Newsflash: bank runs can actually happen in market economies and when they do, they do real economic damage. Yup! Economists proved this to their satisfaction in the ‘80s. Not the 1880s, but the 1980s. That was the moment when three intellectual pioneers found a way of fitting banks and bank failures into a workhorse economic model and specified a channel by which the failure of banks raised the cost of credit intermediation. And that matters because, “as we all know”, intermediating between savers and borrowers is what banks do.

I’m not normally into philistinism. I enjoy intellectual activity and game-playing for their own sake. In such an exercise, self-limitation, playing with rules, seeing how far a limited model will go, are all part of the point. But that activity should be pursued with a sense of modesty of purpose and a clear acknowledgement of the limits of the exercise one is engaged in.

What this year’s economics “Nobel” prize does is the opposite. It has the effrontery actually to celebrate one of the weakest dimensions of modern macroeconomic thinking – its extraordinarily limited ability to grasp the macrofinancial instability of modern capitalism. Rather than challenging the dogged refusal of the economics mainstream to take seriously thinkers who face the essential important of finance and its dangers for the modern world head on, it flaunts the tendency of the mainstream to ignore them.

Cameron Abadi and I discuss the award on this week’s Ones and Tooze podcast.

Not only is the award a gratuitous exercise in self congratulation on the part of a discipline that has huge difficulty in shoe-horning reality into its models. It is also untimely.

As Wolfgang Munchau rather unkindly remarked, the prize seems like a retrospective celebration of the heyday of “boomer macro”, the age, in the 1980s, when the new Keynesian synthesis of macroeconomics with microfoundations finally demonstrated to its own satisfaction that bank runs could actually happen and careers could be made, as Ben Bernanke’s was, by demonstrating, by way of a new take on the 1930s Great Depression, that finance might matter for macroeconomics. All this amidst the Volcker shock, the Savings and Loans crisis and the Latin American debt crises … back to the future indeed!

On the podcast I was somewhat unfair in saying that the Prize committee makes no mention of the work of Hyman Minsky. That is not true. The scientific background paper to the award mentions Minsky in a footnote and cites him once en passant in the body of the text. But it does so only to emphasize that Minsky’s thinking was marginal to the mainstream, which insisted in arguing that a debt-deflation could have no macroeconomic impact because its effect, by raising the real value of debts, was merely to redistribute from debtors to creditors. It took Ben Bernanke to establish the real significance of bank failures in a way that the rest of his colleagues could persuade themselves to take seriously.

Along with Minsky, the unapologetic footnote in the Prize committee report also (sort of) cites Fred Mishkin 1978 paper on “Household balance sheets and the Great Depression” (the paper is actually omitted from the bibliography). The committee also mentions Charles P. Kindleberger, who taught at international economics and economic history at MIT.

In 1973 Kindleberger published The World in Depression 1929–39 in which he gave due emphasis to the debt-deflation mechanism. Kindleberger’s was the definitive history of the Great Depression, until Barry Eichengreen published Golden Fetters in 1992.

Coincidentally, Perry Mehrling – the great “money view” economist – has just published an intellectual biography of Charles P. Kindleberger, which I had the pleasure of reviewing in the New Statesman.

As the Sveriges Riksbank Prize committee noted, Kindleberger, like Minsky, held fast to the obvious fact that money mattered. And it mattered not just nationally. Through the channels of global capitalism, it mattered globally.

What Mehrling helps us to understand is that Kindleberger was not just an analyst of inter-national finance, of balance of payments and currency, of the gold standard and Bretton Woods. Kindleberger was something even more interesting. Kindleberger was a theorist of money and banking as inherently transnational, as cosmopolitan, as anchored in a mesh of private balance sheets as well as in the power of empires and nation states.

As Mehrling allows us to see, if we think of money as inter-national, we succumb to a methodological nationalism, which posits the national unit as the primary unit, which is then related to other national units, as one island is connected to another. In fact global money circulates across borders, currencies and balances sheets, with ownership, accounting and control dispersed in space.

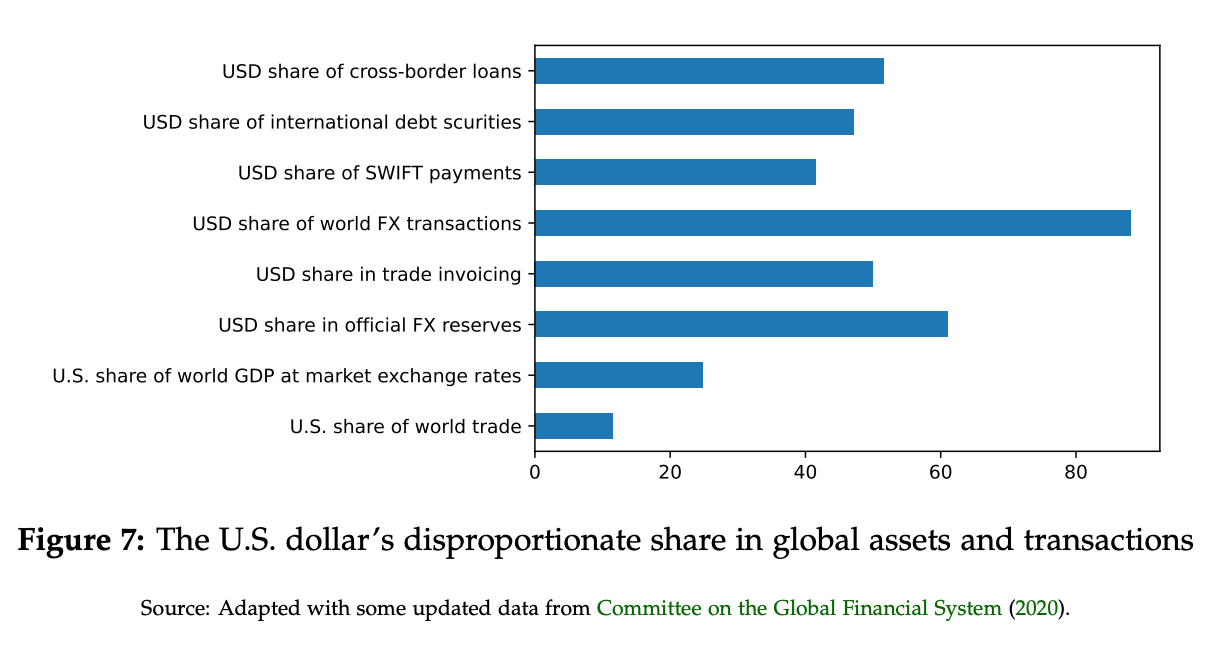

So when we metricate the scale of the dollar’s global reach by putting together a chart like this, which compares flows of global finance with national economic aggregates like shares of global GDP, we are engaged in a comparison of apples and oranges.

Source: Obstfeld and Zhou

There is nothing inherently wrong with such a comparison, but we should be clear about the incongruity and its implications.

Hyun Song Shin has given us what is surely the most effective graphic illustration of this point in this brilliant presentation. Inter-national economics offers the island view. Kindelberger’s cosmopolitan understanding of the dollar system is the networked, matrix view.

As Mehrling notes, it was a sad comment on Kindleberger’s lack of influence that his line at MIT was filled after his retirement by Rudiger Dornbusch, who would become perhaps the preeminent inter-national economists of his day. Dornbusch was a thinker of huge influence and reach, but, as an international macroeconomist, his basic conception of the world economy – the island view – was fundamentally at odds with that of Kindleberger.

Mehrling’s book combines a subtle and interesting intellectual history with a conceptual history. He could have gone far further with his historical exploration. That is a point for another time. But even in the sketch form that he offers, the pay-off is huge. As Mehrling suggests, Kindleberger was perhaps better able to analyze money beyond the nation-state framework, because he was trained by a generation of American monetary economists for whom the existence of an independent American national monetary system was anything but a given.

America’s financial system as a national unit, in fact came into existence between the late-19th and the early 20th centuries. And it came into existence under the influence of international forces, most notably the shock of World War I, which helped to weld-together America’s national financial system, under the supervision of the Federal Reserve. America’s national central bank itself had only been founded as recently as 1913.

With dramatic speed, in short, the US moved from a position of peripherality to centrality in the global financial network.

If you follow the Mehrling-Kindleberger line, if the Sveriges Riksbank Prize committee had actually wanted to reward economist who have enabled us to understand the dynamics of the modern global financial system and its interconnections with the real economy, the prize should have gone to the team at the BIS going back to the William White era and the academic economists associated with them today, most notably Hyun Song Shin.

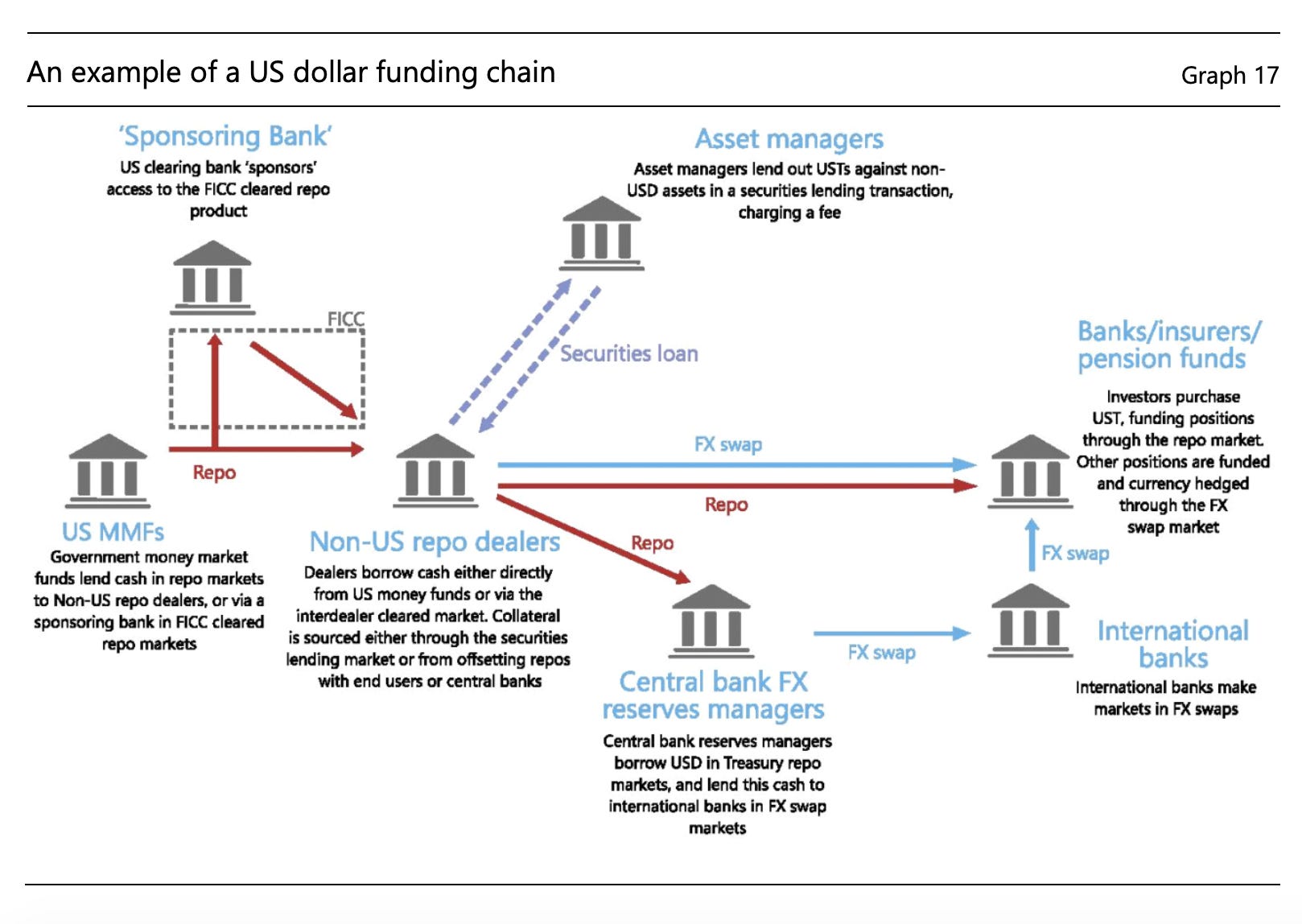

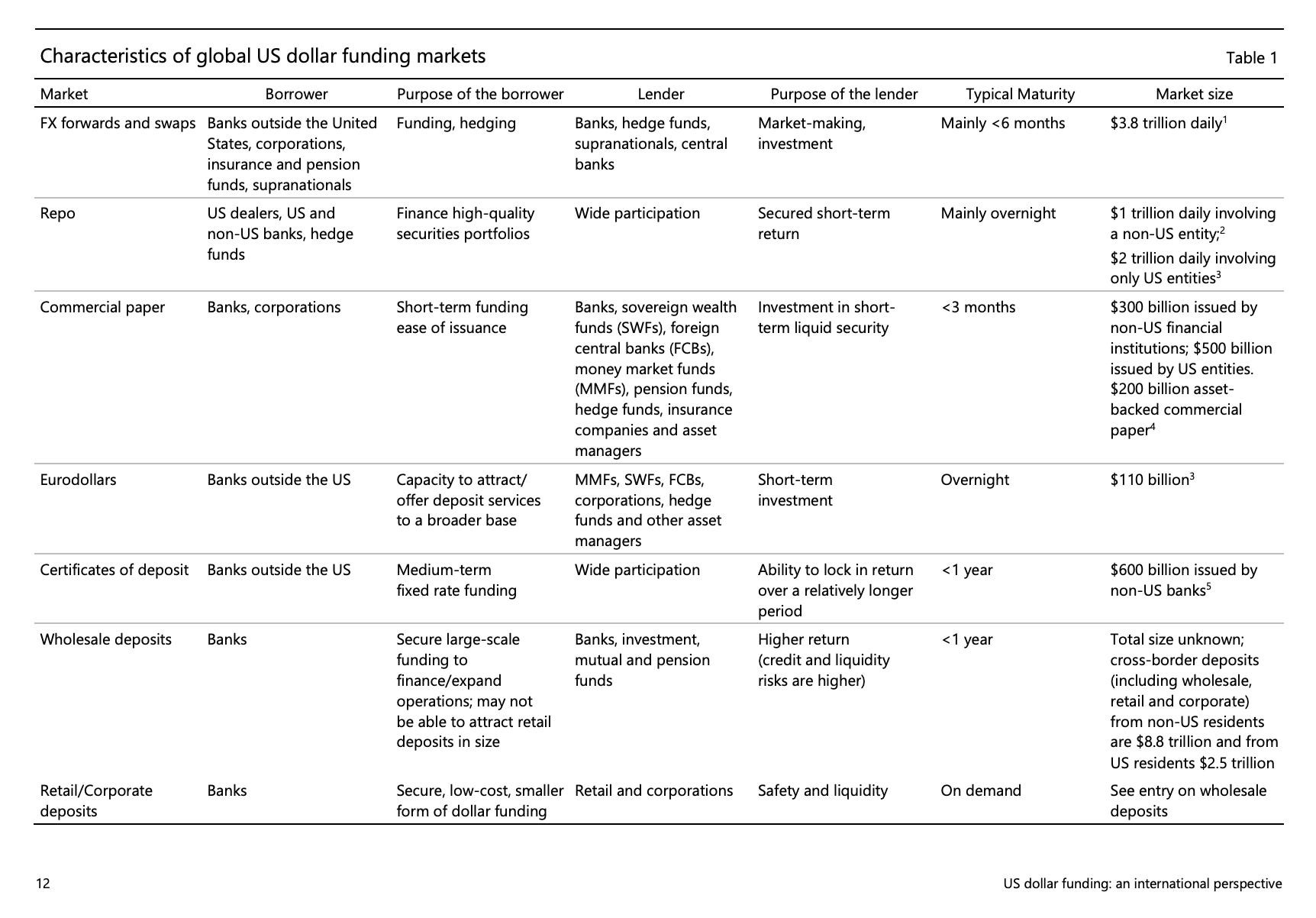

If you want to understand how credit is created globally, don’t start with the neoclassical fable of households savers and borrowers that sits at the heart of the Diamond and Dybvig model (And yes I do know that that does not exhaust D&D’s contribution and that run dynamics of the type they describe happen in market finance too!). If you want to understand the modern system, start with a diagram like this one, as recently drawn by a BIS team.

This is the market-based network of global finance on which the global role of the dollar rests. If you want to understand how ramified the dollar network is, consult this hugely instructive chart, also compiled by the BIS.

I cannot resist quoting extensively from this BIS report since it captures so clearly the forces that underpin the continuing dynamism of the dollar system and speaks so directly to the world as seen by Kindleberger.

The growth of global US dollar funding in recent years has largely been driven by market-based financing. Over the past five years, around three fourths of the increase in international US dollar funding has been in the form of marketable debt securities rather than bank lending. In that time, the stock of US dollar international debt securities has risen relative to global GDP, while bank lending has shrunk relative to global GDP to around its levels of the early 2000s (Graph 10, left-hand panel). As a result, international US dollar debt securities now exceed bank loans, having been around 60% as large a decade ago.20 The increased prominence of market-based funding has reflected a range of factors, some of which are not unique to US dollar activity. As discussed, banks’ asset growth has been limited, as they have focused on improving risk management and repairing balance sheets. While post-crisis banking regulations have improved the safety and soundness of the banking system, the increased cost of intermediation may have also encouraged some activities to migrate outside the banking sector. In addition, there has been strong demand for securities from institutional investors, reflecting rapid growth in their funds under management amid a search for yield in an environment of low global interest rates. NBFIs have also become increasingly important as issuers of debt securities (the dark blue area in the right-hand panel of Graph 10).

Borrowers and lenders of US dollars usually rely on intermediaries. A characteristic of international US dollar funding markets is that they may involve several layers of intermediation that give rise to long and complex funding chains and result in significant interconnectedness for the financial system, more than in most domestic markets. Graph 17 provides illustrative examples where US MMFs act as ultimate lenders; non-US entities are the ultimate users of dollars; and non-US repo dealers, the FICC, central bank FX reserves managers and international banks act as intermediaries. These funding chains cut across jurisdictions and sectors, and add complexity. In addition, it is often the case that whole chains and their interconnections are not visible.

This is a long way from the world with which Kindleberger was familiar, but it is a world which his cosmopolitan (as opposed to international) vision of global finance, was perfectly adapted to analyzing. As Mehrling argues, it constitutes a retrospective vindication of his insistence on the need to understand money’s tentacular flow beyond the boundaries of the nation state.

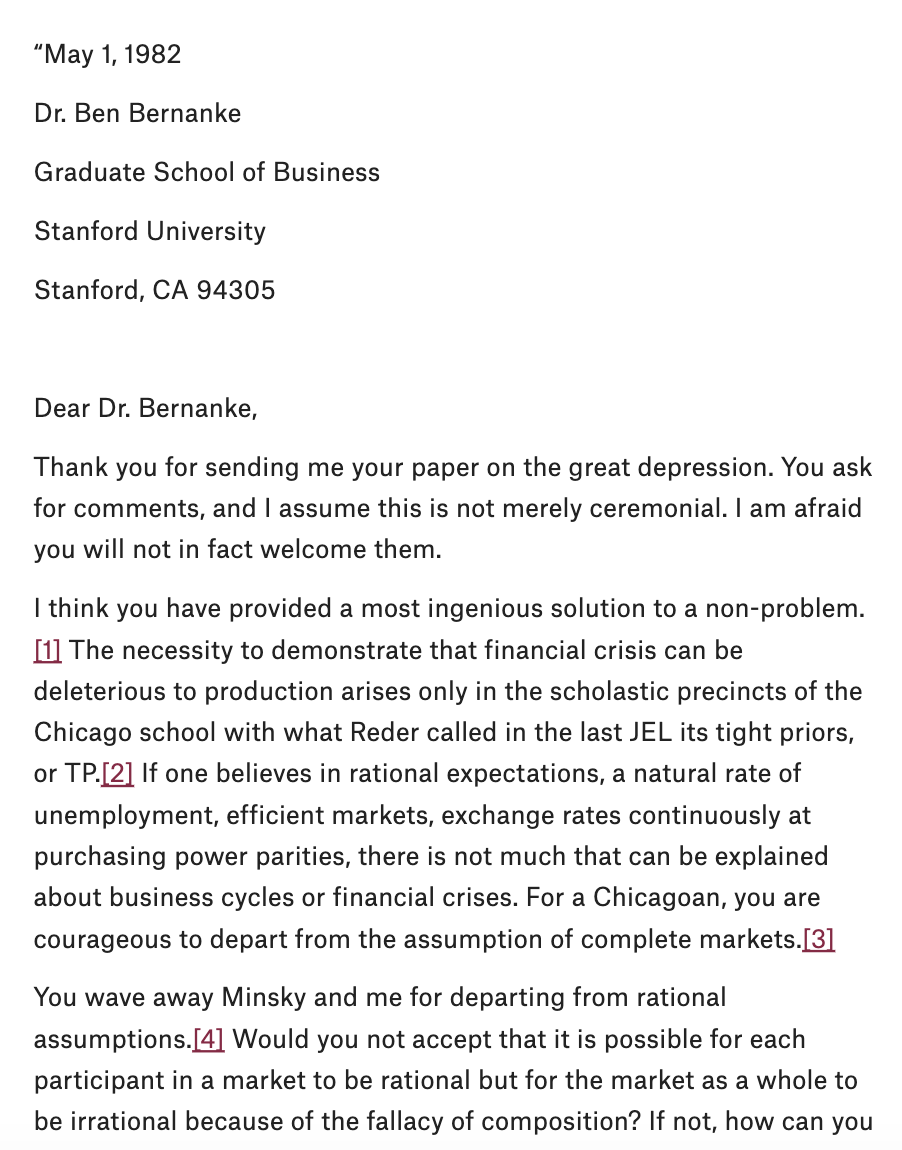

Kindleberger may not have lived long enough to analyze the latest generation of market-based finance. But in the 1980s he was very much alive and kicking. Indeed, he trained many of the cohort of macroeconomists at MIT to which Bernanke belonged. So, when the up-and-coming Ben Bernanke drafted the paper which is cited in the Nobel committee report – Non-Monetary Effects of the Financial Crisis in the Propagation of the Great Depression (1983) – he sent a copy to Kindleberger for comment. Miraculously, Perry Mehrling found Kindleberger’s reply in the archive and has published it on the INET platform.

… and it goes on from there.

****

I love writing this newsletter. It goes out for free to tens of thousands of readers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, there are three subscription models:

- The annual subscription: $50 annually

- The standard monthly subscription: $5 monthly – which gives you a bit more flexibility.

- Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.

Several times per week, as a thank you, all paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images.

To join the supporters club, click here: