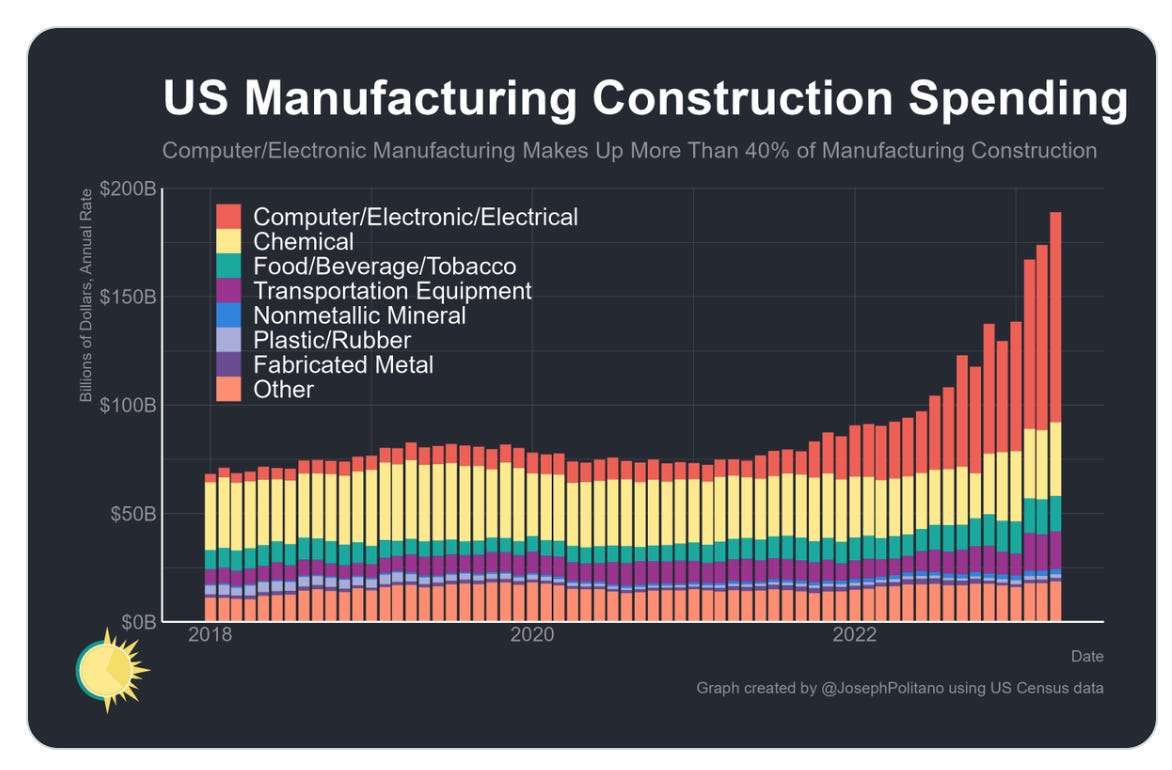

In any case, enthusiasts for the new industrial policy will likely argue that such macroeconomic evaluations miss the point. The aim of the IRA and other legislation passed since 2021 is not to deliver a giant green stimulus but to act as a targeted incentive to investment in the energy transition and the new Cold War tech-race with China. And on those fronts, it seems, the IRA, Chips and the infrastructure bills are delivering. On twitter a dramatic graph of US manufacturing construction has beeen making the rounds.

Source: Joey Politano

This is, no doubt, a dramatic picture. There has been a huge surge in construction in the exorbitantly capital-heavy microchip sector. This has ben supported by a smaller step-up in investment in transportation equipment, presumably in the battery and EV segment.

These numbers are consistent with project-level data compiled by Amanda Chu at the FT. As of April 2023 this came to $139 billion in announced projects for semiconductors and $65 billion for clean energy.

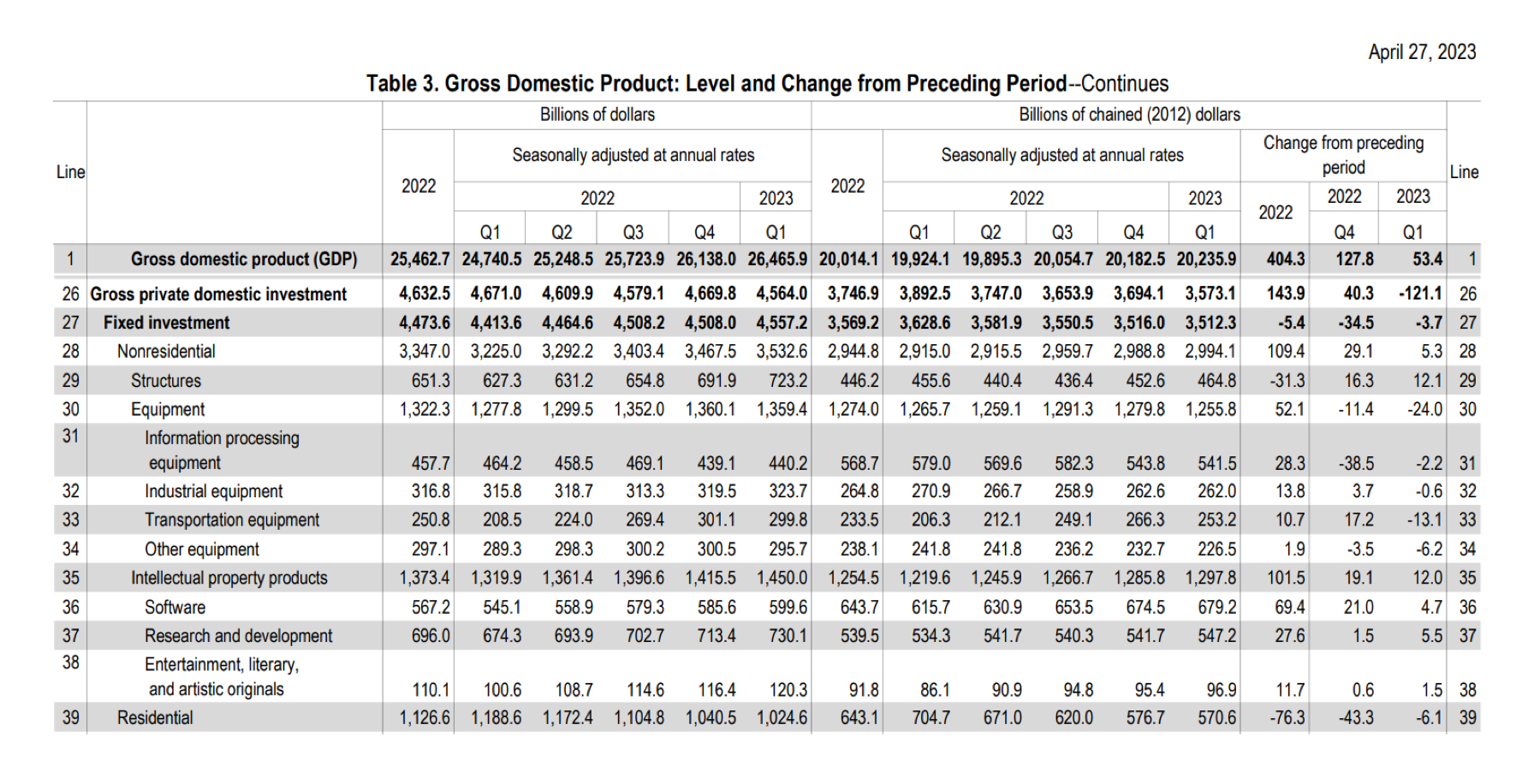

But how does this intensified investment in the heavily subsidized sectors relate to broader investment spending in the US economy at large? If one looks into the national accounts, as laid out by the Bureau of Economic Analysis, it is easy to see how an exciting story about factory construction in two key sectors can be reconciled with with a lack luster story about investment in the economy at large.

The construction surge in manufacturing which is causing so much excitement, amounts to an increase of $100-120 billion per annum, raising the current annualized rate to $200 billion. Investment in structures as a whole across the entire US economy is more than three times that. According to the BEA, investment in structures increased between 2022 and the first quarter of 2023 (on an annualized basis) from $651 billion to $723 billion. Gross private investment as a whole runs to over $4.5 trillion and is trending down, not up.

So the upshot is that we have a particular sectoral boom nested within a much less exciting aggregate picture.

The story turns completely around if we move from nominal figures to investment measured in constant dollars. In inflation-adjusted terms, total investment in structures is up only 5 percent. Equipment investment is down. And Gross Private Domestic Investment in the first quarter of 2023 is down by 5 percent in real terms.

The aggregate numbers also put in context the larger claims made for the longer-term impact of the IRA. Let us assume that the Goldman Sachs prediction comes true and the IRA does generate $ 3 trillion in investment over ten years. That is a lot of money. But in 2021 the US already invested over $80 billion in its electricity grid. $ 300 billion in transportation equipment. Hundreds of billions went into fossil fuels. The lesson is simple, in an economy the size of the American one, $300 billion per annum in investment, which in part replaces existing spending on the fossil fuel economy, is an incremental rather than a revolutionary change.

***

Of course, you could say that all broad-based economic industrial transformations start this way. It is famously true that investment in IT and digitization took years to show up in broad-based productivity increases. Likewise, the industrial revolution of the 18th and 19th centuries worked its way slowly across the economy. The green industrial revolution has already begun in electricity generation and in the accelerating transition in motor vehicles. It will spread pervasively across the entire economy. If measures like the IRA help to accelerate these trends that will be their ultimate historical vindication. It seems likely that 2022 will come to be seen as an important turning point in the history of the American energy transition. But whilst acknowledging this, it is important to be realistic about the quantitative scale of what is going on and above all to be realistic about its likely short-run impact on American society and thus on its politics. This is worth saying because the Biden administration sees its new industrial policy as three-pronged. It is designed to address the climate crisis, the challenge of Chinese competition and the inequality and divisions within society that have undermined American democracy. It may be good politics to talk up this ambition. They would no doubt have done more, if Congressional majorities had enabled them to do so. At the very least the Biden team can claim that they see the problems and have attempted creatively to respond to them. In terms of political messaging that may be enough. Let us hope so. For my part I’m reminded of that phrase that Obama’s Treasury Secretary Tim Geithner used to me in describing the challenge facing America’s liberal governing class. Theirs, he remarked, is an exercise in defying gravity.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you will receive the full Top Links emails several times per week