Military experts warned us that the tension on Ukraine’s borders would reach its height in early February. Here we are and it is unbearable. How it must feel in Ukraine, I can only imagine. On Friday I was on an NYU panel reprising the argument of Chartbook #68. When we logged off we were plunged into the latest round of warnings leaked by US officials and amplified on twitter. My stomach flipped.

Is this the stress that Putin wishes to induce? Is this the stress it suits the US leadership to reflect back into the public sphere? Either way, it is horrible.

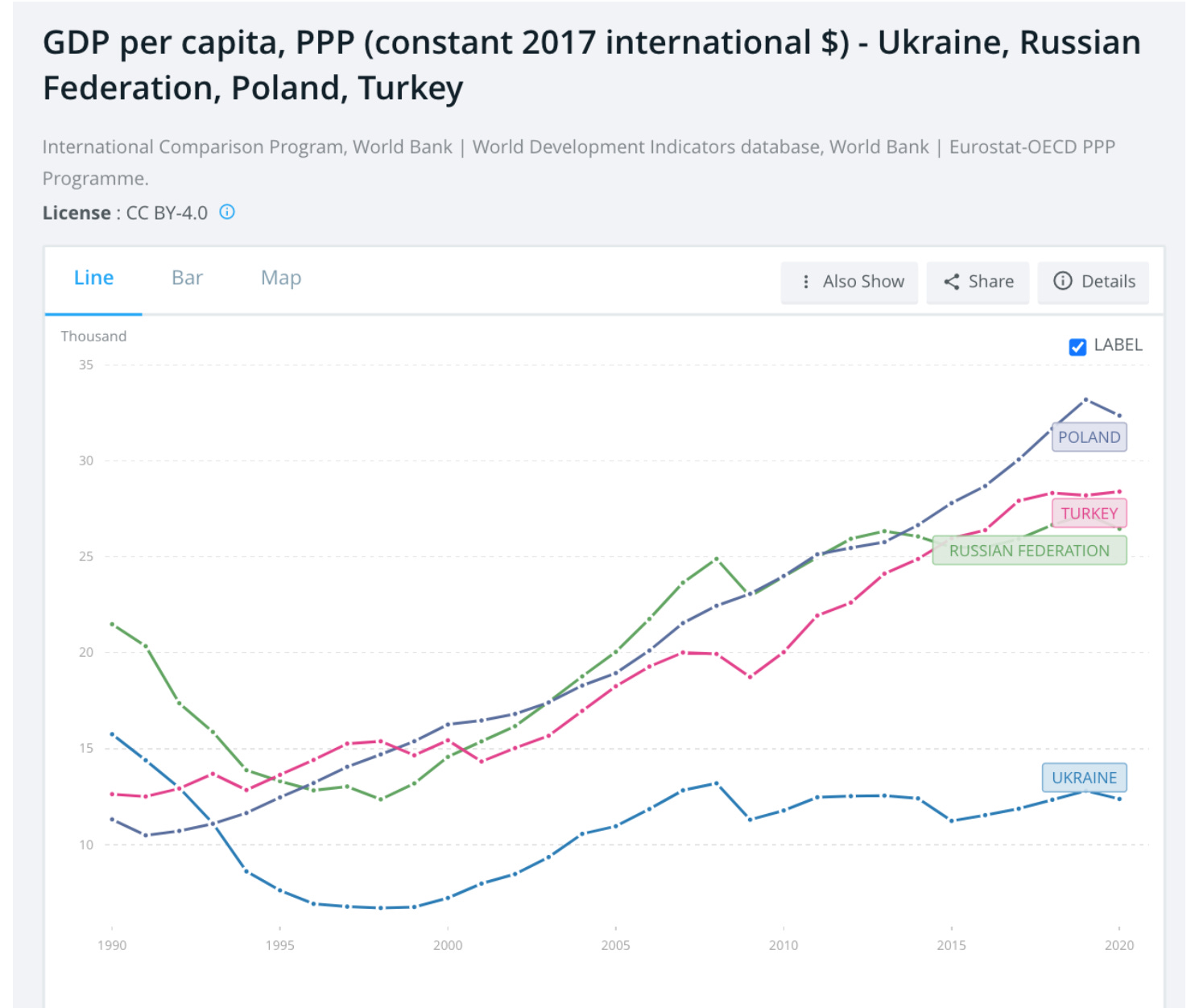

On the NYU panel, searching for grip, I came back to this graph which captures so dramatically Ukraine’s situation.

What is striking about it is that Ukraine’s economic development has failed both relative to Russia and to Poland. It is as though, Ukraine is the low pressure zone where two distinct fronts of global economic development are crashing into each other. Coming from the East, Russia’s development is driven by global commodity demand. To the West, Poland exemplifies development driven by intensive institutional change and incorporation into the EU. This image of fronts colliding haunted me whilst I was writing the East European chapters of Crashed. Today, again, I can’t help thinking of capitalism’s uneven and combined development in terms of a meteorological chart – two weather fronts clashing.

What is missing from this picture, is the United States. And this absence is significant. Right now, the issue of NATO expansion is in the forefront. But what triggered the clash in Ukraine in 2013-4 was not NATO but rivalry between EU and Russia. And as the image of “economic pressure fronts” suggests, there is good reason to think of the clash between the EU and Russia as the deeper conflict. That, certainly, is the “view from KCL”. King’s College London is home to a truly stellar group of historians, regional experts and strategic analysts. Sam Greene and Alexander Clarkson both delivered great threads this week.

I am not sure I would go as far as them in detaching the EU from NATO. It seems a false and unnecessarily sharp distinction. But the distinction is important. And it is constitutively awkward. As Director of the EI at Columbia, I have the pleasure of meeting a fair sample of senior European diplomats. After one event on Ukraine at which a very senior EU figure was touting the then ritual line that the “EU doesn’t do geopolitics”, I was buttonholed by an indignant Scandinavian official attached to one of the UN mission. Over wine and cheese he hissed into my ear: “THEY (i.e. Brussels) may say “no geopolitics”. They may even believe it. But WE (i.e. the Scandinavian and Baltic members) are definitely doing geopolitics in Ukraine.”

I don’t doubt it. The EU is not a unified coherent bloc. There are Baltic and Scandinavian members for whom EU and NATO membership are a package. There are Berlin and Paris tacking between the two and then there is Brussels and the EU apparatus with ambitions to develop an agenda of its own, an agenda, which, in part in reaction to the Ukraine debacle of 2013, is articulated increasingly explicitly geopolitical terms.

In any case, after flashing up the GDP data on the NYU panel, I was seized by a nagging doubt. Could these World Bank figures for GDP per capita really be correct? They are so extreme? Was there something wrong ? Was I – worst case – an unwitting organ of black propaganda against Ukraine? On the NYU panel the talk turned to “failed states”, a term vigorously rejected by those who know Ukraine’s politics far better than I do. After another 24 hours of hunting I am both happy and sad to report that the data do seem to stand up. Indeed, the situation is more extreme even than I portrayed it. In my chart I compare Ukraine to Poland, Turkey and Russia. A recent IMF paper places Ukraine in global perspective.

Source: WP/21/100 Assessing the Macroeconomic Impact of Structural Reforms in Ukraine by Anil Ari and Gabor Pula, April 2021.

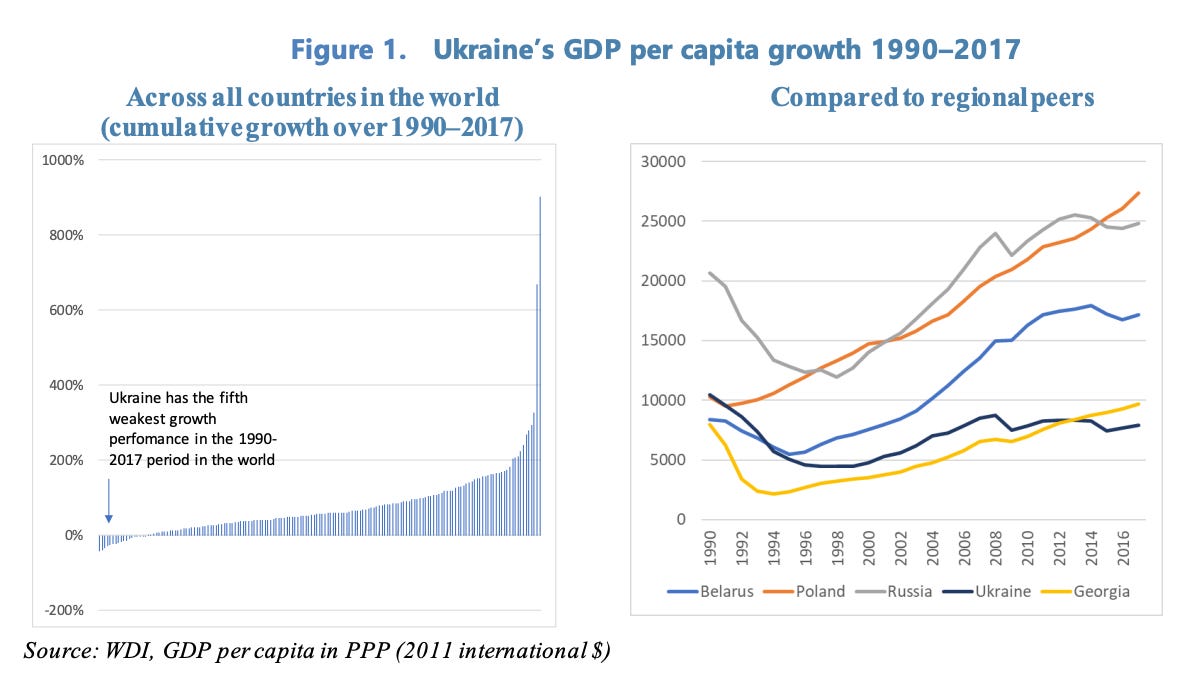

Ukraine’s performance between 1990 and 2017 was not just worse than its European neighbors. It was the fifth worst in the entire world. Between 1990 and 2017 there were all told only 18 countries with negative cumulative growth and even in that select group, Ukraine’s performance puts it in the bottom third. Amongst the four countries that delivered less growth for their citizens than Ukraine were the Democratic Republic of Congo, Burundi and Yemen.

Let that sink in for a second.

If we grant, as my co-panelists insisted, that Ukraine is not a failed state, what are we to make of this? If we insist, as we must, that sovereignty is the issue, what does sovereignty mean against this economic backdrop? A self-determining country with Ukraine’s great human and natural resources, whose polity is fraught but not failed, has experienced a generational stagnation, not at the high level of income enjoyed by Italy, for instance, but at 20 percent below its late-Soviet level. Perhaps the point to make, is that given this economic record Ukraine is the least failed state in the world? Or, as Volodymyr Ishchenko remarked on the panel, permanent crisis is Ukraine’s norm. A crisis of political economy that stretches back in time, over half a century, into the Brezhnev era.

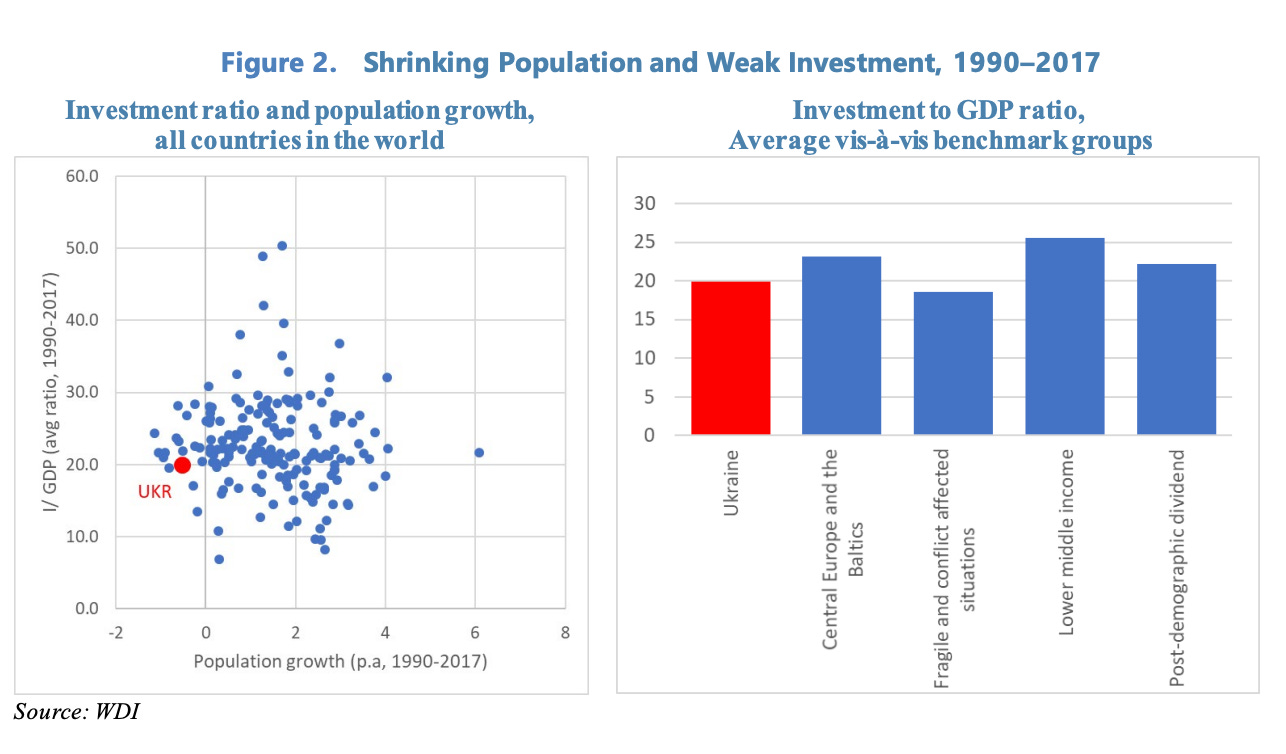

How do we explain this? The IMF authors point to Ukraine’s uniquely unpromising combination of low investment and declining population.

What the IMF authors do not talk about is war.

The IMF does not like talking about wars. The IMF like NATO normally steers clear of areas with active disputes. For this reason, the IMF’s programs for Ukraine in 2014-5 were very unusual. Some folks took issue with my characterization of the relationship between Western governments and the IMF in Ukraine as “instrumentalization”. But rereading this speech by David Lipton (America’s man at the IMF) from 2015 how you would describe the use made of the IMF by its principal shareholders, the Europeans and Americans? Lipton does not even deny the scale of the opposition the IMF leadership faced in pushing through the program.

Today, the question that is more pertinent is economics not the geopolitics of the 2014-5 bailouts. How badly has Russian aggression since 2014 damaged Ukraine’s growth? After all Ukrainians might well want to claim reparations.

Analysts who have addressed this question come to significant conclusions but in doing so they backhandedly confirm the underlying diagnosis of Ukraine’s developmental failure. In assessing the impact of the Donbass intervention, you have to make assumptions about how Ukraine would have developed without the conflict. Fair-minded analysts offer two benchmarks one in which Ukraine did actually begin to grow and one which simply projected the past and that means long-term stagnation. That implies two rather different assessments of the damage.

Source: Cebr

It should be said that despite the ongoing low-level war in Donbass, the IMF programs since 2015 have yielded more than many expected. There has been real stabilization and, finally, some economic growth. But Ukraine’s finances remain extremely fragile. And the IMF does not believe that its interventions have changed the underlying growth trajectory or successfully stabilized deep reform.

The overriding issue for both the IMF and the EU is corruption. The IMF has even prepared quantitative assessments of corruptions’s impact on Ukraine’s economy.

Ukraine : Selected Issues April 2017

On the left-hand side of this graph you have once again the stagnation of gdp per capita between 2005 and 2015 and then various estimated/imagined growth paths depending on various reform scenarios. Note the timeline on the x-axis. Even in the best-case scenario (nicely specified as the Ukraine achieving Eu-levels of corruption), convergence will take generations.

Why are things so bad? Beyond generalities about corruption, demographic decline and lack of investment, what is going on in the main parts of Ukraine’s economy?

Ukraine’s exports are dominated by metal commodities – steel – and agriculture. Perhaps we can get a handle a more concrete idea of Ukraine’s problems, if we start there.

I’ve found it hard to get good sources about the Ukrainian steel industry. But the news does not seem good. In November 2019, the industry produced the lowest volume of steel throughout the history of the country’s independence. The global recession in manufacturing at the time was hitting Ukraine amongst the hardest in the world. Why? One local analyst offered the following list:

the growing tax burden, political instability, tariff hike, hryvnia revaluation, and the like. There were also geopolitical risks, which one way or another depend on the leadership of our country.

Whatever the short-term development, the longer-term outlook for Ukraine’s steel industry is, surely, bleak. Caught between huge overcapacity of China and the EU’s CBAM proposals, which will tax high-carbon imports, it hardly seems a promising growth-driver.

Agriculture is far more promising. Ukraine’s agricultural potential is legendary.

Ukraine is home to a quarter of the fertile “black earth” soil (Chernozem) on the planet. It is already the world’s biggest producer of sunflower oil and the fourth-biggest producer of corn. Along with soybeans, sunflowers and corn are among the main crops grown in the Sunflower Belt, which stretches from Kharkiv in the east to the Ternopil region in the west.

But on the ground, since the end of the Soviet Union, agriculture has been another emblem of bitter legacies and frustration. Productivity is low. In 2014 agricultural value added per hectare was $ 413 in Ukraine compared to $1,142 in Poland, $1,507 in Germany, and $2,444 in France. In and of itself, this is hardly surprising. Ukraine has prime grain and lots of it. That makes for lower output per hectare than if you are raising dairy herds. In a land-rich country, labour productivity is more telling. In Ukraine that is highly polarized between a small workforce in large mechanized commercial farms and the mass of peasants who farm small plots. About 30 percent of the country’s estimated population of 43.6 million still live in rural areas and farming gives employment to more than 14 percent of the workforce. That statistic alone gives a truer indication of Ukraine’s backwardness.

Unsurprisingly, in Ukraine the issue of agricultural reform it is a hot political potato. The Tsar’s emancipation was in 1860s. Then came the revolution and German occupation under the Brest Litovsk regime, then the chaos of the 1920s, famine, collectivization and an even worse famine. Then the end of Communism and a new upheaval.

Though collectivization was brought to an end, as one analyst at Brookings points out, part of Ukraine’s agricultural backwardness is due to the fact that 25 percent of the farmland is still in state hands—10.5 million ha of 40.9 million ha of agricultural land with about 8 million ha being arable land. By comparison, Germany’s total arable farmland is about 12 million ha. That giant stock of land has become a political plaything and an object of intense concern over illegal privatizations.

The land that was actually privatized in 2001 was transferred to 7 million small land plot owners.

Small and medium-sized agricultural producers produce more than 50% of Ukraine’s total agricultural output. But under the terms of the 2001 Land Law, they were barred from buying, selling or mortgaging the property. As a result many farm families have had little choice but to rely on subsistence farming while leasing whatever was left to bigger farming operations. Leases run to a meager $150 per hectare yearly. Given the fertility of the soil rents should be far higher.

Up to 2021 Belarus and Ukraine were the last countries in Europe where farmland sales are prohibited.

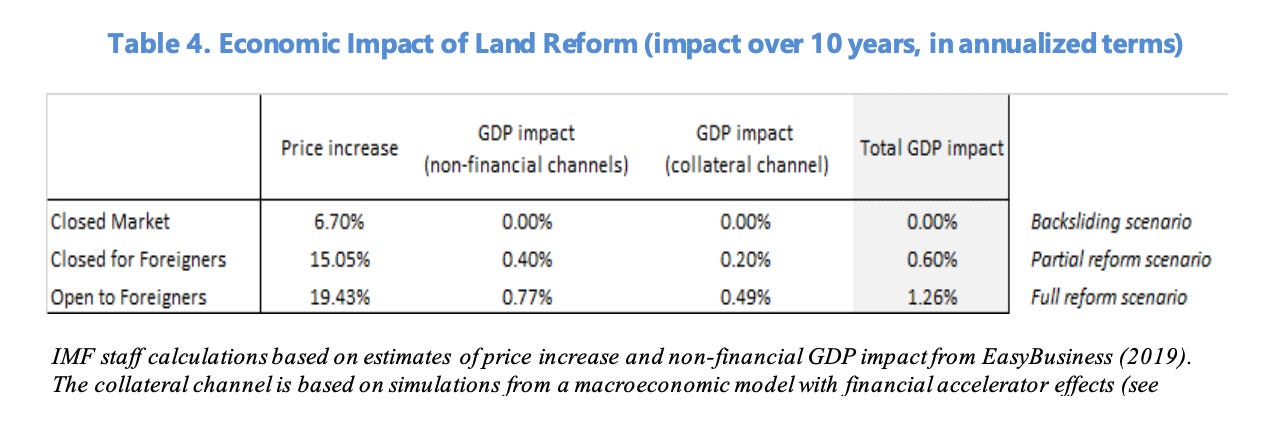

One of the great demands of Western advisors to Ukraine in recent years is that it should liberalize the land market. Perhaps through the development of middle sized families farms a prosperous growth dynamic might be unleashed. IMF modeling estimates a 6.7-12.6 bump in GDP depending on the reform scenario, whether it permitted both foreign and national land ownership.

Source: IMF Working Paper European Department Assessing the Macroeconomic Impact of Structural Reforms in Ukraine Prepared by Anil Ari and Gabor Pula Authorized for distribution by Ivanna Vladkova Hollar April 2021

Elected in 2019, one of Zelensky’s main reform programs was to push through a land reform. It was made into a condition of the latest $8 billion IMF program. And despite public protests and scuffles in parliament, in March 2020 in the midst of the COVID crisis, the legislation passed.

On July 1 2021, between the war scares of last year, a new era began. On that day it became possible for Ukrainians – not foreigners – to buy and sell up to 100 hectares. The real gold rush will start in 2024 Ukrainian legal entities will qualify for transactions involving up to 10,000 hectares. The law applies to an agricultural area of 42.7 million hectares (103 million acres). That is equivalent to the entire surface area of the state of California, or all of Italy.

Whether foreigners should be allowed to buy land is one of the most controversial issues around the reform. Zelensky had originally planned to enable it, but was persuaded, instead, to offer a referendum. That seems like a pro forma exercise since according to opinion polling more than 80 percent of Ukrainians oppose land sales to foreigners.

How much will change hands between Ukrainian interests is unclear. Leases on good agricultural land are already tied up. Furthermore legal certainty is far from guaranteed. Only about 73 percent of the nation’s agricultural land has been properly surveyed.

Nevertheless, the World Bank is in no doubt that land reform is a step in the right direction. As the World Bank puts it:

This is without exaggeration a historic event, made possible by the leadership of the President of Ukraine, the will of the parliament and the hard work of the government.

Ukraine’s politics are not used to that kind of praise from international financial institutions.

By the World Bank’s calculations it should increase rental income to small landowners by $3 billion every year. It will also give rural residents and small farmers, $24 billion of collateralizable assets that allow them to invest in irrigation, horticulture or non-agricultural small enterprises. In additional local taxation the World Bank estimates $2 billion annually.

The World Bank also notes that the Ukrainian authorities have put in place “legislation that reduces raider attacks and land-related schemes, makes land data publicly accessible, and allows local communities to plan land use.”

What they did not manage to do in time for 1 July was to pass legislation that enabled low-cost agricultural credit for small farmers. The Rada was dragging its feet over the Partial Credit Guarantee Fund. This is supposed to help smaller farmers excluded from bank credit that normally goes to farmers with more than 500 hectares and who grow grain and oilseeds, the main export crops. For SMEs interest rates are on average 5-7% per annum higher than those available for large enterprises.

The idea of the Partial credit guarantee (PCG) fund is to backstop agricultural lending by banks, thus producing a multiplier effect, enabling banks to lend on better terms to riskier small farmers. The controversy in the Rada concerned the management structure of the proposed fund and how to insulate it from political influence. This was a precondition for it to cooperate with the IMF and the World Bank and other IFI and thus leverage 20 billion hryvnas in loans to farmers, with a maximum term of 10 years. (Yup, Daniela G, is is derisking again!)

As the World Bank’s man on the ground put it, in no uncertain terms:

The adoption of the Law on the Partial Credit Guarantee Fund in Agriculture is the last cornerstone of the legislative foundation of land reform. Subject to the prompt adoption of the Law, the World Bank will be happy to support Ukraine in the rapid establishment of the Fund, as well as the earliest possible implementation of a temporary government program to provide portfolio guarantors to those farmers who need them now.

That World Bank blog was on October. The law was passed on November 7th. November 2021 that is. Yes, last year. Just as the military tension was beginning to escalate.

Today, only a few months later, these new items seem as though they come from another world.

Will Ukraine’s land ownership and credit structure be of interest if Russia’s unleashes its troops next week? No and with good reason. But, they matter for the longer term future. That is, in part, why I wanted to write this newsletter this morning.

Let us put this down. This is how things looked in the third week of February 2022. Let us hope that we can still be worrying about agricultural credit a month from now.

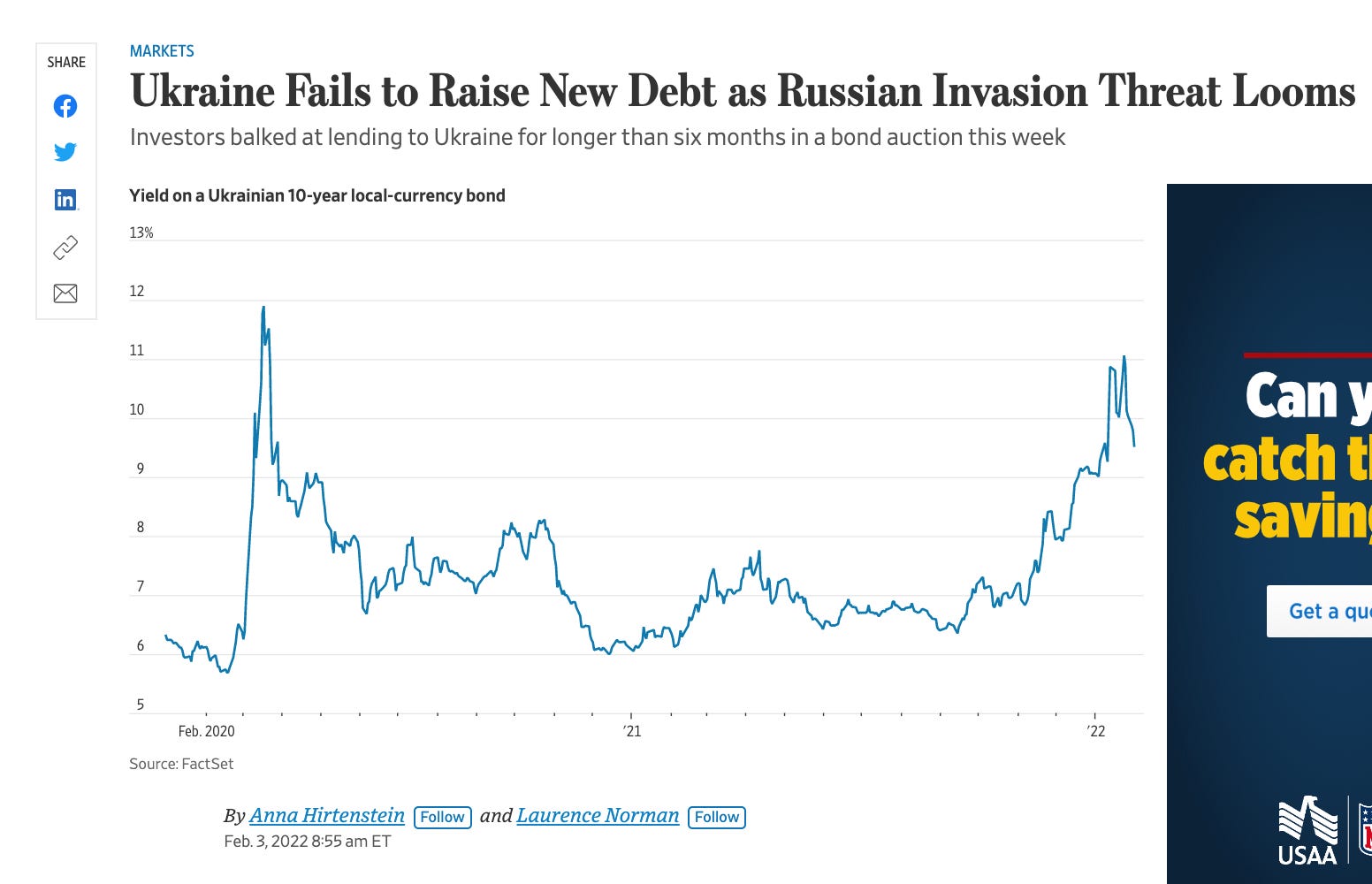

In the mean time the economic and financial situation in Ukraine is deteriorating. Not only are dollar-denominated bonds selling off and CDS-default protection surging, but at the beginning of February a local-currency public debt issue failed. No one wanted debt to be repaid one to two years from now.

Source: WSJ

Credit Default Swap insurance on Ukraine’s debt stand at 550 i.e. you pay 5.5% on top of any interest to insure debt. That is bad. It makes new borrowing unaffordable. But it is not yet apocalyptic. Let us hope the markets are right.

***

I love putting out Chartbook. I am particularly pleased that it goes out for free to thousands of subscribers around the world. Voluntary subscriptions from paying supporters sustain the effort. If you are enjoying the newsletter and would like to join the group of supporters, pick one of the three options, here: