The current situation of unexpected and rapid price increases, has forced us to define more clearly what is inflation. In a nominalist vein you could say simply that inflation is whatever the CPI or some other index says it is. And for everyday purposes it is almost perverse to refuse this simple answer.

But from an economic point view, as the BIS puts it, in a remarkable section of its recent Annual Economic Review, we need to make a crucial distinction:

The distinction between relative price changes and underlying inflation is critical. Relative price changes reflect those in individual items, all else equal. This may or may not be related to underlying inflation, ie a broader-based and largely synchronous increase in the prices of goods and services that erodes the value of money and devalues the “unit of account” over time.

There is a lot to unpack in this crucial passage. We are in a state of inflation when all prices – both those for goods and labour (i.e. wages) – are going up, broadly speaking in parallel. If that happens, since all prices are moving, the only fixed point from which to measure the change is that offered by the unit of account, i.e. the unit of money. This is the deeper meaning behind Friedman’s famous comment that inflation is always and everywhere a monetary phenomenon.

Price movements can do many things and have many meanings and effects. But those price movements that qualify as properly inflationary are those which collectively shift the ratio in which “all goods and services” exchange with the unit of account.

What the BIS shows in its remarkable chapter on inflation in the latest Annual Economic Review is that in this strict sense, in the decades since the 1990s when price indices were growing at very low rates, often well below 2 percent and in Japan even declining, not only was “inflation” low, but in a strict sense, price movements no longer qualified as inflation at all (fast or slow). Price movements were increasingly uncorrelated with each other and crucial connections e.g. between energy prices and the general index became much less significant in statistical terms.

Inflation – the movement in the general price level – was not just low. It would be better to say that inflation had attenuated to the point of irrelevance. It was no longer a reference point. Indeed, successive Fed chairs, Paul Volcker and Alan Greenspan adopted defined price stability precisely in these terms:

“a situation in which expectations of generally rising (or falling) prices over a considerable period are not a pervasive influence on economic and financial behavior.”

The macroeconomic dimension of prices and money “in general” was no longer relevant. The price changes that were observed were interpreted in microeconomic terms i.e. as shifting relativities between goods and services rather than being indicative of the general state of the economy or society. The general price level, one of the basic macroeconomic variables, was no longer a relevant reference point.

By contrast, an inflationary period is one in which issue of the general price level, as captured by an index, or perhaps the exchange rate, comes to dominate all other considerations. What matters, in the first instance, are not relativities, but keeping up with the overall level. In this state, the macroeconomy emerges from irrelevance, to be the dominant, overriding concern for all decision makers.

When prices rise faster, we miss the point if we simply say that inflation is higher. Reading the BIS report between the lines, it would be better to say that as rate of price increases increases, “inflation happens”. We enter an inflationary state.

To survive, investors have to shift from being stock pickers, to macro bond investors.

What is remarkable about the BIS’s recent report is that is able to show in extraordinarily rich empirical detail how the emergence and then disappearance of inflation as a macroeconomic phenomenon played out over the last half century.

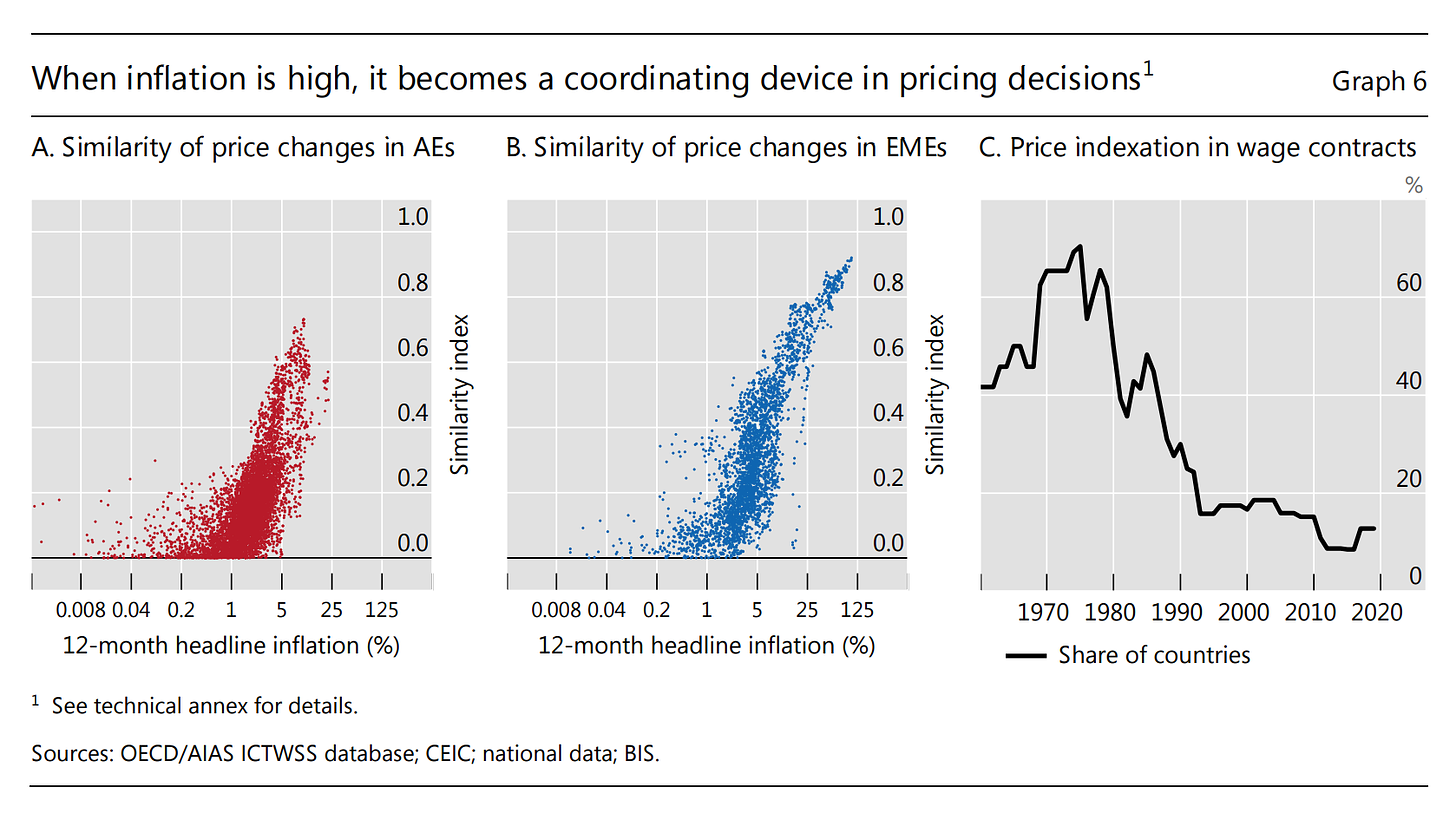

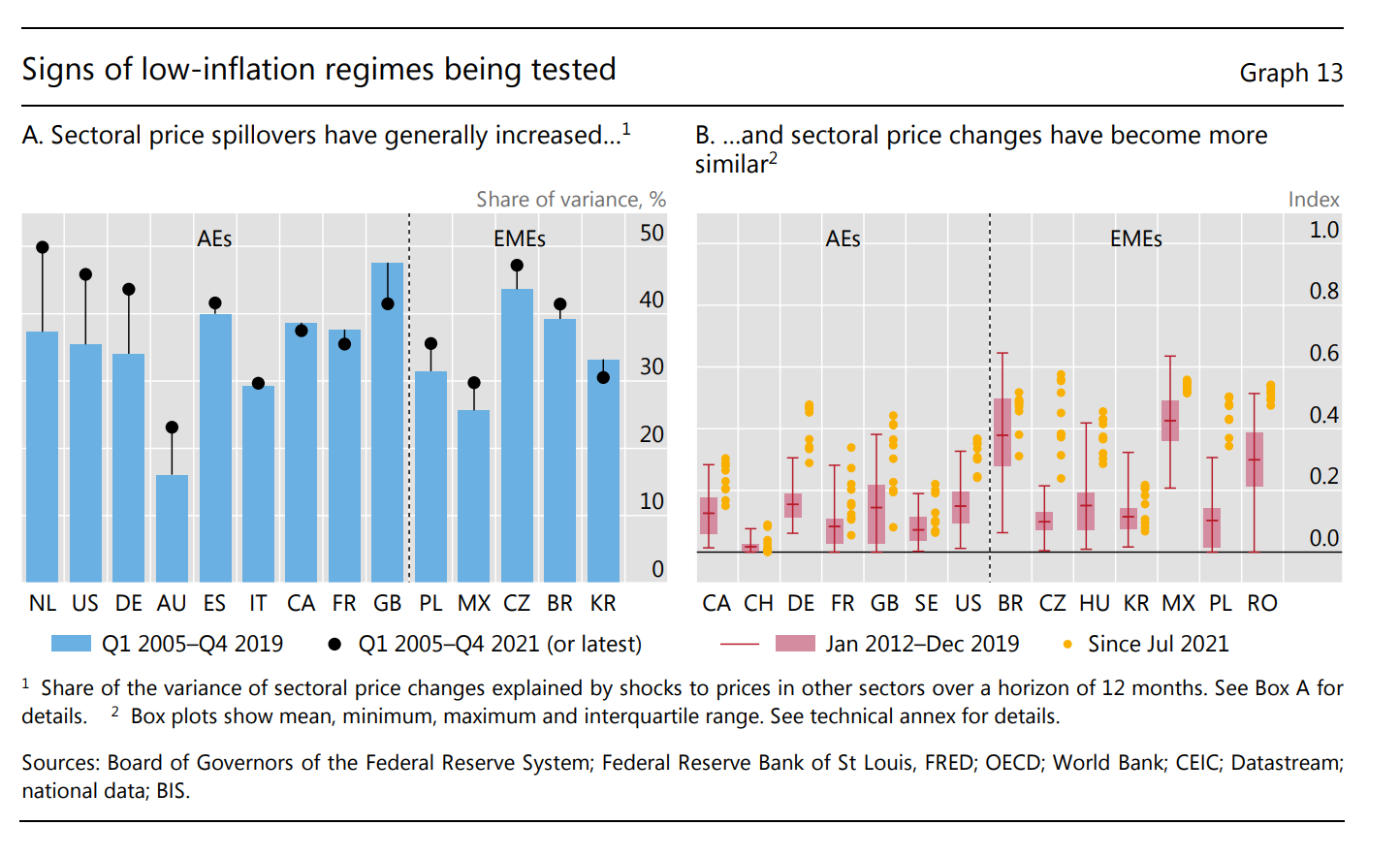

One crucial index of this process is simply how far price changes begin to resemble each other. In an non-inflationary situation price changes are idiosyncratic, driven by supply factors, particular business decision or bargaining strategies by trade unions. As inflation takes over, that changes:

the degree to which the general price level becomes relevant for individual decisions increases with the level of inflation. When inflation rises, price changes become more similar

This effect can be achieved through explicit social agreements and contracts e.g. price indexation. But the BIS’s data analysis allows them to show this effect in operation across price-setting more generally. In Advanced Economies, once inflation rises to around 5 percent, the similarity of price-setting surges. For emerging market economies, with inflation experiences that go as a high as 25 percent, the effect is even more pronounced.

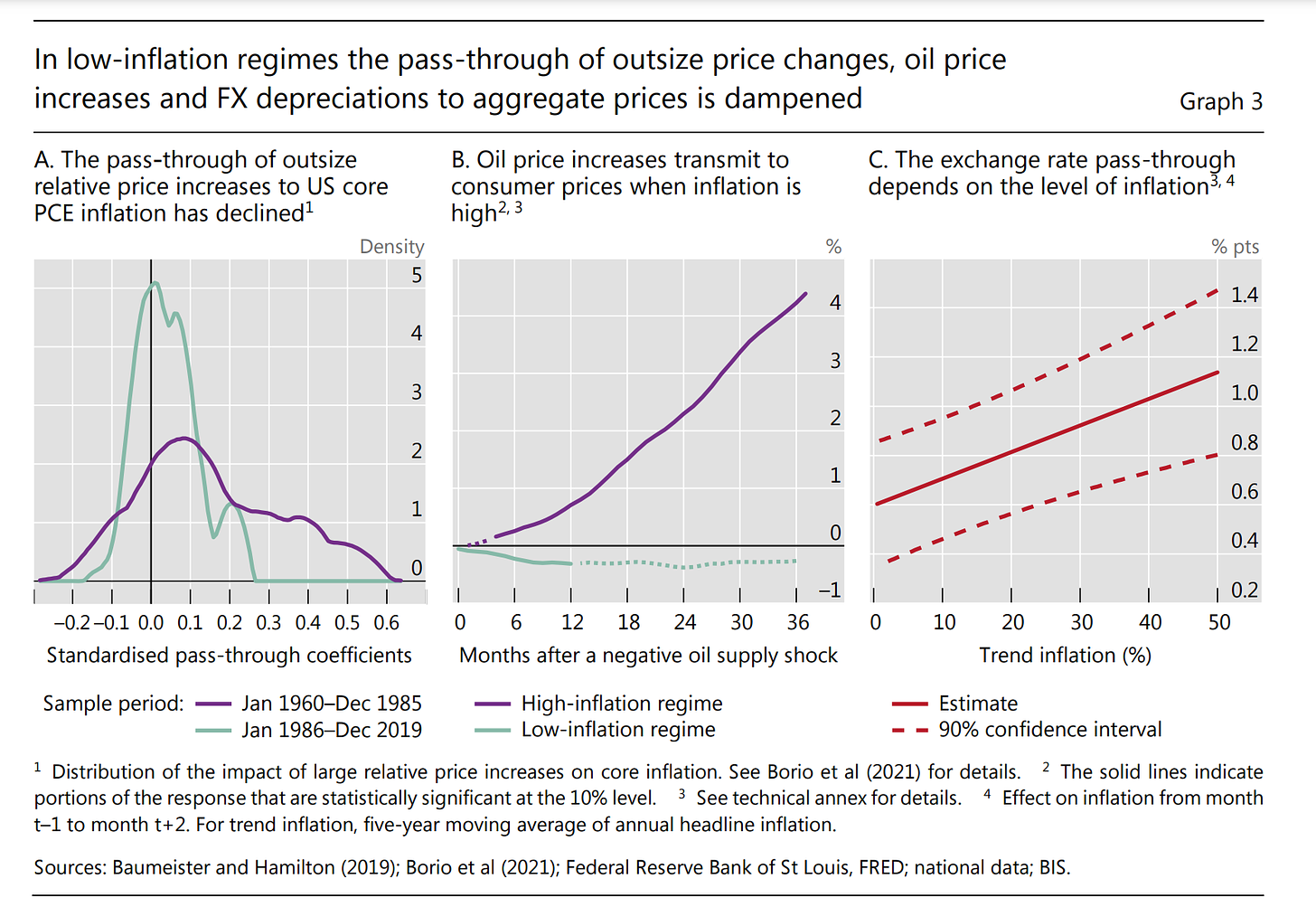

As inflation becomes the dominant concern, what we see is the emergence of key prices that help actors to orientate themselves in an increasingly confusing scene. Energy prices and exchange rates, for example, have a far larger influence on the general price index in high inflationary regimes than in low inflation regimes.

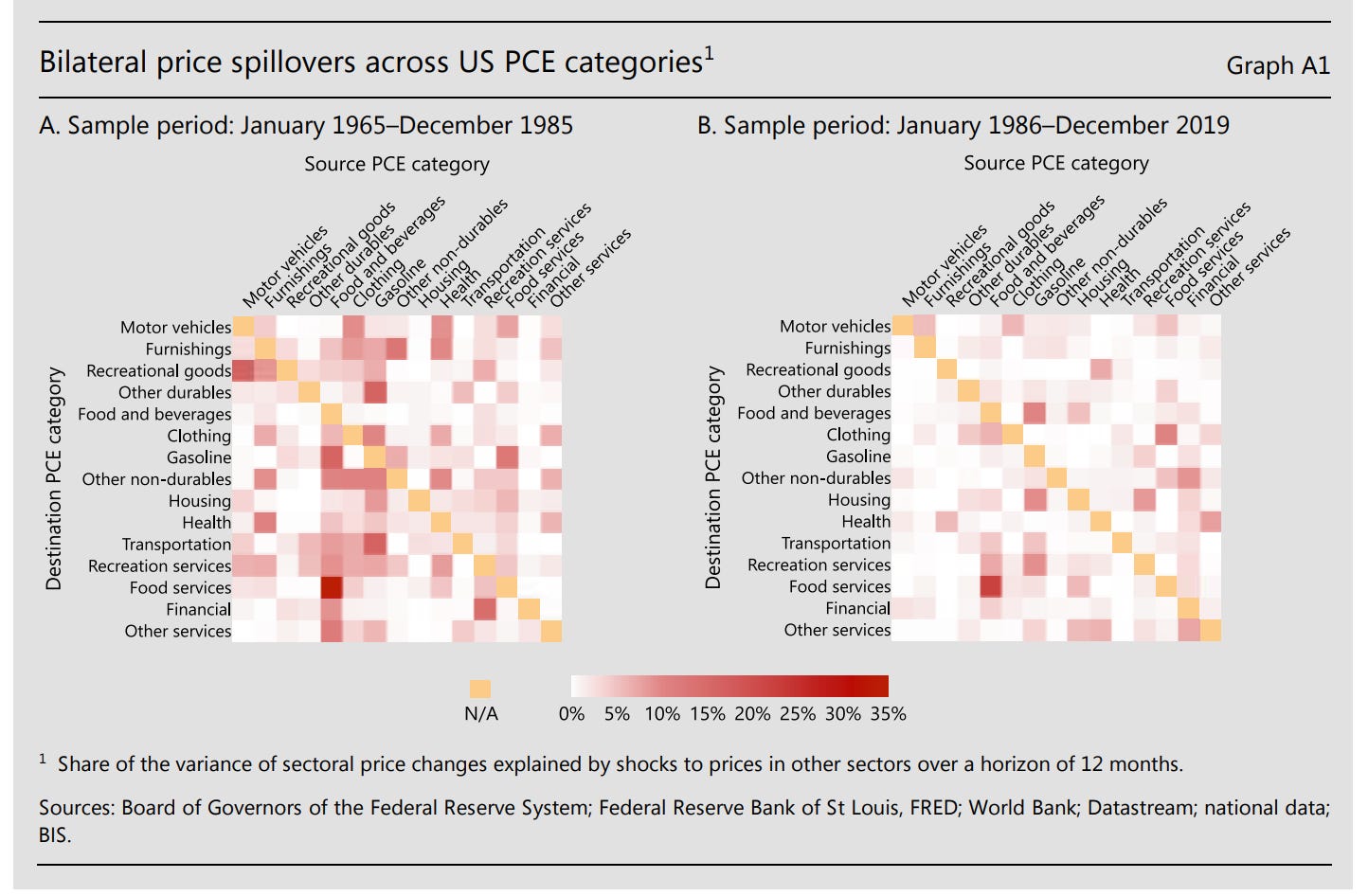

But one does not have to confine oneself to examining just the headline numbers like oil and the dollar exchange rate. What the BIS has constructed is a general measure of the degree to which shocks in the price of one sector affect the rest of the economy.

Examining how shocks to prices in certain sectors transmit and propagate to others can help shed light on how individual price changes are able to morph into broad-based inflation. One relatively simple way to do this is to look at how shocks affecting certain sectoral price indices affect the variability of prices in other sectors within a certain horizon.

The key ingredient for the construction of the spillover indices is the generalised forecast error variance decomposition (GFEVD) matrix.2 This measures the share of the variance of each PCE sector (the rows) explained by shocks to each of the sectors (the columns).

Apart from the fascinating sectoral details, what the comparison of the matrices from the high-inflation period (on the left) and the low-inflation period (on the right) shows is how inter-sectoral price linkages become attenuated as inflation falls. The matrix on the left has fewer dark-red cells.

Higher inflation per force constitutes “an economy” that moves as an articulated organism, with ripple effects running from one sector to the other. As inflation fell from the late 1980s onwards, those connections became progressively attenuated.

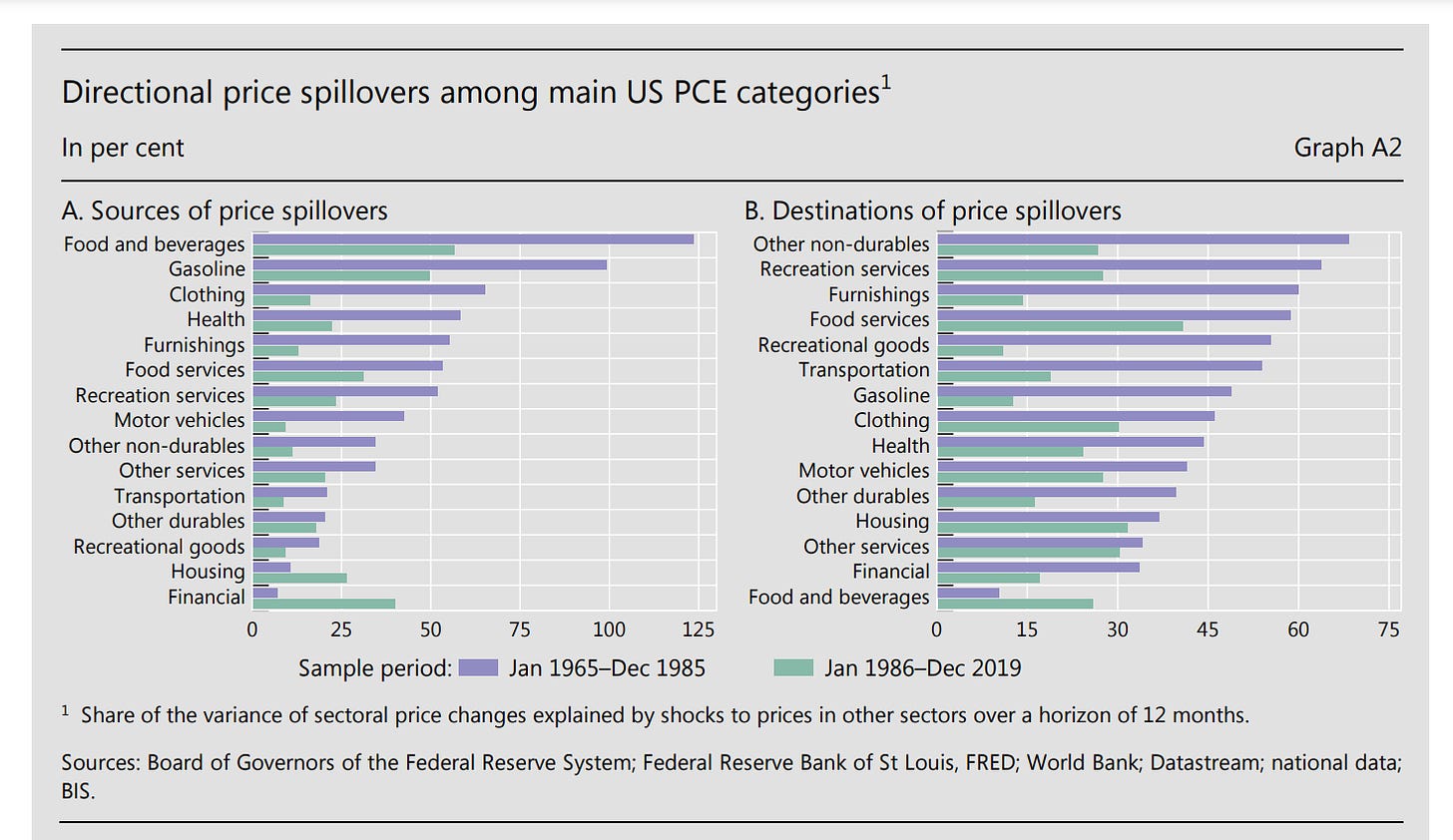

For ease of reference this result can also be broken down by particular index components. In the period 1986-2019 the key sectors no longer delivered the kind of shocks that they did in the 1965 to 1985 period, the period of the “great inflation”. Conversely, price movements which before 1986 were heavily influenced by shocks in other sectors, became less and less susceptible.

Though the BIS does not apply a political economy lens to these numbers, it would be possible to do so. The question is who has price-setting power and who does not. Who are price-takers. Because the matrices are based on the PCE price index they do not include wages, but, as I discussed in Chartbook #133, the BIS has shown how in an inflationary regime, wages are more responsible to prices and conversely prices are more responsive to wage pressure.

What worries the BIS right now is that even in the short space of time since the summer of 2021, as prices have surged, there are signs that what we are witnessing is something akin to a true inflationary process of correlated, spillover-driven, imitative price changes.

On an alarmist reading, the point is not simply that prices are rising, but thatt inflation (in the general macroeconomic, Friedmanite sense) is baaaaaaaaaack.

This may indeed be alarmist. Crucially, the signs of a wage-price spiral which, as the BIS acknowledges, is crucial to any truly general inflationary process, are weak at best.

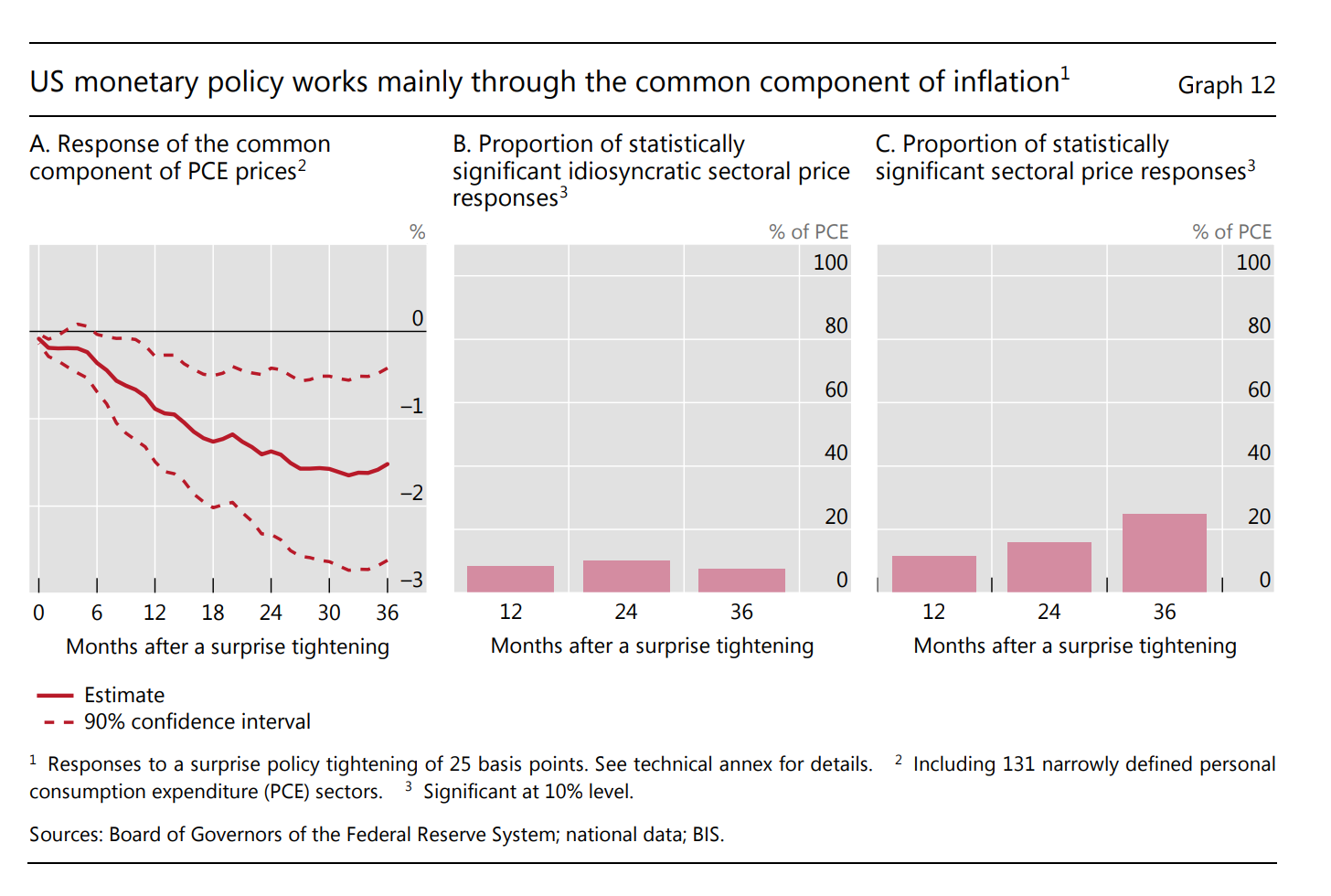

Furthermore, the report adds an interesting consideration about policy.

Monetary policy – as in central bank interest rate setting – operates most powerfully on the common, general component of price increases.

In the low-inflation environment of recent decades it was not for nothing that central banks had to resort to unconventional measures. Their instruments have little bite in a world of microeconomic price movements.

As of early 2022 this has clearly changed.

The contention of those who refused to be panicked by inflation and still are not panicked, has always been that, if inflation were actually to occur, policy-makers had the tools to deal with it. That contention is now going to be put to the test.

*******

I love writing Chartbook and I am particularly pleased that it goes out free to thousands of readers all over the world. But it takes a lot of work and what sustains the effort is the support of paying subscribers. If you appreciate the newsletter and can afford a subscription, please hit the button and pick one of the three options.