It is hard to exaggerate the scale of the sell-off in China’s stock markets last week.

The drama caught my attention as it did the attention of my eagle-eyed friends Robert Armstrong and Ethan Wu over at the FT’s Unhedged newsletter.

So, it seemed obvious to make China and its prospects the subject of the first of three paired newsletters between Chartbook and Unhedged – call it Uncharted or Hedgebook (h/t @joshspero).

Chartbook will feature three pieces written by the Unhedged team. The first you will find below. To read my piece today, click this link for exclusive free access to the FT’s Unhedged newsletter.

The current plan is to exchange columns every Thursday for the next three weeks.

If you don’t subscribe to the FT’s Unhedged newsletter already, you are missing out. If you are interested in following the mind of the financial markets there really is no better source.

The analysis from Unhedged is sharp. Sometimes technical, but never impenetrable. Plus the writing is great. It is, no kidding, the first thing I check in the FT every morning. It’s a pleasure to be in dialogue with Robert and Ethan.

Our pieces emerged out of email exchange and are closely keyed to one another. You can plunge into Robert and Ethan’s analysis below and then flip over to the FT using your exclusive link. Or you can start with me over at the FT and then come back here.

The choice is yours!

It is, frankly, very exciting to be able to offer readers of Chartbook exclusive access to top content from the world’s premier financial newspaper. In honor of the occasion, I wish I could tint the following newsletter pink. In any case …

… YOU ARE NOW ENTERING THE WORLD OF THE FT’s UNHEDGED:

Adam is clear-eyed about China’s challenges, but is optimistic that they can be overcome.

China’s investment-driven, debt-heavy development model needs replacement. Its geopolitical and economic position will become more precarious if the globe’s authoritarian and liberal democratic blocs decouple, a threat made vivid by the war in Ukraine. Its demographics will be a drag on growth. All of this is plain fact. But Adam sees reasons for hope:

- China’s technocrats have, to date, demonstrated competence in managing the economy’s imbalances. “By means of its ‘three red lines’ policy, [China] is stopping in its tracks the most dramatic accumulation of wealth in history … if Beijing manages to stop the largest property boom ever without a systemic financial crisis, it is setting an entirely new standard in economic policy.” Pricking bubbles before they burst and wreak economic havoc is exactly what the US has serially failed to do. “If we look in the mirror, why aren’t we applauding more loudly?” Adam asks.

- Similarly, the Chinese state’s recent intervention in the tech sector, while it has led to market volatility, is aimed at doing exactly what western regulators want to do, but can’t seem to do: stop huge companies from extracting monopoly rents from the economy.

- Beijing has policy options. “China needs a welfare state befitting of its economic development. It needs to get serious about ending its dependence on coal. If it needs more housing, it should be affordable. All of this would generate more balanced growth. 5 per cent? Perhaps not, but certainly healthier and more sustainable … if you had to bet on a state which might actually have what it takes to break a political economy log-jam, which would it be? The United States, the EU or Xi’s China?”

“On balance,” Adam sums up, “If you want to be part of history-making economic transformation, China is still the place to be.” Indeed there are certain sectors — green energy first among them — where serious investors really can’t reasonably avoid China.

At Unhedged, we have views about the first two points, but they are not well informed. We’re not policy guys. The third point is where we disagree. We just don’t see China as having any good options for maintaining strong growth.

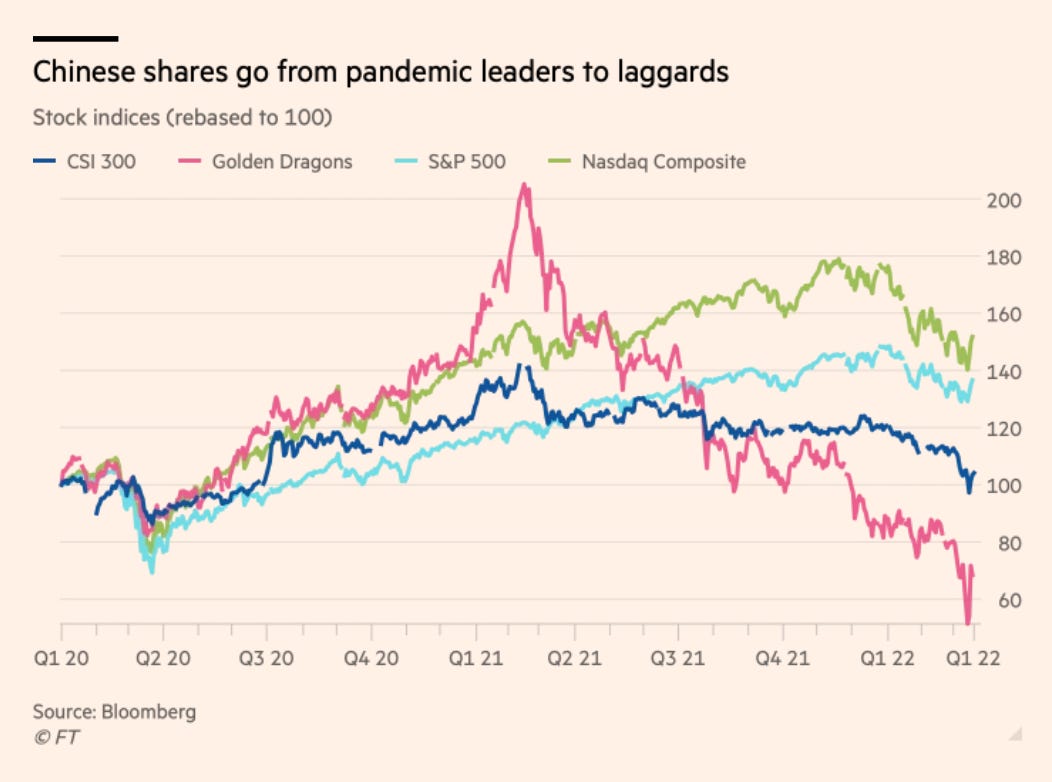

Up until now, investors in China’s equity and corporate credit markets have had to deal with extreme volatility driven by both unpredictable government policy and the fickle risk appetite of local Chinese investors. In return, they have participated in a remarkable growth story, and have been able to do so at a reasonable price, given the often attractive relative valuations of Chinese stocks and bonds.

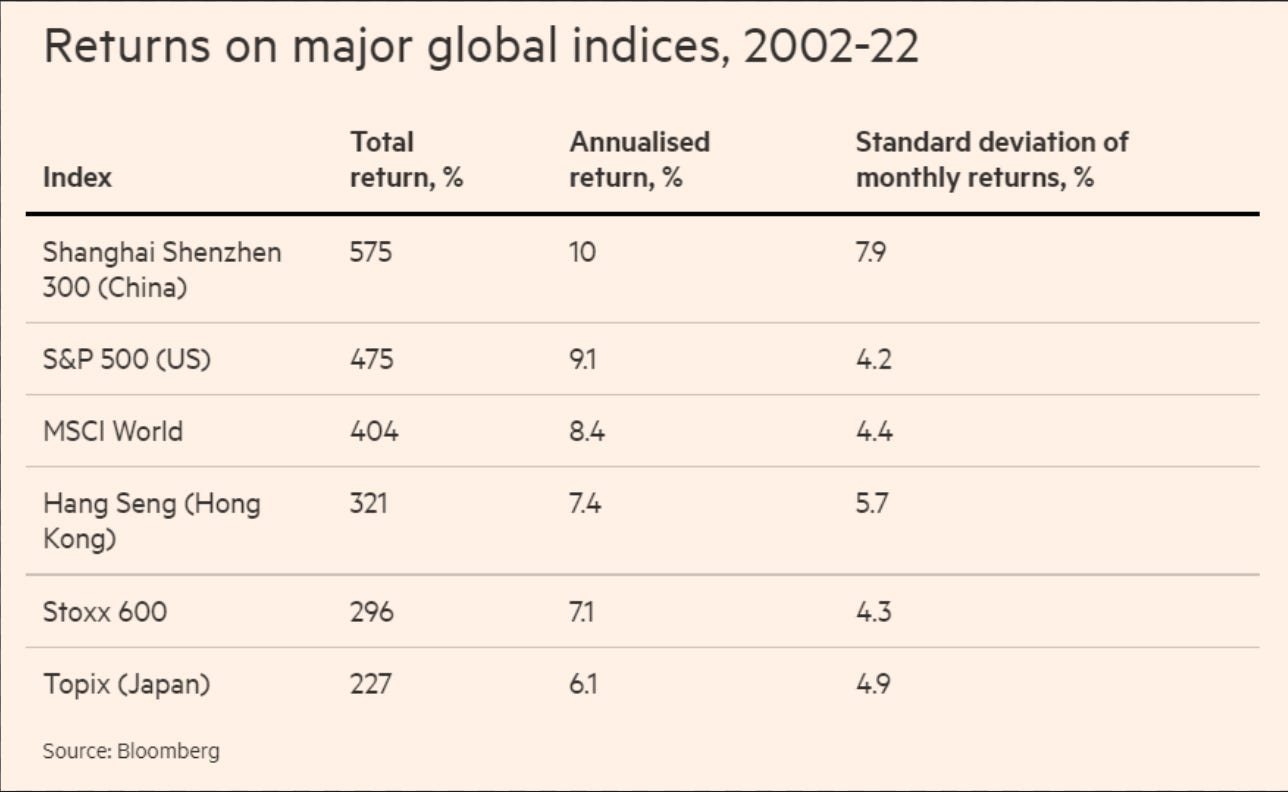

Focusing for just a moment on the stock market, mainland Chinese equities have performed well relative to the basic global alternatives over the long run. Here are 20-year total and annualised returns, all in dollar terms, through the end of February:

Mainland China has delivered significant extra returns — 87 basis points a year more than the mighty S&P — for anyone willing to hack the wild volatility. But we think China’s underlying growth story is coming to an end as the country’s economic imbalances become unsustainable and global decoupling picks up steam. The volatility and low valuations, on the other hand, are likely here to stay.

What imbalances are we talking about? In crude summary, China’s growth has been driven by debt-funded investment, especially in property and infrastructure. The problem is that the returns on these investments are in fast decline, even as debt continues to build up. Here are China’s official GDP growth numbers and the country’s estimated debt/GDP ratio:

The imbalances in China’s economy have only gotten worse in the decade since the financial crisis. This can’t go on forever. Eventually, you have all the bridges, trains, airports and apartment blocks you need, and the return on new ones falls below zero (How do you know that you have arrived at that point? When you have a financial crisis).

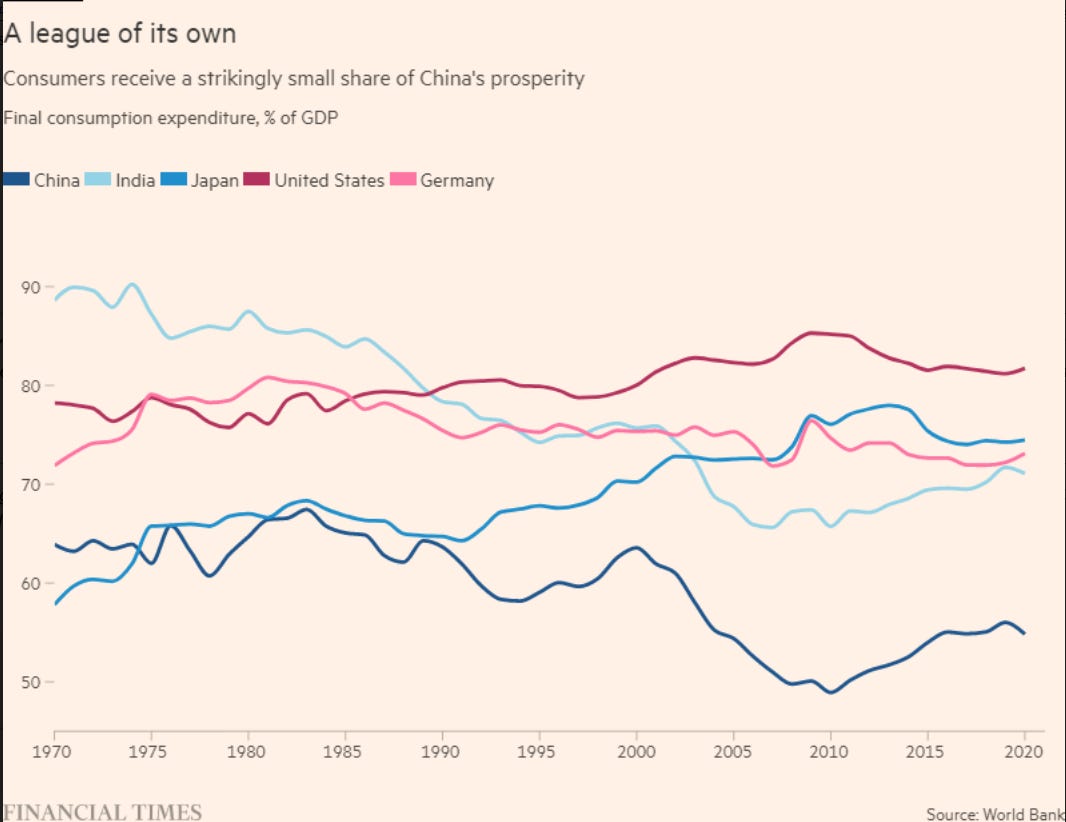

Another way to describe China’s imbalance is that as the state has driven investment, its households — as opposed to the business and government sectors — have received a very small share of GDP. Here’s an international comparison:

The problem is that without a healthy consumer, China’s only real options to create growth are investment and exports — and at the same time as return on internal investments are declining, the rest of the world, led by the US, are increasingly wary of dependence on Chinese exports.

Household income growth has fallen over time:

What are China’s policy options? Broadly, there are five, as Micheal Pettis explained to us:

- Stay with the current model.

- Replace bad investment in things like infrastructure and real estate with good investment in things like tech and healthcare.

- Replace bad investment with domestic consumption.

- Replace bad investment with (even) move exports and a wider current account surplus.

- Just quit it with the bad investment.

At Unhedged, we think that options 1 and 5 are not really options at all. The current model will lead to a financial crisis as return on investment falls further and further behind the costs of debt. Simply ceasing to overinvest in infrastructure and real estate, without changing anything else, will simply kill growth.

What about options 2-4? Option 2 might be summed up — as Jason Hsu of Ralient Global Advisors summed it up to us — as China becoming more like Germany. Hsu argues that Chinese policymakers are very focused on not falling into the same developmental traps as Japan, whose investment-heavy model blew up in the late 1980’s, leading to a period of very low growth that persists today (Japan, it should be noted, carried a burden into its crisis that China today does not: a massively overvalued stock market). The idea is that China would steer more and more money away from real estate and towards high value-add sectors from biotech to chip manufacturing.

The problem with option 2 is that investment is such a huge part of the Chinese economy that it is difficult to see how that the capital could be efficiently allocated to the country’s tech-heavy, high value-add sectors, which are comparatively small. In 2020, China’s total capital formation (roughly, net capital invested in property, equipment, and inventories) was $6.4tn or 44 per cent of GDP, double the proportion of the US or Germany. Government policy would struggle to move a meaningful fraction of that to high-value-add sectors without creating hideous distortions. The most promising Chinese firms are swimming in capital as it is. And developing productive capacity isn’t just about capital. It takes things the state can’t rapidly deploy, like knowhow and intellectual property.

Option 3 is more promising. China could start, as Adam suggests, by building up a proper welfare safety net. But it is reasonable to expect pretty serious social and institutional resistance to this sort of mass redistribution. The income that would be distributed to households would come from the sectors that currently control outsized slices of GDP: government and corporations. They will resist. Local and provincial governments would be especially loath to give up resources and influence.

To put the same point another way: why hasn’t China increased its welfare state until now? Longtime China watcher and friend of Unhedged George Magnus suggests it is because of a deep bias in the Chinese policy establishment. “It’s how Leninist systems operate: they think production and supply are everything … if you see a demand problem as a supply problem, you get the wrong answers.” China’s latest policy solution to its growth problem, tax cuts aimed mostly at business, make exactly this mistake. The supply side in China doesn’t need help. Households do.

Option 4, increasing exports’ share of China’s economy even further, may be in the abstract the most appealing. But it runs directly into the fact that both China and the US and its allies have reasons to reduce mutual dependence on their economies. These reasons include China’s relationship with Russia, but are hardly limited to it. The US-EU policy establishment, for example, is not going to stand idly by while China increases its share of the semiconductor market. In the FT on Monday, our colleague Martin Wolf emphasised that the war will make the preexisting tensions worse:

The emergence of geopolitical divisions between the west, on the one hand, and Russia and China, on the other, will put globalisation at risk. The autocracies will try to reduce their dependence on western currencies and financial markets. Both they and the west will try to reduce their reliance on trade with adversaries. Supply chains will shorten and regionalise…

Russia must remain a pariah so long as this vile regime survives. But we will also have to devise a new relationship with China. We must still co-operate. Yet we can no longer rely upon this rising giant for essential goods. We are in a new world. Economic decoupling will now surely become deep and irreversible.

In all, the most likely scenario is that China’s growth just keeps slowing. That does not mean that investors in China will necessarily lose money. But it does suggest that generic China exposure — simply owning Chinese equity or credit indices — is going to be a losing proposition in the long-term. The analogy with Japan is again useful. The performance of Japanese indices has been awful for decades, but certain companies and even sectors have done unbelievably well.

Thanks for reading. Email us your thoughts: Robert.Armstrong@ft.com and Ethan.Wu@ft.com. We do hope you’ll consider subscribing to the FT. If you do, you not only get Unhedged, but the world’s best newspaper to boot.