March 2020 will forever be remembered as the month of the global lockdown. By April 2020 80 percent of the global workforce would be under one or other type of restriction. It was like nothing else in economic history.

In anticipation of that shock the financial markets began to quake already in February.

The immediate reaction, unsurprisingly was a flight to safety that put pressure on equities and corporate debt. That began in earnest in the last week of February. The effect of the flight to safety was to increase demand for safe assets like Treasuries. So far so good.

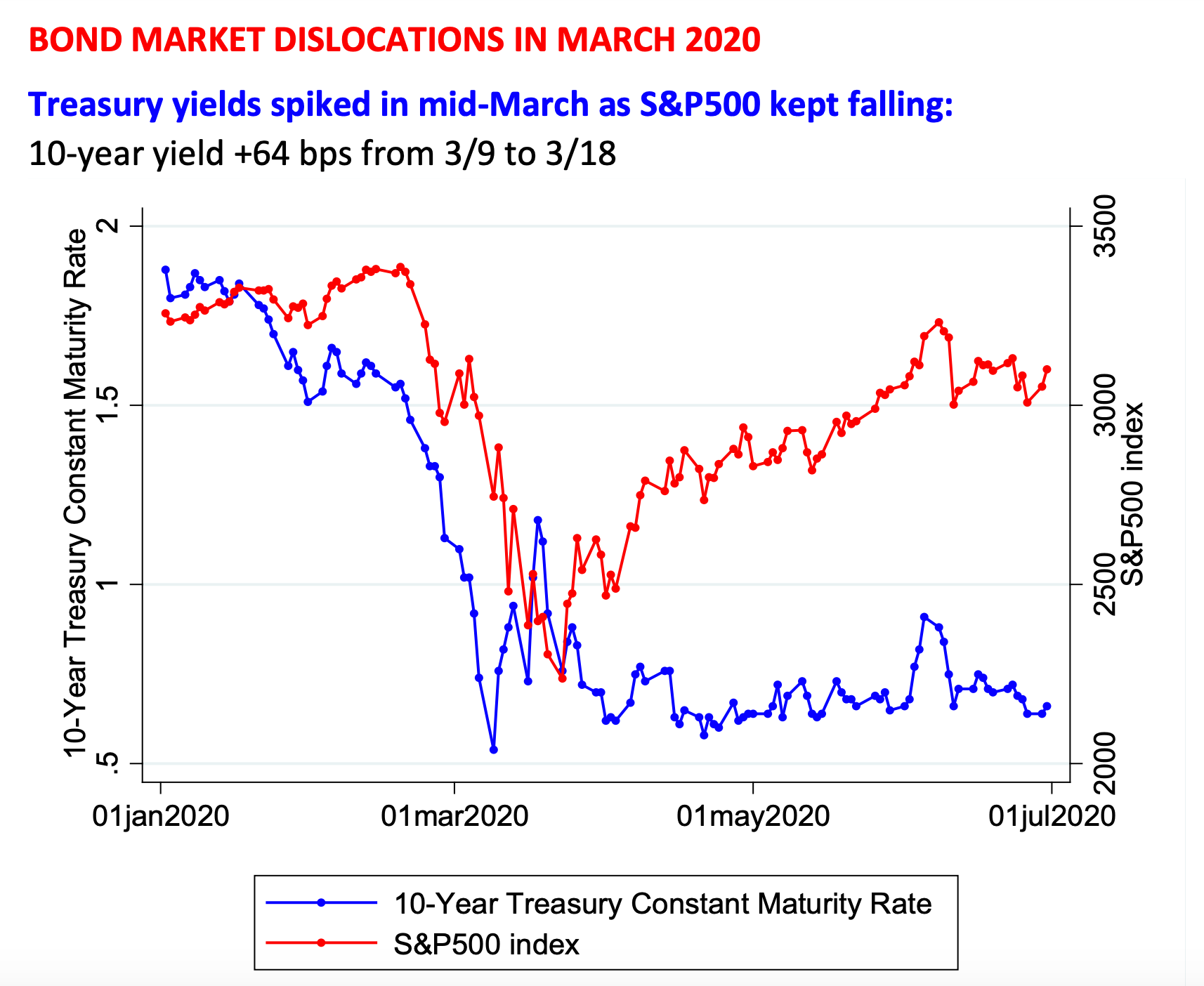

But on March 9 something much more disturbing began to happen. The flight to safety turned into a global dash for cash. Huge selling pressure built up in the market for Treasuries that one might normally think of as a safe haven for worried investors. Over the following two weeks the US Treasury market was profoundly disturbed. Prices fell, when one might normally have expected them to rise. Yields spiked. The market became dislocated. Market depth collapsed.

This chart from the excellent slide pack by Annette Vissing-Jorgensen, University of California Berkeley and NBER paints the picture. The surprising thing is that the blue line (Treasury yields) spikes as the red line (shares) descends. This means that both shares and bonds are selling off simultaneously. Everyone just wants cash.

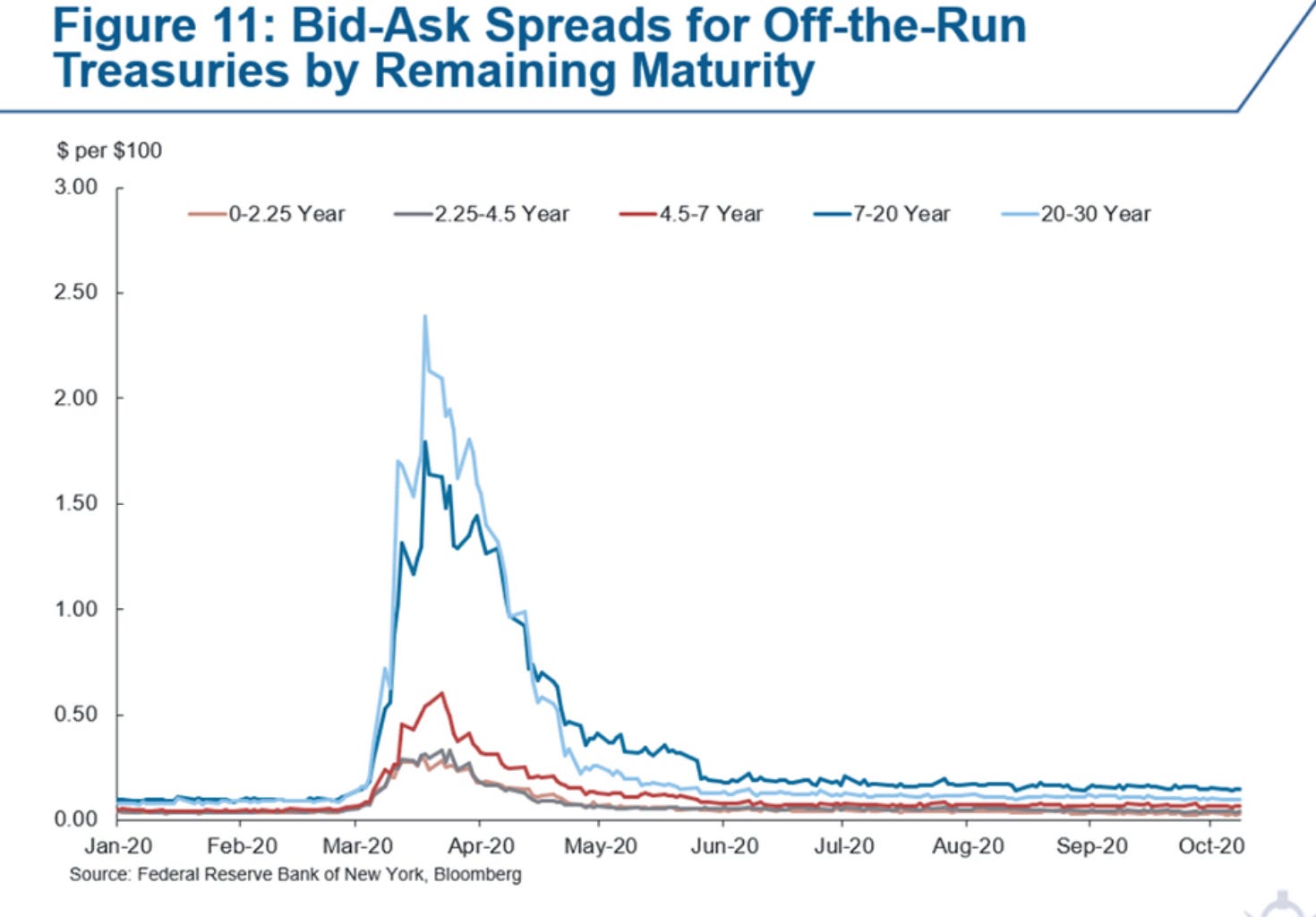

Meanwhile, the bid-ask spread for unfavored off-the-run Treasuries exploded. This gives an indication of market “stickiness”, the incentive that a dealer has to be offered to buy a Treasury.

Source: Logan (2020)

This disturbance in the Treasury market is of such significance, because the $ 20 trillion dollar market is normally the most liquid market in the global financial system. US Treasuries are the assets on which the market based financial system pivots. They are the safest asset. It is also the market on which the US government relies for selling its debt.

As the proponents of MMT have taught us, the reliance on debt to finance government is a choice. But, it is the currently prevailing arrangement and to sidestep it would be a significant shift, certainly amidst a crisis of confidence like that in March 2020. The Bank of England, which in effect announced that it would sidestep the UK Treasury market if necessary, hastened to insist that it was doing so only temporarily and as nothing more than an expedient.

A dramatic sell off of US Treasuries is a dark fantasy that has haunted political economic prognosis since the beginning of the century. In the early 2000s commentators imagined the Chinese selling off their hoard of US assets, driving US interest rates up and the dollar off a cliff. Superficially, the 2020 tremor resembled that scenario. Foreign asset holders were selling US Treasuries in large volume. This was, therefore, a crisis linked to the role of the dollar as a reserve currency. But, the logic of the March 2020 crisis was precisely not a flight out of dollars. It was a flight into cash and the cash that everyone wanted was dollars. As Treasuries sold off, the dollar rose in value against all other currencies.

This was a disruption to the US financial system resulting from the use of US dollar assets as the world’s piggybank. Everyone wanted to smash the piggybank. But it was not a challenge to the anchoring role of the dollar. Rather the opposite.

The challenge for the Fed was huge. As several great journalistic accounts have made clear, the instability in the market was extreme. See for instance this excellent piece by Colby Smith and Robin Wigglesworth of the FT.

Nor was it confined to the US. Very serious pressures of a similar variety made themselves felt in the UK Treasury market, where the Bank of England has spoken of a “meltdown”. And in more decorous tones the ECB has also reported on dramatic turbulence in Euro area fixed income markets . Part of that was driven by anxiety about Italy, “spreads” and the weak architecture of the euro. But that was compounded by the global dash for cash. I will return to the events in Europe in a future newsletter.

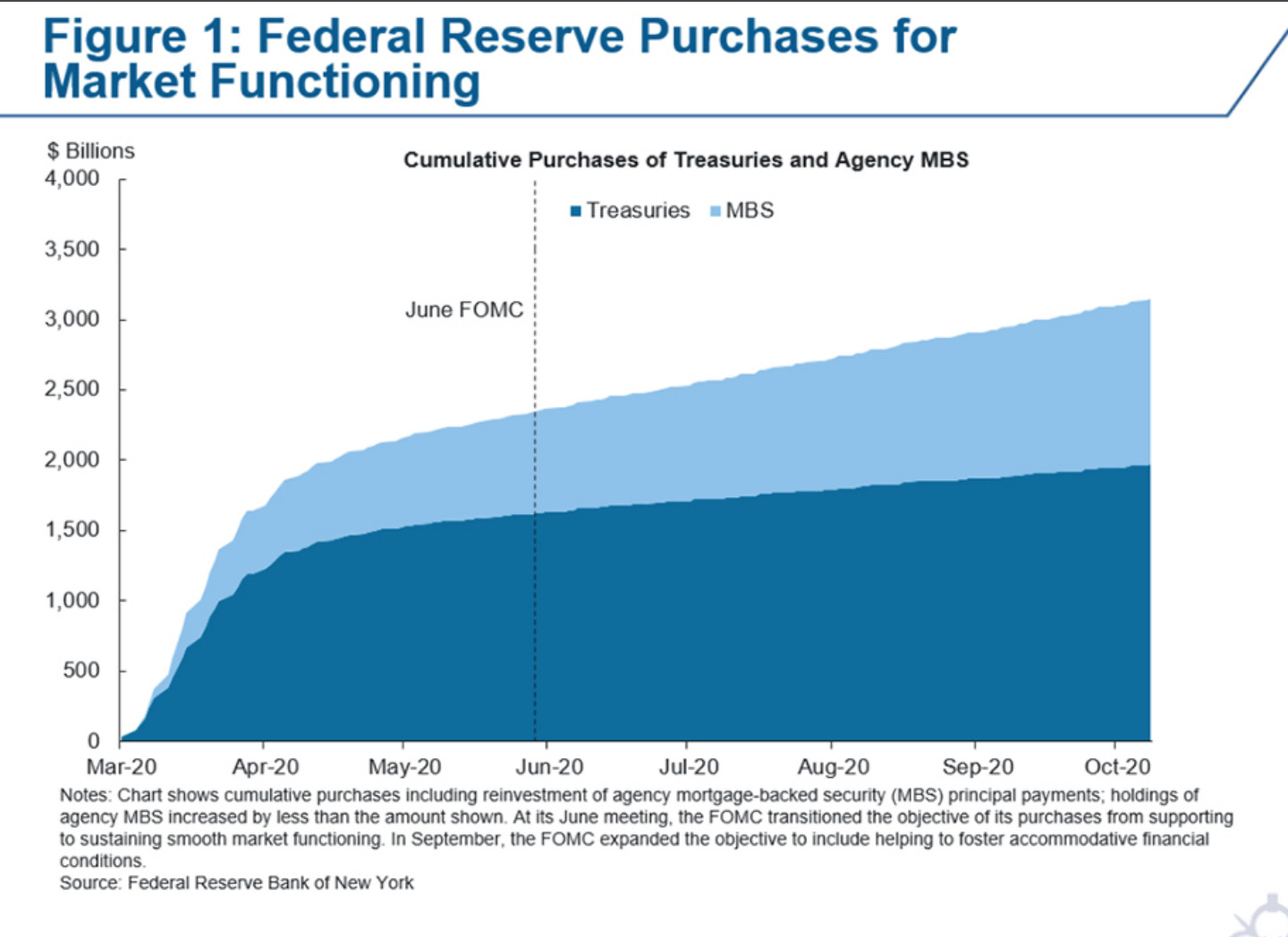

The turbulence was stopped in the last days of March by concerted central bank intervention. But it was a hair-raising moment. It is not clear whether the global financial system could have survived unscathed many more weeks like those between 9 and 27 March. The scale of the central bank intervention, particularly that by the Fed, is testament to the scale and urgency of the problem. The Fed purchased a trillion dollars in Treasuries in a matter of weeks.

Source: Logan (2020)

At the safe distance of a few months a debate is now going on about what triggered the turbulence. Who or what was to blame? Research is revealing new dimensions of the problem. The global Financial Stability Board has issued a wide-ranging report. The BIS has weighed in. The Fed in its November Financial Stability Report devoted to a special “box” to the theme.

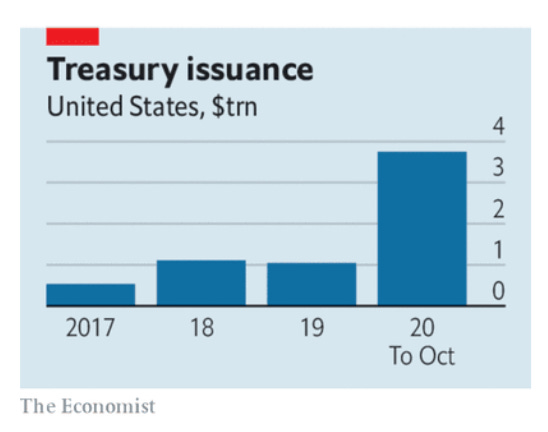

This is not merely a matter for academic debate or retrospective recrimination. It is an urgent and practical issue. Given the volume of debt that will need to be issued over the coming years, all around the world, but particularly in the US, ensuring the smooth functioning of the Treasury market is a paramount concern. See this timely intervention by The Economist.

There is no more significant area of financial reform for the new administration to work on.

I have pulled together here a variety of charts and arguments about the March 2020 moment. If you have other angles, report or experiences you would like to share, you know where to find me.

The issue is so large that it merits several takes.

In this first installment I am setting the scene and focus on the selling side of the crisis. Who was selling and why? In a second take I will focus on the question of why no one was buying. In part 3 I will look at the disturbances in the Euro area and the UK. In take four I will look at the Fed’s response and the reform debate.

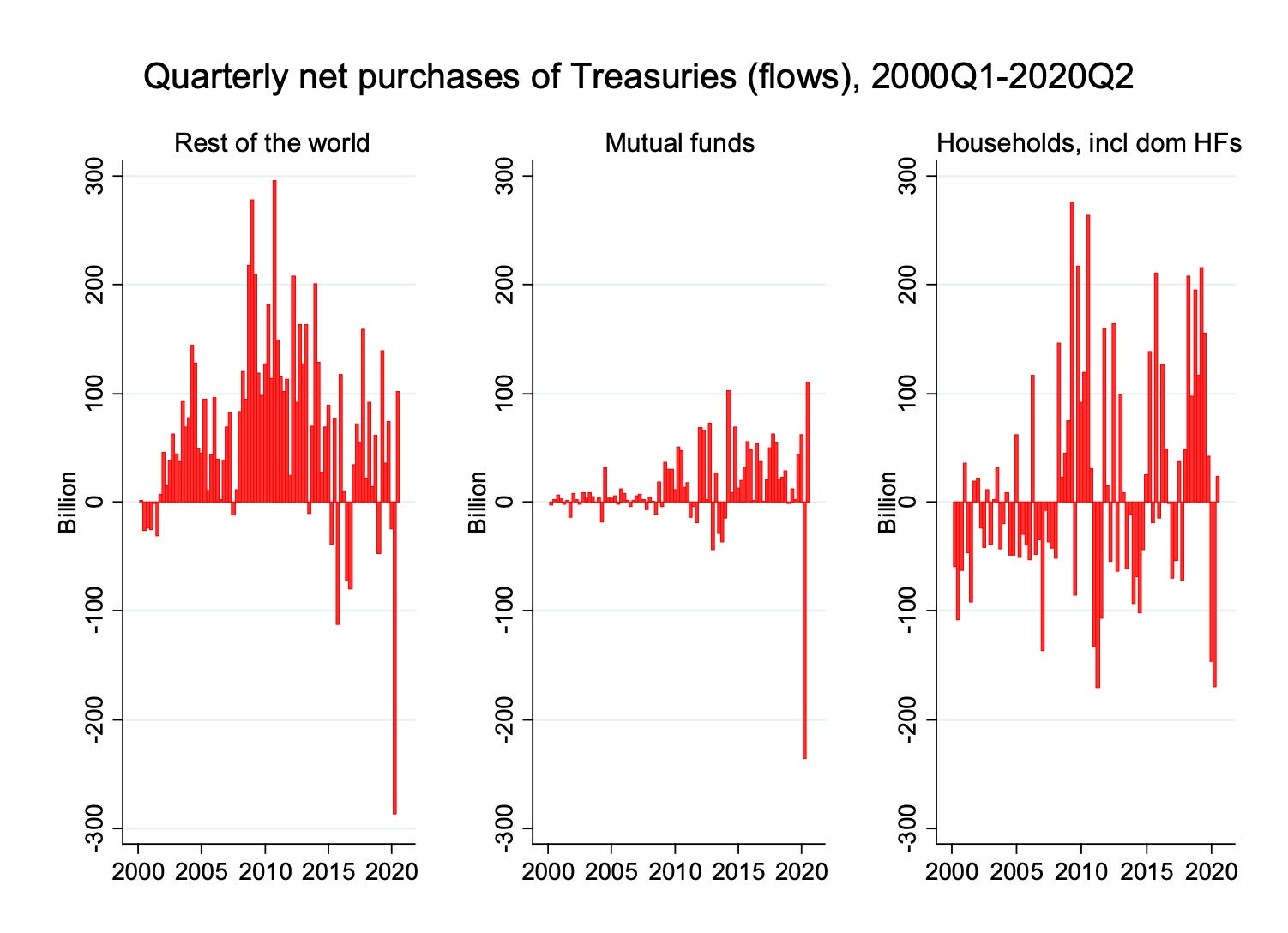

Initially, it was tempting to blame particular groups of sellers for unsettling the market. But the data pulled together by Annette Vissing-Jorgensen shows that, in fact, the sales were broad based and driven by three groups: foreign reserve managers, hedge funds and open-ended US mutual investment funds.

Source: Annette Vissing-Jorgensen 2020

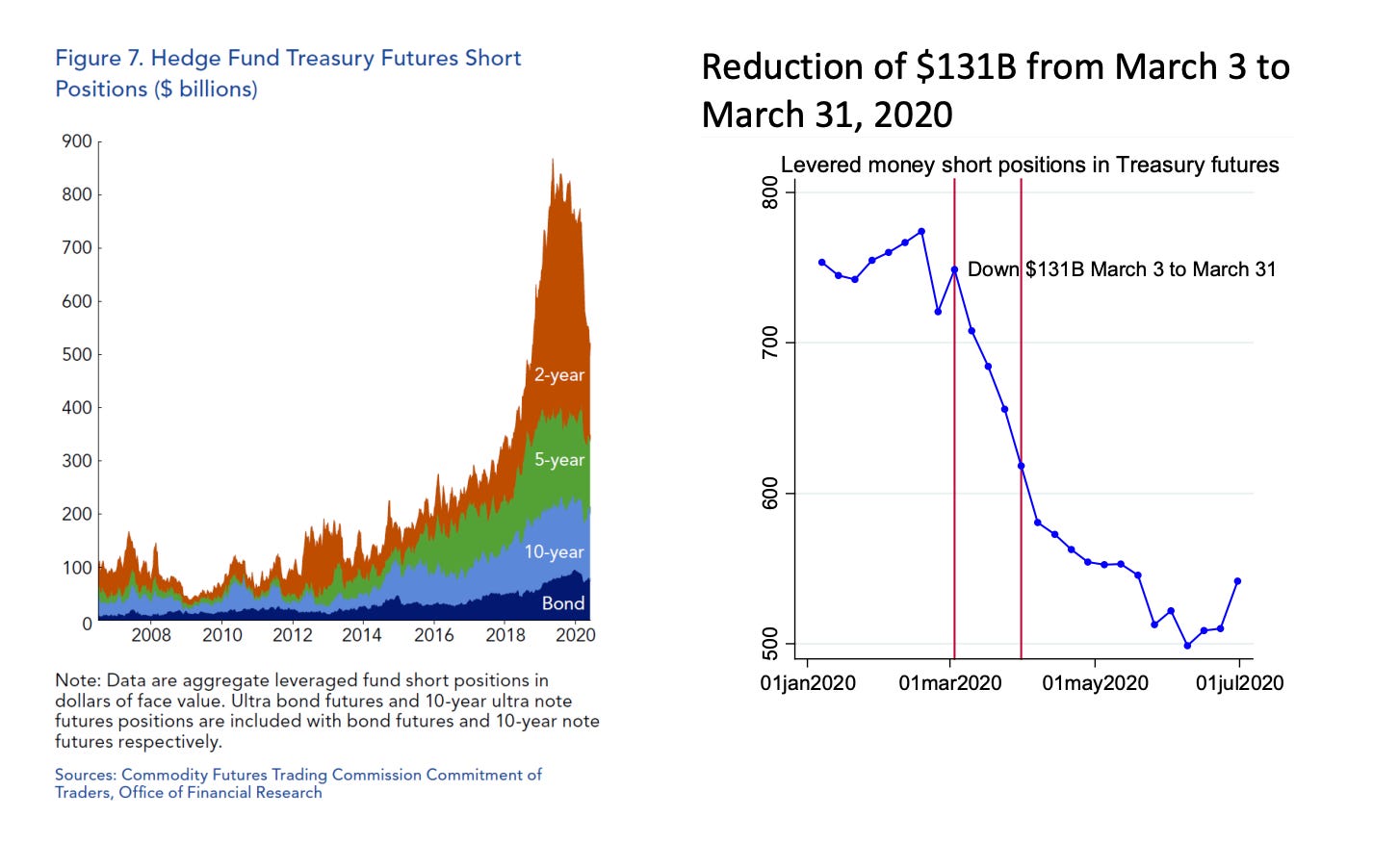

The most contentious part of the story is the role of hedge funds and the unravelling of so-called basis trades. Vissing-Jorgensen gives a brilliantly clear and succinct explanation.

In the basis trade the hedge funds enters a short Treasury futures position i.e. promising to deliver a Treasury at a future date in exchange for a good price. To make profit you find cheaper Treasuries to buy now. You fund your holding in the interim by repoing them i.e. swapping them temporarily for cash. It is a business that generates profits on tiny margins by trading at large scale.

Source: Annette Vissing-Jorgensen 2020

As data on hedge fund treasury futures short positions shows, the trade has surged in popularity since 2014. With volume rising from $100-200 bn to over $800 bn in 2019. In March 2020 the trade unwound. Prices of Treasuries began to behave erratically relative to futures contracts and repo funding became more expensive. There was a reduction in hedge fund short positions in Treasuries of c. $ 131 bn over the course of the month.

We would be better able to gauge the impact of this winding down of hedge fund positions, if we had more comprehensive data. It is a remarkable fact that the Fed does not have better data, or at least it claims not to have better data on their activity. It is possible that some additional hedge fund selling shows up in sales by the Rest of the World, most notably from the Cayman Islands.

All in all, hedge fund strategies unwinding added to the turmoil but, as Lorie Logan, Vice President at the New York Fed has put it: “In the context of broad-based selling pressure … I think of these sales (by hedge funds) as an important contributing factor, but not the sole source of the challenges.”

A larger source of openly declared domestic sales were the mutual funds. As the Fed stresses in its Financial Stability Report, the promise by open-ended funds to allow investors same day withdrawals whilst their money is invested in illiquid assets creates considerable run risk.

The growth in mutual funds since 2008 has been huge.

Size of the US Fixed-Income Mutual Fund Sector: 1995 to 2019. Fixed-income funds include government bonds funds, corporate bond funds, loan funds, and multi-sector bond funds. Source: Ma, Xiao, Zeng (2020)

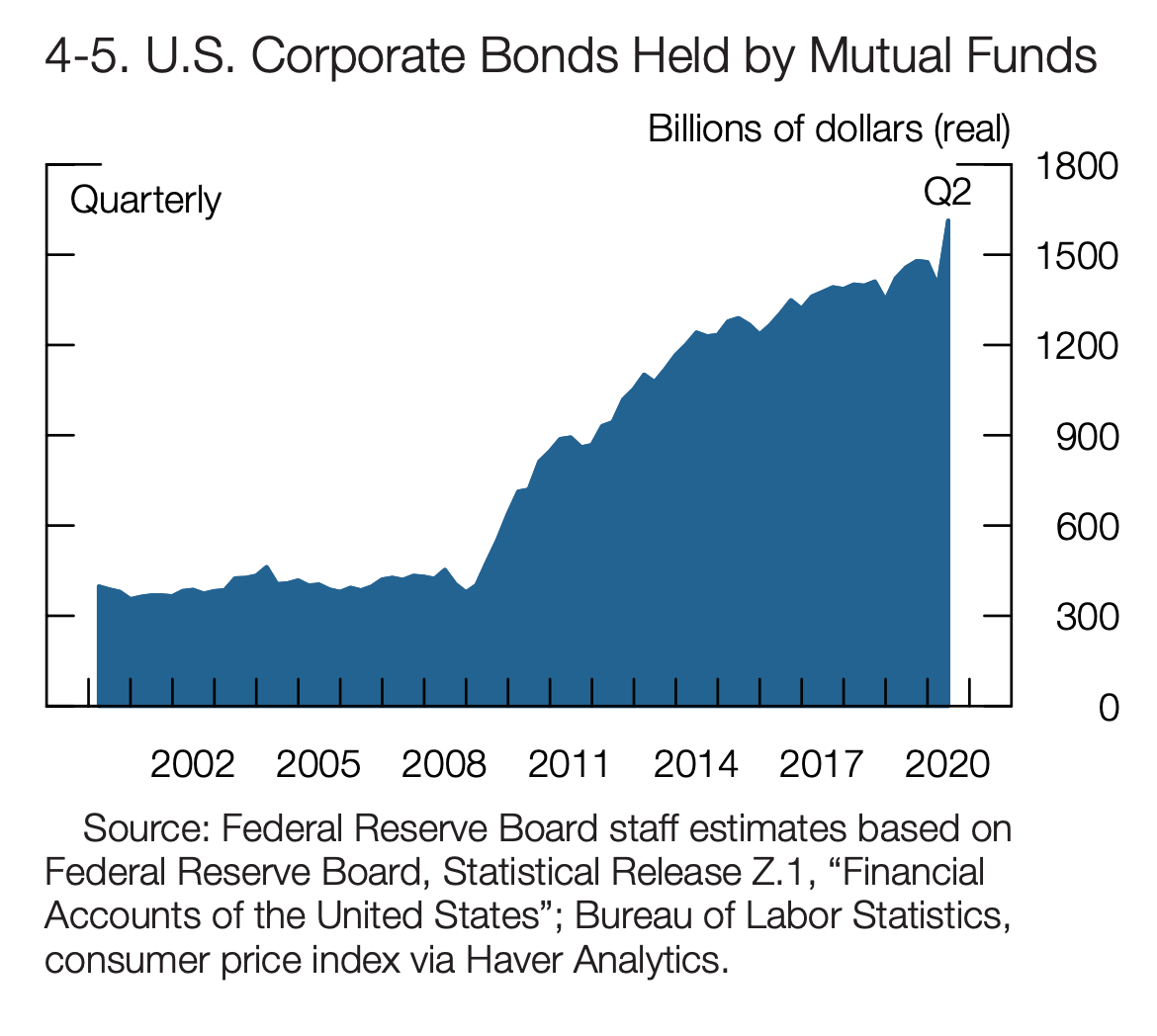

In search of yield the mutual funds have moved heavily into riskier corporate debt:

Source: November Financial Stability Report

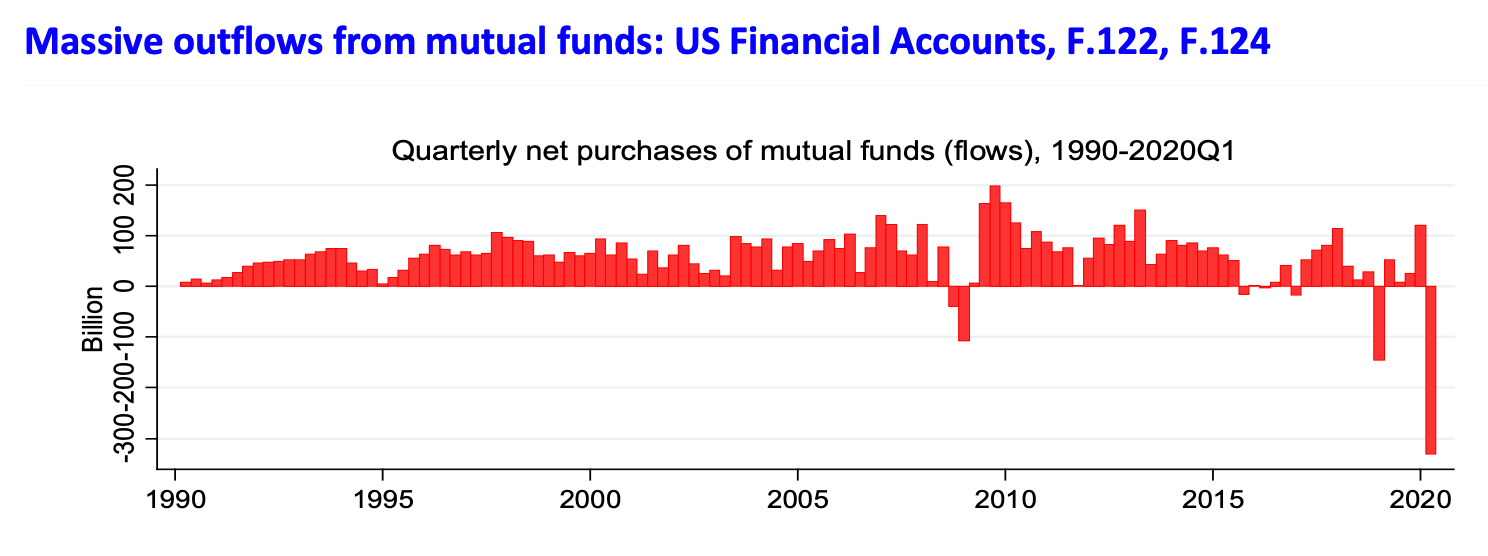

This inherently unstable structure unwound in the spring of 2020, when the mutual funds suffered bigger withdrawals than ever before in their history. Far worse than in 2008.

Source: Annette Vissing-Jorgensen 2020

To meet these huge demands for cash, mutual funds were forced to sell their more liquid assets, which means Treasuries, rather than stressed corporate bonds. Through this so-called “pecking order effect”, anxieties about corporate debt spilled over into fire sales of Treasuries. Ma, Xiao, Zeng (2020)

Bad as the run on the mutual funds was, the largest sales by volume was by the “Rest of the World”. This category is obfuscating. There are data for foreign transactions and holdings. There are data that divide between private and official and by country. But there are no publicly available data that divide by country and by private/official.

Source: Annette Vissing-Jorgensen 2020

If we use the holdings data, which are considered more reliable, then it was foreign official sales that dominated the sell off. Presumably these were foreign reserve holders, desperately trying to provide dollar liquidity to local financial institutions that were finding it hard to obtain dollar funding.

This is the gap that was filled by Fed liquidity swap lines with other central banks. The new Fed facility that enables foreign reserve holders to repo assets with the Fed without having to offload them into stressed markets is designed to address the same pressure.

In a situation in which Treasuries are being sold at knock down prices the obvious question to ask is why is no one buying them. There are clearly profits to be made. The normal purchasers would have been market makers. I will address that side of the crisis in the next newsletter.

The key takeaway from the first installment is the drama of the shock and the multi-sided pressure that this key market was under. It is the true hidden crisis of March 2020.

Part 2 to follow on Wednesday.

In other news:

I hosted an interesting conversation with Nicolas Veron of Bruegel and Peterson and Marco Buti of the European Commission. Enjoy the video: